It’s actually quite difficult to answer the question posed in the title, which in itself is a clue. What we know for sure is what does not count as reserves for a non-reservable currency system. It’s that contradiction that sets off the often graphic misconceptions.

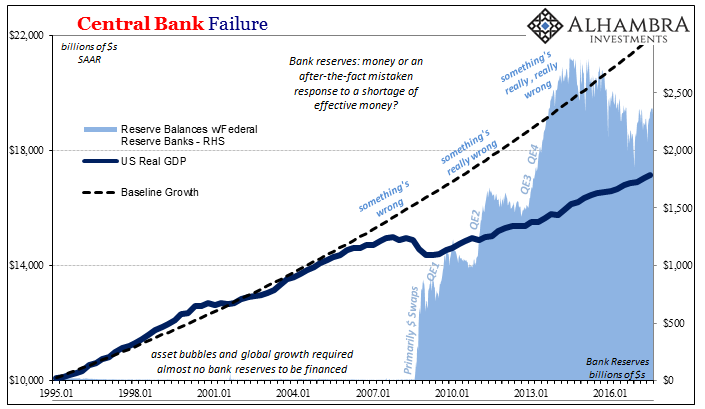

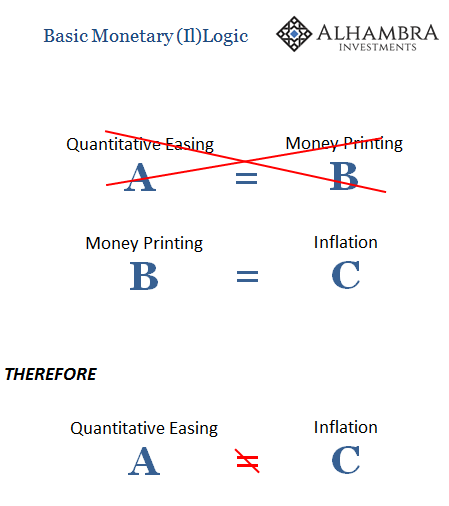

Quantitative easing has been described as printing money. That’s certainly what central banks wish for you to think because its primary purpose is to influence inflation expectations along those lines. In practice, QE only creates bank reserves as a direct byproduct of its undertaken transactions. So, in reality the most that can be said of quantitative easing is that it “prints” bank reserves.

Whether or not those reserves are money is the entire story. For many if not most they are because what else does a central bank do if not that? But bank reserves in the American system are, actually, a recent occurrence. There were practically none up until the panic in September 2008; the week the GSE’s fell into conservatorship, the one right before Lehman, the entire balance of bank reserves totaled $9.02 billion with a “b”, not trillion with a “t.” For some, this explains a lot, meaning that without bank reserves the system was monetarily vulnerable.

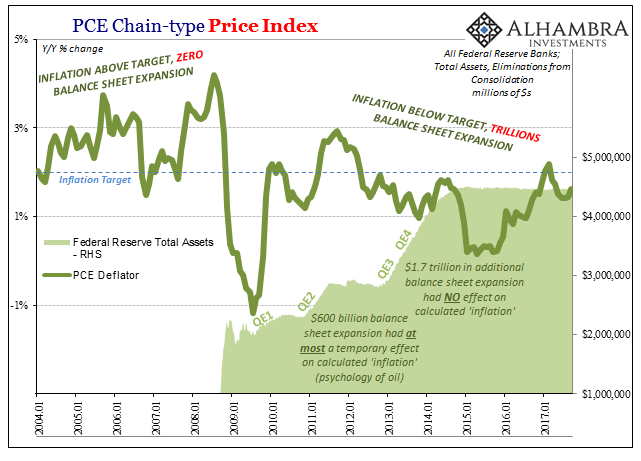

And yet, there was then the problem of multiple QE’s. Despite the sudden appearance of trillions of them, the global dollar system underwent several subsequent liquidity/monetary setbacks. As Open Market Account Manager Brian Sack exclaimed during one of those setbacks in early August 2011:

MR. SACK. Can I add a comment? In terms of your question about reserves, as I noted in the briefing, we are seeing funding pressures emerge. We are seeing a lot more discussion about the potential need for liquidity facilities. I mentioned in my briefing that the FX swap lines could be used, but we’ve seen discussions of TAF-type facilities in market write-ups. So the liquidity pressures are pretty substantial. And I think it’s worth pointing out that this is all happening with $1.6 trillion of reserves in the system. [emphasis added]

With them or without them, the result was the same: gross systemic illiquidity. At the very least, it should give one pause when blindly assuming what role bank reserves might actually play in the modern monetary system.

How could the system evolve in this fashion? The answer is, ironically, at least at the start, federal funds.

In December 1957, the Federal Reserve launched a comprehensive study of the federal funds market. It wasn’t a new piece of the US dollar system by any means, but in the fifties it was resurrected after decades being dormant in the aftermath of the Great Depression. The monetary collapse in the early thirties obviated any need for such a robust, dynamic money market simply because nobody remaining trusted it any longer; it became common bank practice to hold a huge liquidity cushion far and above any statutory requirements as a matter of prudence.

