Inflation hysteria was primarily focused on the bond market. While it had political elements attached, mainly the desperate attempt to discredit the basis for populist discord, mostly it was a bond bear thing. The economy especially in the US was about to finally live up to the unemployment rate, the hysterics claimed, which meant an explosion in wages therefore inflation, and finally Jerome Powell’s confidence to go faster and farther with the federal funds rate.

All these things were to produce an epic, biblical BOND ROUT!!!! The flattening of the yield curve was a loud if partial rejection of that thesis. This was ignored partly because of blatantly dishonest economic commentary and partly plain economic illiteracy. And when it comes to financial curves, the dearth of understanding them is near total.

You might wonder how this could be, though the answer is very simple. Economists are not taught anything relevant about how the bond market works in the real world. They aren’t taught much about economy, either. Rather, they spend their time in equations taking advanced mathematics courses that at some point was supposed to help them better map out economic processes.

Somewhere along the way, very early on in the discipline’s turn toward Positive Economics and econometrics, they started to appreciate only the math at the expense of competence about the economy. I would put the approximate date for this transition somewhere in the 1960’s certainly completed by the 1970’s with Robert Lucas’ invention of rational expectations theory. It’s been downhill from there.

This is why in the most crucial period in the economic and financial history of the last four generations, eighty years by then spanning back to the Crash of ’29, the Economists at every central bank could stare into the face of very dire financial and money market warnings and completely ignore them. It is form of corruption born of illiteracy predicated on self-selected ignorance.

Having learned nothing from the incident nor the constant reminder of the ongoing aftermath, here we are again with markets saying one thing that “experts” all claim is another.

The latest example comes to us from Bloomberg (of course) in the form of a story that starts out like so many others in the right way.

Bonds in Indonesia, India and Australia are witnessing a flattening of yield curves that’s showcasing the challenges these formerly-favored markets face as dollar liquidity tightens.

In many places, central banks have either intervened or raised rates to address eurodollar insufficiency. The upward pressure on short rates ends up balanced against a recalcitrant long end – very much like what’s happening in the UST market and its curve right now.

These are not contradictory signals, however. The long end in India or Australia, for example, is merely expressing pessimism about what may come out of the very serious stuff at the front. A sharply flatter curve in this way is a harmonious and unmistakable alert, one which the Bloomberg article to its credit at least picks up on.

But then it ends, as they usually do, on a happy, optimistic note. Nothing can stand in the way of the recovery narrative. In order to downplay the warning of the one curve in Australia we must ignore the US curve’s similar testimony to be able to arrive at the same typical nirvana of nothing to see here.

“The developments in short-term funding rates are directly affecting the outlook for the yield curve in Australia” by “pushing short-term yields higher and thus creating pressure for the curve to flatten,” said Tamar Hamlyn, a Sydney-based principal at Ardea Investment Management, which oversees A$10 billion ($7.4 billion).

However, “as the U.S. recovery continues and yields there continue to rise, all else equal this will have a steepening influence on the Aussie yield curve,” he said. That echoes a view held by Grant Samuel Funds Management.

The US unemployment rate is now supposed to rescue Australia and India, too? The US curve(s) aren’t playing along with this scenario – at all. The UST curve continues to flatten much worse than in these other places, and more than that there is already inversion in places like eurodollar futures. Indeed, what’s going on eurodollar futures only helps confirm the underlying “dollar tightening” thesis the article adheres to only as a way to setup this strawman.

