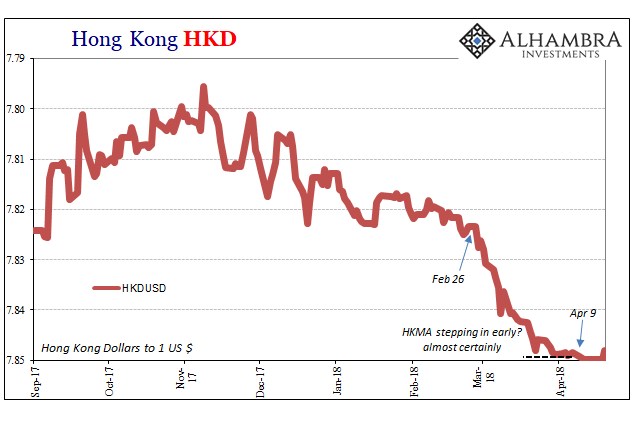

Today for the first time in over a week, HKD moved. That’s not unsurprising, as we should expect that nothing goes in a straight line – even devaluation of this kind. The issue is more about why it might have moved, or what it cost to move it.

The Hong Kong Monetary Authority (HKMA) had started carefully. They were only buying HKD in small amounts at first. This week, however, they stepped up their operations. Through April 18, HKMA had sold $4.3 billion in US$ reserves, half of that total on the 17th and 18th alone. Today, the monetary board acting now as de facto central bank has sold $2.2 billion more.

There have been 13 operations and $6.54 billion already spent. It’s a drop in the bucket compared to the level of forex reserves in HKMA’s exchange fund. As of March 31, the authority reported HKD3.24 trillion in foreign assets, net of HKD352 billion of liabilities (repos and securities lending arrangements). That’s about $412 billion.

Given the size of the stockpile, most media commentary is of the same comforting tone – nothing to worry about. It’s this laziness that is most frustrating, as if nothing interesting has happened over the last decade with regard to central banks making the same claim. You would think that the media would notice how many times central bankers have been unshakably reassuring only to be severely shaken themselves (China and CNY being a pretty relevant recent example).

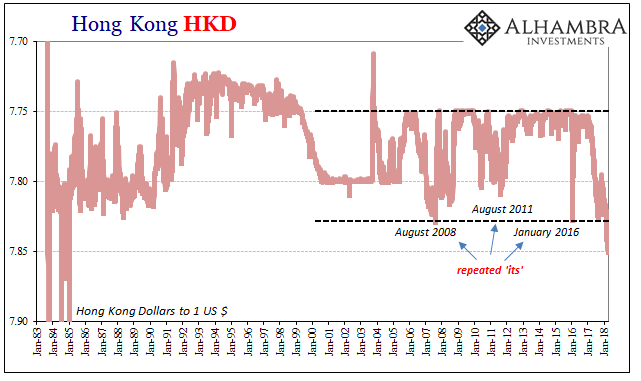

Maybe the fact that we are talking about Hong Kong makes a difference this time. After all, the whole point of HKMA was its stability, and the predictability of its monetary and financial arrangements.

Over the years, the HKMA was tested a few times, especially during the Asian flu of 1997 and 1998. Unlike its Asian neighbors, Hong Kong never came close to devaluation and economic destruction, even as China took over sovereignty amidst its own Asian flu symptoms.

It earned the HKMA and its HKD currency a quality that is so often unappreciated in modern times: boring.

Yet, here we are in 2018 and that’s exactly what has changed. HKD and the HKMA have suddenly become very interesting.

To that end, $6.5 billion, or 1.6% right at the start, is even more fascinating. You might even start doing a little back of the envelope math on run rates. Recent history has shown sanguinity the wrong play. I don’t doubt that HKMA officials actually believe they have it totally under control; they all believe that in the beginning (subprime is always contained). Many still believe after it is over.

To do so, they need only tell themselves “it” was some exogenous factor beyond their control. That works if you are a central banker lacking conscience (which you might mistake for courage if you do actually lack conscience), but that accomplishes nothing for those exposed to the numerous and repeated “its” (i.e., everyone). There shouldn’t be any, but with almost measured frequency there continue to be despite all assurances, reassurances, and often outright denial.

You might have even drawn the conclusion from all these “its” that central bankers don’t know the first thing about money. Shocking, I know. Interesting, too.

Stay In Touch