As that practice wound down in the re-remerging economic and financial opportunities of the fifties, federal funds came roaring back so that by the end of the decade the US central bank was forced to reckon with what by then had already become standard operation. The results of the ’57 study, published in ’59, found:

Immediate availability of Federal funds, in contrast to the delayed availability of clearing-house funds, has given rise to other uses. A large part of all transactions in Treasury bills and other short-term Government securities is settled in Federal funds. Purchases and sales for the Open Market Account of the Federal Reserve System are also settled in Federal funds. The practice of settling a substantial part of Government securities transactions in Federal funds, which has become increasingly widespread, has drawn others than member banks into the market. Government securities dealers, as market intermediaries, have become important participants. Dealers in financing their positions often use repurchase agreements and buybacks to tap out-of-town money, and settlement is made in Federal funds, transmitted through the Federal Reserve leased-wire system. Other corporations, largely because of their securities transactions, find themselves in possession of or in need of Federal funds. They sometimes enter the market as buyers and sellers, usually indirectly by having their commercial bank act for them.

“Immediate availability” is what gave rise to the first instance of federal funds all the way back in 1920. One bank simply exchanged checks with another bank for the purposes of meeting statutory reserve requirements. The first bank, holding “excess” reserves, loaned them out to the second. The difference was in clearing each check; the one from the first bank being drawn on that member bank’s reserve account, thus funds presented immediately, while the second being drawn on the borrowing bank’s house or clearing account for presentation the next day.

What’s important to note for our purposes is why reserve account funds, these federal funds, could be immediately available. Because a reserve account was one held at one of the twelve local branches of the Federal Reserve System, there was no doubt at any point the Fed could meet any cash obligations arising from a depository claim – the Fed, after all, could simply print actual money if push ever came to shove.

That was, in a twisted sense, what was behind the resurgence of federal funds in the fifties onward. As that money market grew, so too did the implicit assumption behind it; that what was available to any federal funds claim was money printing, the presentation of them in a last resort situation that the central bank would have to meet by actually printing up Federal Reserve Notes if cash was otherwise unavailable to satisfy the obligation.

Not only that, banks in NYC had started to become once again money dealers in actively intermediating the flow of reserves throughout the country. Traditionally, call money had been the primary means of addressing “idle” bank reserves in money centers, but, owing to the aftermath of the Great Depression, the call money market had largely been banished in practice (though never forbidden). The opportunities of a greatly expanding audience in the 1950’s and really into the 1960’s opened up the possibilities for this new kind of money dealing.

It was developed into something called an “accommodating business” whereby NYC banks, only a few at first, started performing what amounted to brokered federal funds. They would buy and sell federal funds on behalf of their correspondents. This had the effect of attracting new volume into federal funds from the interior and across the US, drawing smaller banks into the burgeoning and increasingly modern style of interbank money markets.

It was often the case that a corporation took possession of federal funds via the sale of T-bills (a common cash management practice at that time) to securities dealers; they would acquire federal funds for their part of the transaction owing to the distinction in clearing and presentation of payment. Federal funds meant that the dealer would be paying in proceeds available immediately rather than a check drawn on a clearinghouse account that may take two or three days to clear. Companies in possession of federal funds through these transactions would then sell them to their banks which increased the volume, and sources of that volume, of money dealing intermediation.

The addition of non-banks to the periphery of federal funds was also abetted by repurchase agreements (repos). Non-bank deposit accounts as well as non-bank funding relationships were constrained by Great Depression-era legislations. Because non-banks were prohibited from direct participation in federal funds and banks were limited as to the interest they could pay on non-bank deposits, they began to use repos as a way of offering non-banks something like money market participation where they could be competitive in terms of offered rates. The bank would obtain a repo of cash or account from the non-bank, pay a repo rate slightly less than the federal funds rate and obtain a small, positive spread by redirecting into the federal funds market.

