Over the past two days, Chinese exports exploded, US payrolls bested 300k, and China’s CPI recorded the hottest inflation in 5 years. Globally synchronized growth? It’s times like these where remembering how nothing goes in a straight line helps settle and ground interpretations. In thinking that way already, you are never surprised when there are good even perfect data reports on occasion the way policymakers are always surprised with “unexpected” bad ones. We are in a global upturn, after all.

The question, as always, is whether these things represent a meaningful shift. The inflation/boom scenario is one where the economy doesn’t just meander at low level positives but accelerates forcefully into an inarguable growth period – something we haven’t seen anywhere for more than a decade.

It might be tempting to view this recent positive report cluster in that way, but, again, we’ve seen these before. It’s not just one month that is required to suggest what everyone is looking for. These have been over the past few years rather easily explained by outliers (China exports), noise (payrolls), and statistical difficulties (China CPI). We will know things are truly picking up when the bad months are what become attention grabbing for their infrequency.

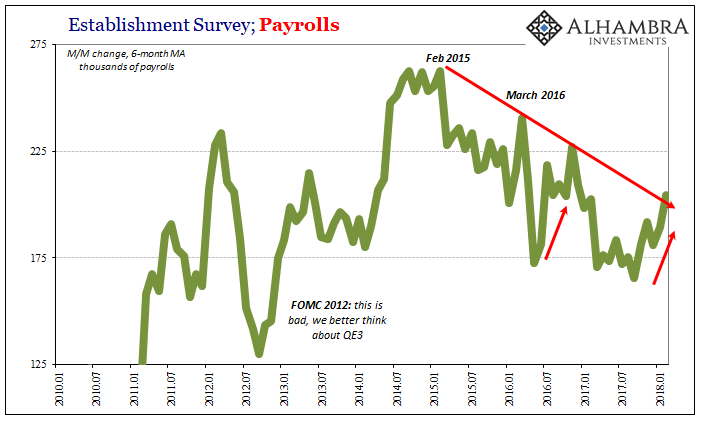

Each of these data points deserve individual examination, so I’ll leave the two China series for later. Taking US payrolls first, it was a nearly perfect report. That in itself tells us very little. These had been almost common in 2015 and early 2016. As I wrote in January 2016 for the December 2015 BLS estimates:

I think it entirely fitting, even useful in the long run, that December’s payroll report was yet another perfect month; the fourth of 2015 by my unofficial count. There was absolutely nothing wrong with any of the components, at least in the raw job count estimated by various statistical regressions and adjusted with imputations (wages, not so much). The problem with surging labor statistics becomes obvious in the context of everything not labor-calculation related. Does anyone really buy that the economy shifted so much higher, and in December of all months?

People relying on just the monthly noise of the payroll reports might have been shocked by what was happening in early January 2016 – the very worst of a global economic downturn that though milder in its impact on the US was taking a heavy toll across the rest of the world. Perfect payroll reports are nice, I suppose, but solely for entertainment purposes so long as they are uncorroborated by other data, or even just other months.

The other big problem with the current BLS figures for February 2018 is that +311k sounds impressive but it shouldn’t. It does only because the labor market is just that weak. What I mean by that is any reasonable standard for meaningful growth is so far above what we have become accustomed to. It’s not that the labor data is misleading on its face, it’s that the interpretations of them haven’t been re-calibrated properly for the last decade.

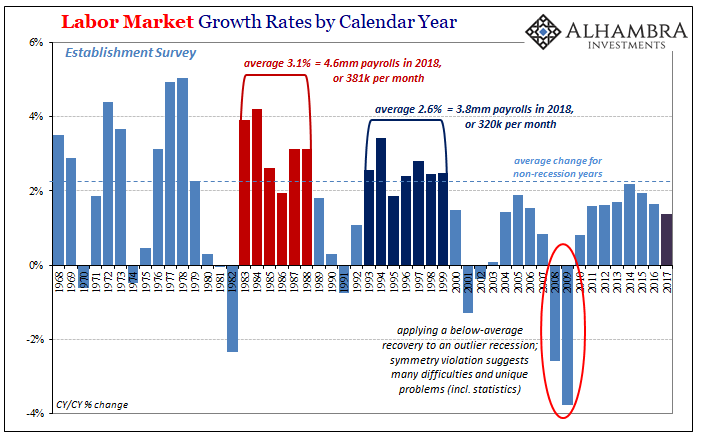

Using the averages for the late nineties, the Establishment Survey if it represented solid growth would gain almost 4 million payrolls in 2018. That would be an average of 320k per month. The latest estimate for 311k is actually below average. That means everyone is celebrating as some kind of blowout what would otherwise fall as a weak month under more reasonable analysis. That’s how bad the labor market has been for so many years.

And it’s an outlier, but it’s not the first. The BLS data shows that in June and July 2016, for example, payrolls gained +285k and then +325k, respectively. Taken in isolation, those two “blowout” months seemed to suggest economic acceleration in keeping with the “reflation” sentiment that was then just forming. We know, for that labor market anyway, those two perfect reports were quickly forgotten, mere statistical noise that represented instead more of the same – the good months, even two in a row, are the exception.

