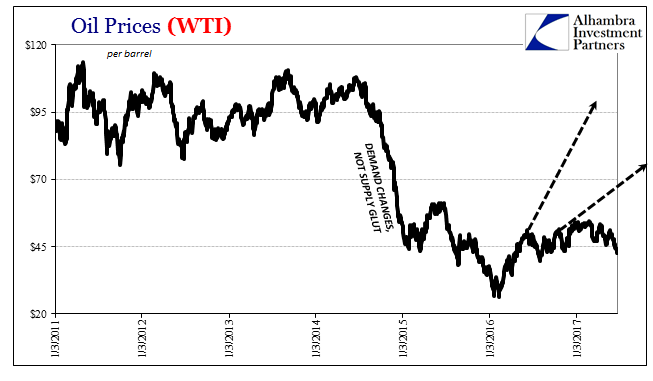

When the price of oil first collapsed at the end of 2014, it was characterized widely as a “supply glut.” It wasn’t something to be concerned about because it was believed attributable to success, and American success no less. Lower oil prices would be another benefit to consumers on top of the “best jobs market in decades.”

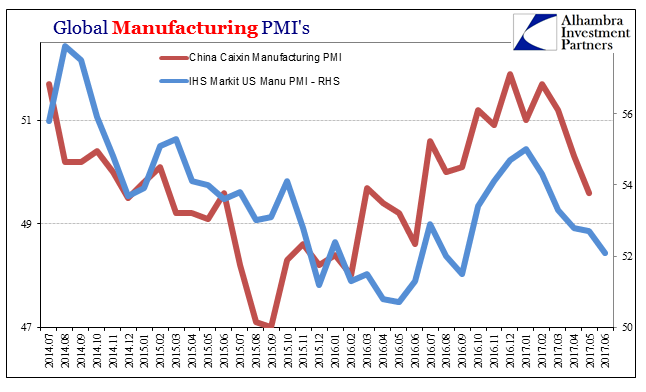

That may have been how it was written in the mainstream, but in especially manufacturing it all looked very different. The global industrial sector quickly ran into a contraction, one that couldn’t have been anything other than a sudden and sharp drop in demand. For manufacturers, the price of oil was a realtime indication of business conditions very much like what they were seeing on the demand side. Economists could dismiss it as benign, economic agents did not.

The power of the oil price was that it held information content that wasn’t immediately available (practically) anywhere else. Policymakers and economists kept up their optimism all throughout, and by the harmonized uniform drop in global manufacturing PMI’s industrial businesses stopped believing them relatively early on. Crude had become the only useful business barometer anyone might be able to rely upon.

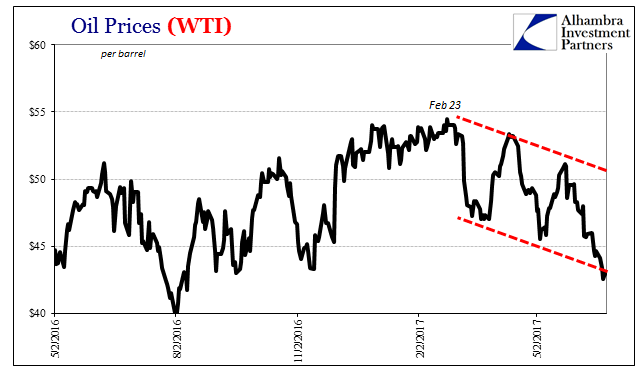

For oil prices to rebound, then, was a hugely positive signal for potential global economic demand. It took several months for that to become legitimized, both as a matter of financial prices (volatility can mean false rallies, too) and as economic weakness related to the downturn continued to linger well into the summer. By the time “reflation” was taking hold, it did appear that though the WTI bounce wasn’t going to be a short, parabolic restoration it was at least to that point sticking.

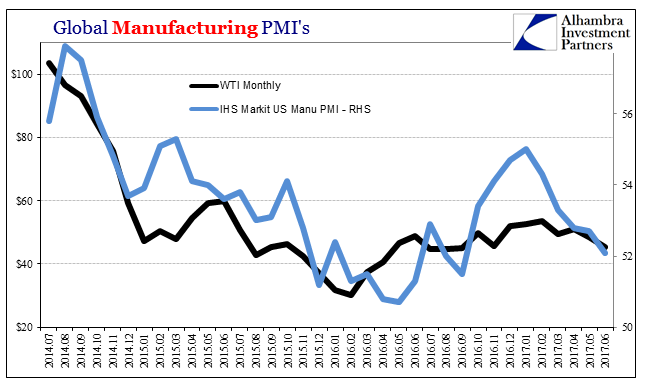

It is difficult to discern exactly what effects that view might have had overall, but in terms of manufacturing sentiment it is very likely the reason for what is more and more proving to have been naked over-optimism. That is to some degree understandable given the nature of the period prior to it. A two-year contraction (in some places longer) that finally ends coincident to rising oil prices might make some believe in a very robust immediate future.

