If a central bank is doing something, you can almost be assured that at its theoretical root lies a statement or idea proposed by Milton Friedman in the 1960’s. This is not to say that Friedman would approve of what has been done in his name, even before he died a decade ago he became flustered over what his disciples, loosely speaking, had been up to even by that point. In the end, however, he opened these doors and thus his name deserves its attachment to what has been carried out.

The nascent monetarism of the 1960’s actually stood in sharp contrast to the dominant Keynesianism of the time; in fact, most of Friedman’s work rose out of trying to disprove a great deal of it. The problem we all live with today is that in the later 1980’s and throughout the 1990’s Keynes and Friedman were no longer kept separate as opposite ends of a heated debate. They fused, and suddenly we were left with only one operating dogma which held an activist central bank, not the background guidepost central bank Friedman had envisioned, as the primary if not only monetary agent.

In the years after Samuelson and Solow’s introduced their “exploitable Phillips Curve” in 1960, Friedman along with Edmund Phelps debunked much of it but not before its incipient ideas had put the global economy on the path to a decade and a half of stagflation. Speaking at a conference in 1966, Friedman said:

In my opinion, there is what might be termed a “natural” level of unemployment in any society you can think of …for any given labor market structure, there is some natural level of unemployment at which real wages would have a tendency to behave in accordance with productivity…If you try, through monetary measures, to keep unemployment below this natural level, you are committed to a path of perpetual inflation at an ever-increasing rate.

Rather than heed Friedman’s warning, economists of this neo-Keynesian era decided instead that what was wrong about the Great Inflation was not the attempt but rather the execution. They retroactively ascribed Robert Lucas’s rational expectations theory such that it would describe the manner in which central banks should have responded. Economists have never stopped loving inflation, believing it to be a genie which could be controlled. In other words, like Communists who to this day still claim it didn’t fail because it was never truly tried, Economists are similar confident that inflation policy has been sufficiently modernized so as to go back and make the same attempts.

In his speech in 1966, Friedman warned:

Our record economic expansion will probably end sometime in the next year. If it does, prices will continue to rise while unemployment mounts. There will be an inflationary recession. Many will regard this prediction as a contradiction in terms, since it is widely believed that rising prices always go with expansion and falling prices with recession. Usually they do, but not always.

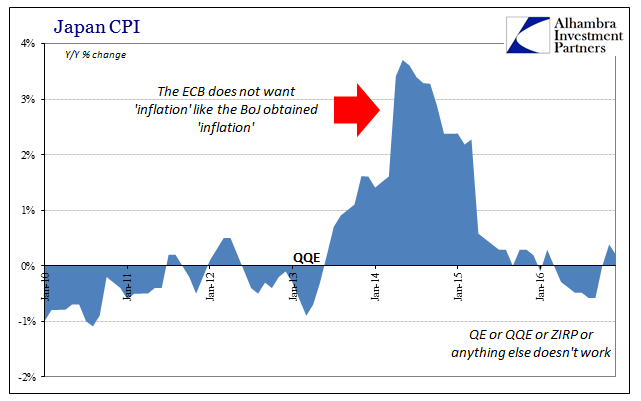

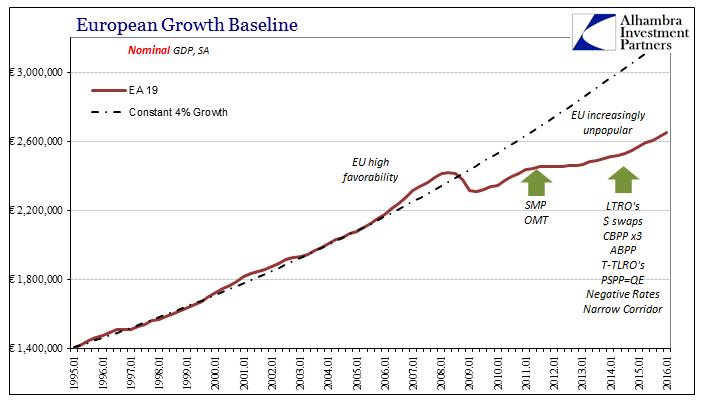

In the 2010’s, central banks the world over have been trying to prove this statement wrong. They have been actively seeking out inflation through increasingly ridiculous means. The Bank of Japan, as always, pioneered the absurdity, experimenting with parameters beyond size of asset purchases, to various forms of assets and even negative interest rates. They seek out the most ridiculous possible negative (instability) factors by which to create a positive and sustained recovery.

At the other end of the scale has been Europe, according to convention, where the ECB has been judged slow to respond and often meager in its response. This circumstance of reluctance is always attributed to Germany who is always placed in fear not of Nazis but the Weimar hyperinflation that brought about Nazis. By last year, however, the mainstream of global monetary thought began to realize the difference never was QE in the first place; it was instead that none of this actually works in the way in which it is meant to work – from money to credit to output to wages. What has happened instead is variable forms of unstable prices, whether consumer, asset, or currency.