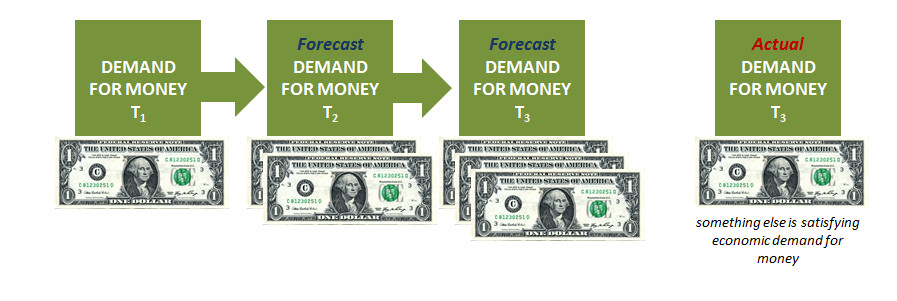

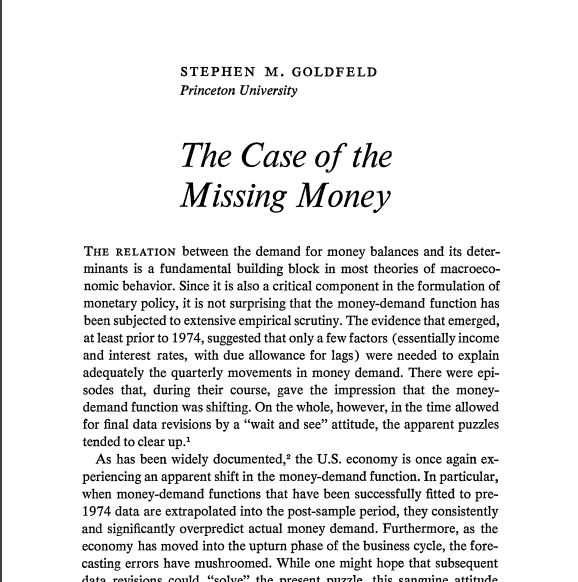

It increased the volume further in federal funds trading while also linking repos and the federal funds rate together. As that practice expanded into the 1960’s, so too did chronic usage. The system was using other things to carry out monetary functions, linking back to federal funds rather than cash, and it was becoming a broad-based practice (leading to Stephen Goldfeld’s “missing money”).

But if federal funds were a derivative claim on cash, then why not a derivative claim on federal funds (and then a derivative claim on that derivative claim, which was itself a derivative claim on the first derivative claim, federal funds)? They were an acceptable substitute for reserves of cash because the banking system, with implicit central bank approval, accepted them in that fashion.

Things would continue to move in that direction throughout the sixties and into the seventies. In February 1977, the staff of the US Congress’ Joint Economic Committee prepared testimony on the question of the eurodollar market (or Eurodollar, as they wrote it). Among the several key issues the panel was looking to explore was the impact of eurodollars on US domestic as well as global money supply. It was, of course, a hot topic being smack in the middle of the worst part of the Great Inflation.

The role of eurodollars in that inflation was, well, not very well understood:

Thus, an initial dollar deposit in a European bank can lead to a variety of outcomes. The amount of additional liquidity provided to nonbanks may be zero, equivalent to the deposit, or some multiple of the deposit. This uncertainty about who may be the borrower of dollars from a European commercial bank and how these funds will be employed raises the question of the size of the “Eurocurrency multiplier.”

The eurodollar was a non-reservable currency system for a reason, and the mystifying connections into and out of it was in practice much more than European banks. What that meant was that banks participating in the eurodollar market set the terms for what satisfied each other’s derivative dollar claims (you can pay my IOU with a different IOU so long as I accept that IOU because as another interbank participant you should have recourse to something dollar-related somewhere). As Ronald McKinnon wrote in 1977, quoting what Paul Einzig wrote in 1973:

Almost all Eurocurrency transactions are interbank, and most outstanding deposits are interbank claims, reflecting the highly developed intermediary role of the banks on behalf of their nonbank customers. Much like the spot and forward market for foreign exchange, these interbank loans “are unsecured credits, hence the importance of names attached by would-be lenders” ( Einzig, 1973, p. 19). [emphasis added]

The reason there was this hierarchy, of sorts, was because the eurodollar system’s fluidity and dynamism depended upon derivative IOU’s of derivative IOU’s. They might occasionally be backed by collateral as in repo, but by and large up until 2007 whatever one bank might dream up as a liability was taken as a satisfactorily resolving claim at whatever other bank would accept it. The inclusion of bank reserves, in the official Federal Reserve sense, was nil; thus, bank reserves up until September 2008 just didn’t feature because there had evolved no role for them.

That’s what an exclusively interbank monetary system means; that the banks themselves set all the terms of operation, all the protocols and standards for practice. The eurodollar system grew without bank reserves because it had evolved without any need for them; what the Fed claims is a reserve isn’t necessarily what the system takes for whatever might otherwise fill that role. It became a comfortable system set for perpetual exponential growth because it seemed to work and work very well; until it didn’t.

In short, the banking system through its modern wholesale evolution substituted its own format(s) for bank reserves that would satisfy its own liquidity rather than statutory requirements. The legal constraints for reserve balances had been all but expunged for all practical purposes once Basel re-arranged regulatory focus to the banking system’s asset rather than liability side.

The eurodollar system didn’t want those traditional bank reserves because they didn’t solve the need for the other types of liquidity “reserves” that had been created over the decades in the space where bank reserves had always been missing (my gas station analogy fits here). If you open the door to such robust qualitative expansion, you should not be surprised that what develops isn’t backwards compatible (and it argues that what’s most important is keeping up with the system’s evolution rather than assuming you can accomplish a lot with a huge dose of 1950’s policy).

That’s why in 2011, the Fed was stunned over a second global liquidity crisis (hitting not just the repo market) despite, as Brian Sack repeated several times during that discussion, the presence of “$1.6 trillion in reserves in the system.” The Fed was supplying something the system didn’t ever need; not up until 2008, nor, then, after that time.

They were reserves in name only, and were not eurodollar “reserves.” Therefore, the Fed printed bank reserves with its QE’s, not money. Everything else about the last decade falls into place for that one observation.

Stay In Touch