Increasingly sentiment, particularly in manufacturing and not limited to just those in the United States, is reverting back to where oil prices actually are of late. The latest is the IHS Markit flash PMI reading for US manufacturing in the month of June 2017. At 52.1, that is the lowest since last September and a level far too much like the worst of the downturn (the Markit PMI never did drop below 50, suggesting once more why PMI’s should not be read as above or below that level but rather as relative indications of relative conditions).

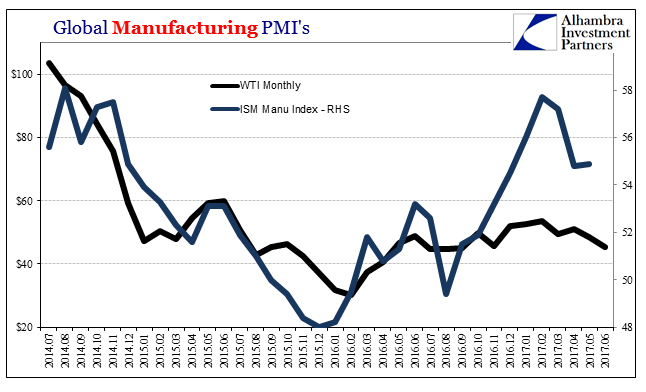

This over-optimism compared to oil prices is not a singular correlation; we find it to an even higher degree elsewhere.

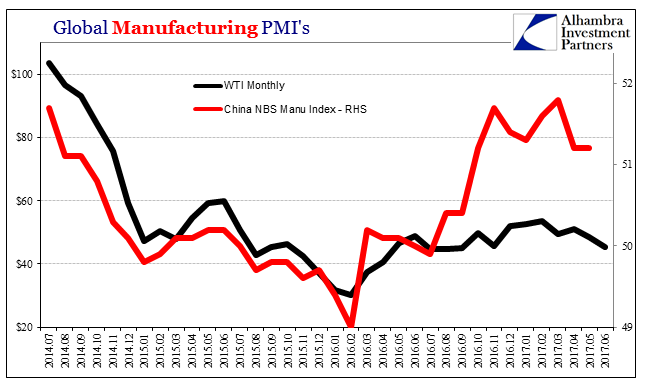

In the Chinese official version, we see the possible introduction of another variable upon forward economic expectations. China in early 2016 began a prominent and large “stimulus” program through State-owned Fixed Asset Investment (construction of more ghost things?). By early autumn, the combined promise of Chinese “stimulus” with steadily if slowly rising oil seemed to have suggested the possibility of for the first time in years actual economic improvement.

Some firms likely acted on those expectations, which is what we find in rising PMI’s. The indices are supposed to measure more tangible factors like the status of orders and production. If some industrial companies did ratchet up their activities based on those considerations, it is also understandable why they might scale them back again later in 2017.

Both Chinese economic data and now what is clearly a downtrend in oil would make even those buying into the “reflation” premise more cautious about doing so. For others, the retreat in WTI (or Brent, Tapis, etc.) brings up too many dark signals more of early 2015.

Just as in 2014, this latest retrenchment recalls again the flaws in mainstream economic theory. Economists believe that expectations are an almost magical property. If you can make someone believe (through largely asset prices) that the future will be much better, then it is assumed that this person will act today on that outlook. And that is true, but only to a limited extent, and certainly nowhere near enough to overcome more tangible impediments.

It does invoke the concept of hysteresis, where the possible beginning of expectations-driven activity must be confirmed at some point by something greater and more solid than further expectations. In other words, you can start to do more or even just plan on increasing production but if at some point it looks like all you are doing is adding to inventory (or even not allowing inventory levels to shrink fast enough) expectations aren’t going to be nearly enough.

Despite high levels of manufacturing and service sector business sentiment, as well as perhaps greater consumer confidence, it has not as yet turned into customers, revenue, and the confirmation that all this positivity was actually appropriate.

In the end, it appears, expectations need to be “backed” by more than just the absence of further contraction; and that was before oil prices turned back lower again around late February. Now the economy seems to be building up all over again to renewed problems of both unconfirmed expectations as well as now lower oil prices signaling nothing sufficiently positive (if not downright negative) about future global demand over the near and intermediate terms.

Stay In Touch