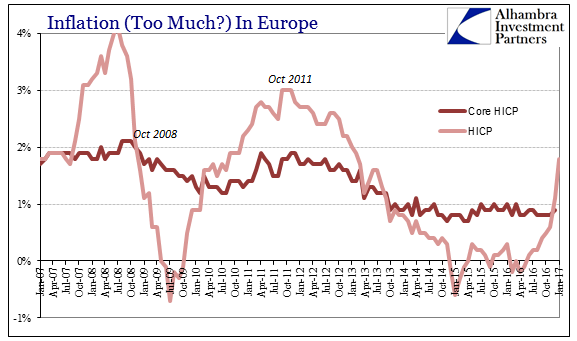

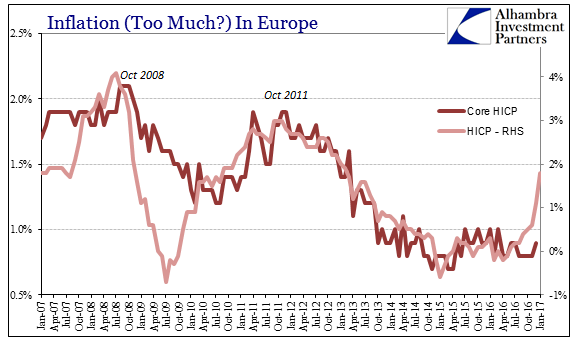

After trying so hard to ignite inflation by keeping the real interest rate in Europe below whatever monetary officials there believed the natural interest rate might be (the 21st century proxy for Friedman’s “natural level of unemployment, R*, or r-star), and then giving up on the quest, Europe finally is on the receiving end of inflation. As recently as May 2016, HICP estimates were negative for the EU as a whole, and just +0.6% in November. As of January 2017, the HICP was 1.8% and appears likely to burst well above the target rate of 2% in February. Wholesale prices in Germany burst in the latest figures:

Wholesale inflation – a measure of costs faced by German food retailers – jumped to its highest level in more than five years at the start of 2017 as rising food and energy costs lift prices across the continent.

Germany’s year on year wholesale inflation accelerated from 2.8 per cent to 4 per cent in January – its annual highest level since late 2011.

Naturally, there are many who now want Mario Draghi to declare success and start scaling back ECB efforts. He is understandably reluctant, since there is every indication what is happening in Europe is not monetary policy success but rather Friedman’s caveat resurrected. HICP rates are up because of commodity prices rebounding from the bottom, not because Europe’s economy is on the righteous path to recovery and mending.

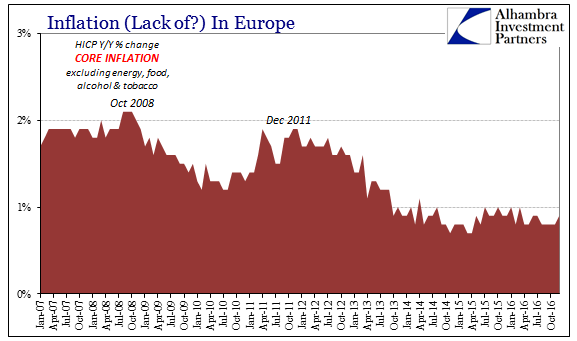

If we strip food and energy prices from the HICP figures, we plainly see the difference. The so-called core prices fell off starting in 2011, coincident to the re-introduction of global money problems, and have yet to rebound even though energy and food prices have. In large part that is because of the euro’s exchange value against the dollar, which isn’t “sterilizing” the energy price retracement this time so much as amplifying it. Therefore, Europe finds itself in an inflationary environment that isn’t what Draghi has been seeking all along, instead threatening to replay the circumstances of Japan in 2013-14.

The rise in EU HICP rates is almost exclusively the sort of “cost push” inflation that is devastating to fragile economies, just as it was in Japan not long after the onset of QQE. Four years ago it wasn’t QQE’s “contributions” to the unthinkably large pile of useless, idle bank reserves that did it, rather it was the response of Japan’s currency that made it all that much worse for the Japanese people (since it delivered none of the benefits). Europe has now set itself up in almost exactly the same shape; a set of conditions that are perfectly exemplified by the growing difference between HICP and core HICP of late.

Friedman cautioned that Keynesian economists should rethink the manner in which they proposed to meddle with money and inflation. He should have scolded them instead to stop meddling with currency and inflation altogether. The world craves, demands, stability. All it gets instead are all the ways economic pain might be inflicted by these academic types who are apparently incapable of empathy. Modern economics has devolved steadily into all the ways in which especially activist central banks can destabilize systems that much more thinking that greater instability will suddenly spark a stable turnaround. Instead, like the 1970’s, the economic system in particular gets locked into a pattern of variable illegitimacy from which it cannot escape no matter what is done to it (because of what is done to it, instead of for it).

Stay In Touch