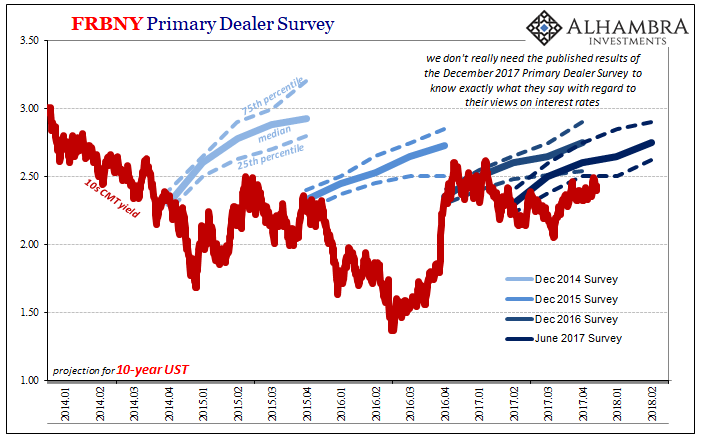

FRBNY’s December 2017 Primary Dealer survey results aren’t yet published, so we will have to wait a few days for the collection of those banks’ economists to tell us what they think their own traders likely won’t do. It’s a mess in that situation, but one as old as the crisis. Nevertheless, Economists for some reason still occupy prime slots in mainstream commentary opining about a great many things often year after year (after year).

One such is Blackstone Group’s Byron Wien. Mr. Wien is well-known throughout Wall Street and not just as the firm’s current Vice Chairman. He has a long and storied career in high NYC finance, having served two decades as Morgan Stanley’s often-seen Chief Investment Strategist once looming as a constant presence over the dot-com era with widely followed, and market moving, weekly essays.

Among his publications most people still follow is his annual “surprise” list. It’s a catalog of ten items, each one where Wien believes the larger public sees a slim one in three chance of happening which he thinks is actually better than 50%. His list this year includes:

With higher inflation, interest rates begin to rise. The Federal Reserve increases short-term rates four times in 2018 and the 10-year U.S. Treasury yield moves toward 4%, but the Fed shrinks its balance sheet only modestly because of the potential impact on the financial markets. High yield spreads widen, causing concern in the equity market.

It follows, as it would, his “surprise” that GDP growth and US wages accelerate this year (2018), following closely the narrative set out by Janet Yellen (in her less conflicted days) and many, many others. It may count as a surprise only in that very few might be inclined to believe it outside of the class of professional economic forecasters.

This far broader skepticism isn’t exactly unwarranted, of course. We need only look back to Mr. Wien’s list of 2017 surprises to see why:

Increased economic growth, inflation moving toward 3%, and renewed demand for capital push interest rates higher across the board. The 10-year U.S. Treasury yield approaches 4%.