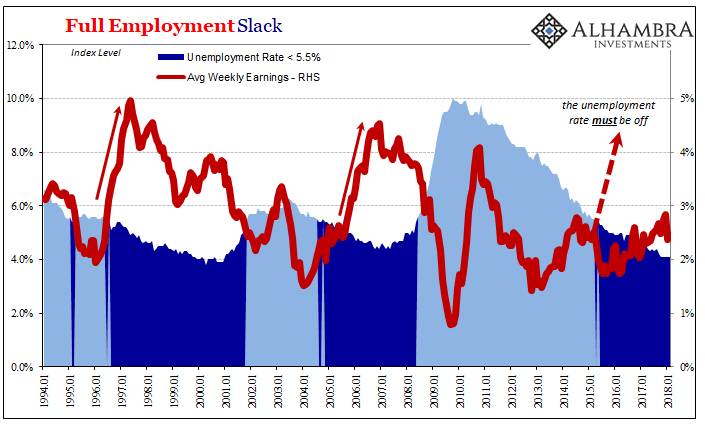

If you go into each monthly report believing the occasional below average month (rather than the more frequent way below average month) is a good sign then stubbornly lackluster wage and income growth is some big mystery. Average weekly earnings, which are even more noisy month-to-month, rose just 3.2% year-over-year in February after being nearly flat, +0.8%, in January.

Despite the unemployment rate sticking at 4.1% for the fifth straight month, there isn’t the slightest hint that earnings let alone wages are accelerating; nor is there any indication they are about to.

Even perfect payroll reports aren’t without questions. The unemployment rate stayed at 4.1% because of a sharp rise in both the labor force (which is a good sign, or it would be) on the denominator as well as a big jump in the Household Survey (numerator). The Household Survey gained +785k last month despite +729k in full-time employees and an additional +292k in part-time. This flips from January when the HH Survey gained +409k even though FT was +293k and PT was just +14k. The sum of FT and PT don’t equal exactly HH, but they should be close(r).

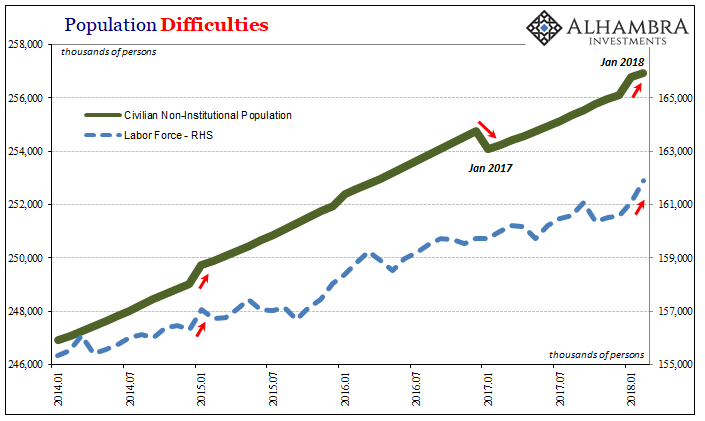

Part of the problem, especially with the labor force estimates, is that the Census Bureau contributes, so to speak, data discontinuities in the population sets at the beginning of many years. It can at times throw off the monthly progressions. The Civilian Non-institutional Population, for instance, has been interrupted in each of the past two years, in 2017 by a discontinuity where population growth throughout 2016 was less than originally thought.

Population growth last year, apparently, was more than previously believed in estimates released during it. The BLS is then forced to fit their population sensitive series into those discontinuities, which then makes year to year interpretations meaningfully more difficult.

The labor force has grown over the first two months of 2018, but by how much? Same question for the HH Survey.

The Establishment Survey doesn’t have as much of these problems, which is why it is the preferred indicator for economists and the media. It is more managed and smoothed out so as to eliminate these possible gaps, but it cannot eliminate all the noise inherent in this kind of statistical enterprise.

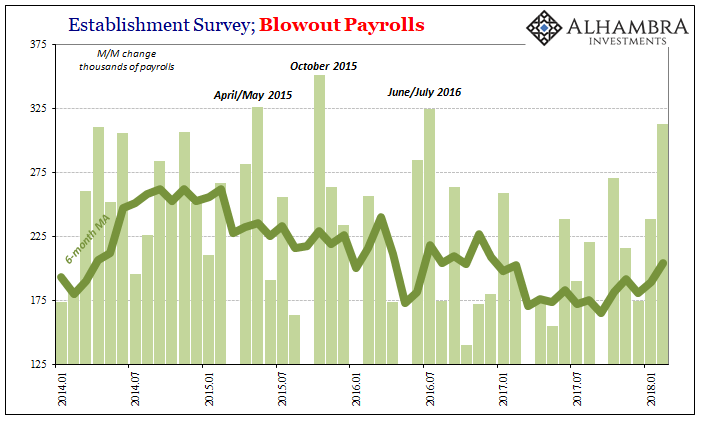

That’s an important point for the last six months of data. The average has increased over that period, culminating, obviously, in this latest “blowout” month for February. Is that the usual noise that we’ve become used to as noted above? Is it the beginning of the labor market finally stabilizing after three years of slowing? Or is it Harvey and Irma?

It’s hard to ignore when the bottom in the average was September 2017, the month initially thought to be payroll negative due to the immediate impacts of Harvey in particular. Since then, like so many other economic accounts, the Establishment Survey has registered some increase. Given the inherent lags economy to employment, it is possible that what’s indicated in February is the trailed effects of the artificial hurricane boost.

This is where the noise works against us (like the middle of 2016). There is, right now, simply no way to tell. If it is the aftermath of the storm aftermath, then over the next few months it will not be unexpected if the payroll reports soften again. Not only is that the still-indicated baseline, by weekly earnings especially, those other economic accounts have already started to roll over moving further in time away from last year’s tropical disruptions.

Jerome Powell and the Fed’s Greenbook claim there is wage-driven inflation imminent. On the surface, +311k makes it seem like he could be right. However, until +311k is proven instead to be rather weak by regular +350k or more, then it isn’t that wage-driven inflation is unlikely, it’s just not possible. The occasional +300k is still huge slack.

Stay In Touch