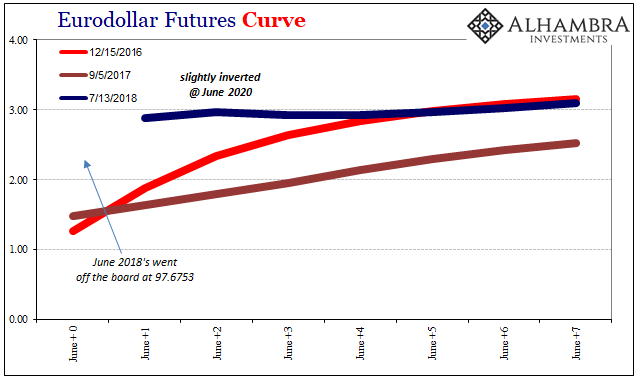

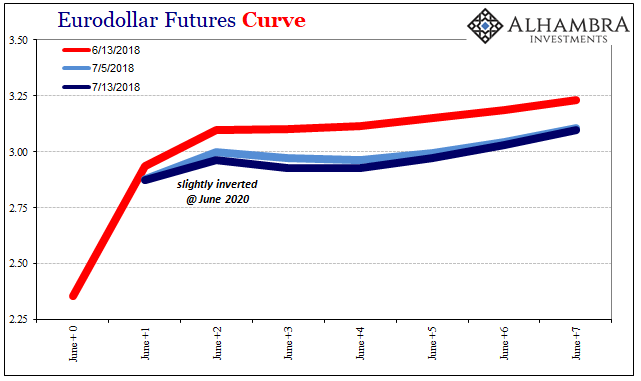

The eurodollar curve actually inverted in the middle of June. It wasn’t really noticeable, and thus confirmed, until last week. It started off at fractions of a basis point between the June 2020’s and 2021’s, but has grown steadily though incrementally ever since. Exactly one month later, the difference has increased to 4 bps in trading today.

The contortions shown above are decidedly negative. In fact, we are right on the precipice of the June 2022’s inverting further with respect to the June 2021’s. They are right now equal, but several times over the past week they have been fractionally lower.

In short, the eurodollar futures market view is that there is a real nontrivial chance of something.

So, what is this something? The shallow nature of mainstream commentary and the experts quoted to shape it go no further than to equate inversion with recession. It’s a comforting diversion because in the UST curve form of inversion that might mean a recession no closer than 18 months and more like 2 years in the future. A lot can happen between now and then.

That’s not what eurodollar futures are indicating, however. These are money curves. Like early 2007, they are saying there is a growing chance the Fed is going to have to reverse itself; interest rates at the short end that are supposed to be rising and then remain raised aren’t being viewed that way. Inflation hysteria posited that the US central bank would have to become more aggressive whereas the markets are pricing something else entirely. Right now its a still-cautious Fed that will end up going the other way anyway.

We need only go back to 2007 when FRBNY’s Open Market Desk Chief at the time Bill Dudley made his absurd rejection of the same kind of warning.

MR. DUDLEY. …they [Economists] advised me not to take what was going on in the Eurodollar futures markets literally because they felt that some of them [traders often at the very same banks as the Economists] were putting on these positions in case of a bad scenario that led to significant reductions in short term interest rates.

Yes, it is this “bad scenario” that is causing futures investors to increasingly hedge against it. For now, they are doing so in the 2020-22 contracts, but that doesn’t mean they necessarily expect those years to be exactly when all this happens. The curve shape is not meant to be taken literally.

Participants are growing concerned about a future problem that they feel requires some increasing level of protection, and it may just be those contracts are where this protection is most available at the market-clearing price. At just a few bps of inversion, what should be noted here is some future “bad scenario” whose outlines don’t yet show up on this side of the horizon. What’s going on with inflation hysteria and Jerome Powell’s intractable viewpoint only muddies that horizon.

If things continue on as they are, including yield curve flattening all over the world, it may be that the June 2020’s get bid so that they eventually invert with respect to the 2019’s; and some of the 2019’s with respect to the 2018’s. We don’t know when this “bad scenario” might occur or yet how it might develop, but we can at least say that it isn’t just rhetoric like “the U.S. recovery continues and yields there continue to rise” stuff.

The eurodollar market, like the treasury market, is incomprehensibly deep. For something like this to register within it, a clear and palpable distortion to what should be a smooth, uniform recovery curve, it can only mean there is something like broad worldwide consensus forming that this isn’t something to just ignore. Again.

After eleven years, I doubt that so much widespread economic illiteracy will be solved given how much curves remain such an unnecessary enigma. And I haven’t even mentioned for the nth time that all this is taking place at and now less than 3% nominal. There is nothing good in these curves and it is spreading.

Stay In Touch