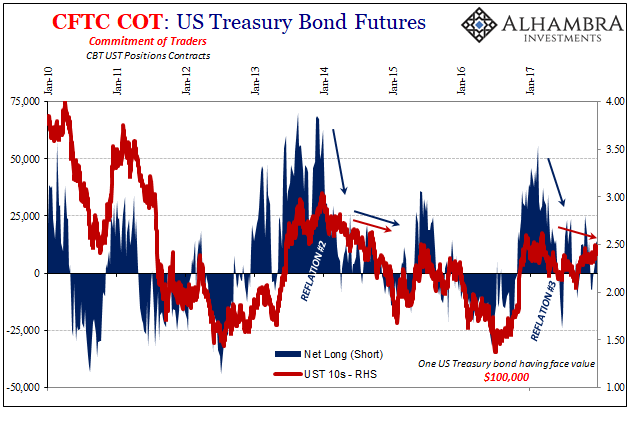

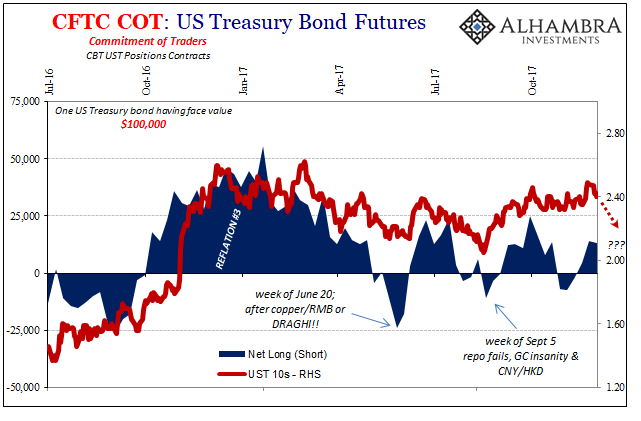

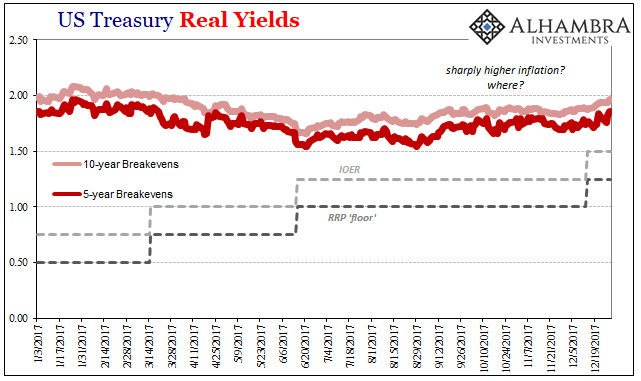

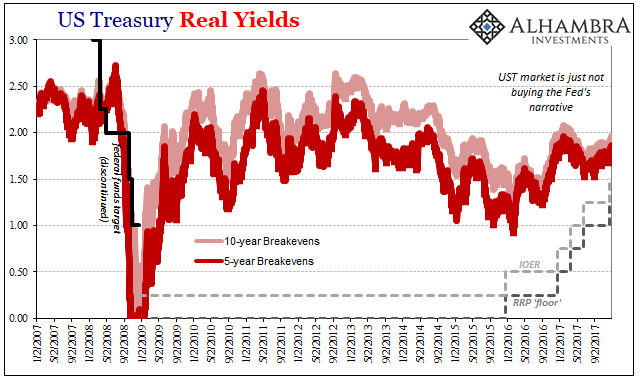

Interest rates have nowhere to go but up, except that they don’t. The reason is as simple as it has been since August 9, 2007, when the gaping distinction between dollar and “dollar” suddenly became all that mattered.

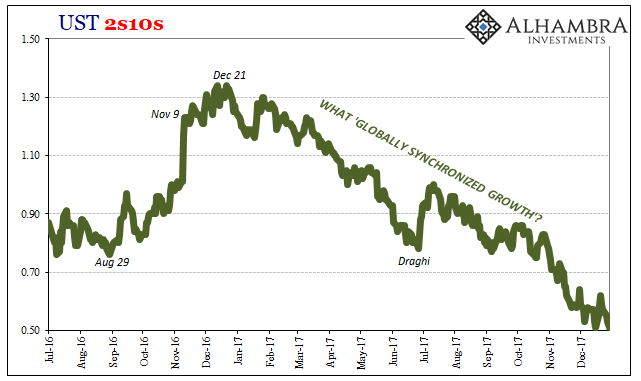

Last year was supposed to be the one of “globally synchronized growth”, where for the first time since 2007 all cylinders (meaning regions) of the world economy would be firing simultaneously, leading to so much momentum that nothing would stand in the way of actual growth this time. In reality, “globally synchronized growth” was only ever 2017’s updated buzzword du jour, the next iteration of 2014’s “global growth” or 2011’s “recovery.” It proved to be yet again all sizzle and no steak.

Even nominally bond bears were all but certain that 2017 would close out with the long end of the UST curve pushed up – if by no other reason than the (presumed) power of monetary policy in the US. In March 2017, for instance, “bond king” Jeffrey Gundlach described the UST 10s as trading in a “zone of death”, one that would see their yields first decline (they did) before making around 3% by last week (they didn’t get even halfway).

What it demonstrates is what I wrote early last year, in that inflation had become everything as it was representative of a great deal more than consumer prices. In other words, the bond market is very closely linked to the real economy through effective rather than imagined (QE) monetary conditions. That’s what everyone keeps understating if not ignoring outright; “dollars” not dollar.

None of this is strictly devoted to just inflation expectations or even inflation itself. Consumer prices are the monetary junction between money and economy. The shedding of the so-called inflation anchor (which can be observed in financial curves, too) is as much a commentary on economy and therefore the reversal of the Greenspan aura. It is a conclusion that the people seem to have arrived at several years in advance of policymakers…

It’s a truly amazing tale, which is one reason why very few choose to consider it even a possibility (especially by those in the media, who have been duped more than any others). For decades, the man so celebrated by all (at least most) the “experts” had no idea what he was doing? That US monetary policy had for all this time included little or no understanding and appreciation of money? It is almost too hard to believe; almost. It has taken some time, but with one lost decade already in the books, the Great “Moderation” starts to seem a very different thing, and the man who supposedly made it looks more and more to be the only one who was ever lucky.

The people who still view monetary policy of the nineties and aughts most favorably are the same who can’t figure out why these things never happen: growth accelerates, wages with it, inflation rises, and therefore interest rates too and not just the long end but the whole UST curve.

The market, by contrast, just doesn’t buy it (literally), and why would it? Going back to 2013, hell, even 2010 and 2011, these people have been talking about growth, inflation, acceleration, wages, recovery, etc., constantly. Now all of a sudden they get it right? Not only that, there’s no evidence right now, still, that they might be, a point even they have to concede.

No, we are to believe that all these things absent in the current data will just start showing up in 2018. Only they said the same thing, as noted above, about 2017. That’s the real message from 2017, all the “should be’s” that never were. Last year wasn’t strictly as bad as 2015-16 and that downturn, of course, but in many ways it was worse. Last year confirmed a lot about where things stand, meaning that in the grand scheme of things nothing has changed. Last year was supposed to be the year everything did.

Steadfastly refuting that narrative is where the long end of the yield curve remains (not to mention TIPS), exactly where it has been apart from brief “reflations” scattered here and there across the last decade. Until something substantial and meaningful alters this lamentable global (monetary) economic course, the only surprises are why Economists and analysts keep kicking this dead horse; at least it would be a yearly surprise if Economics was instead anything like a scientific rather than ideological endeavor.

Stay In Touch