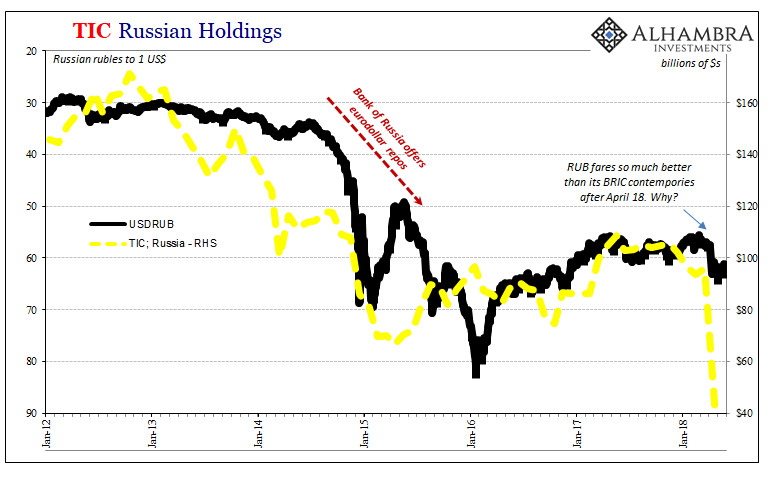

The Russian ruble has fared far and away much better than its EM peers. Compared to something like the Brazilian real, there is no comparison. The ruble has been relatively steady following an initial drop in April with the imposition of sanctions. April 19 came and went, and while that date is displayed prominently across all the key currencies it meant nothing for Russia.

It may be that oil’s continued rise in the face of eurodollar tightening is offering RUB some amount of protection. The Russian economy isn’t much more than its energy sector. It already experienced the wave of deflationary devastation with the advent of 2014’s “rising dollar” – which decimated oil prices. So far this time around, this prospective Eurodollar Event #4, it is different in that regard.

While oil could offer a plausible premium in the ruble unavailable to other struggling currencies, I have to believe there is more to it. It smacks of intervention, particularly the narrow range RUB has traded within despite some crucial potential interruptions (May 29, for one).

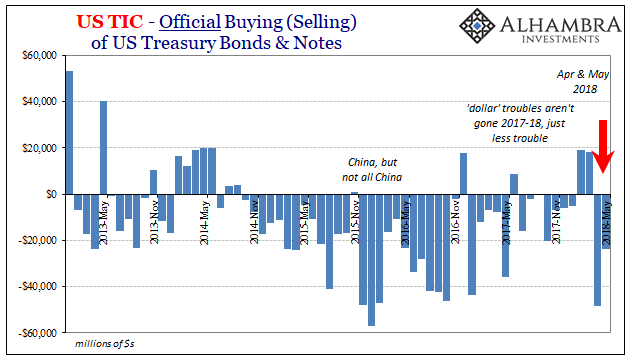

The Treasury Department’s TIC figures offer some tantalizing confirmation along those lines. According to the report for May 2018, released today, the Russians have nearly run out of UST’s. Well, they haven’t run out so much as the balance has been run down to less than $30 billion and therefore no longer qualifies to be disaggregated as an individual line. They are now part of “All Other.”

However many UST’s the Russians have left, it is interesting, and telling, that the level has collapsed during these specific months of April and May. Russian officials, almost certainly with the experience of the “rising dollar” burned into them, are possibly being hyper-proactive about the ruble, meaning the eurodollar’s tightening grip.

How much they have left in the bag after some heavy “selling UST’s” already isn’t known but judging by RUB’s behavior in June and so far in July they have some ammunition left at their disposal (and it may be that these UST’s disappeared from the TIC figures have merely been shifted to other accounts that don’t register in the custody data, therefore theoretically still available in official channels for mobilization and use).

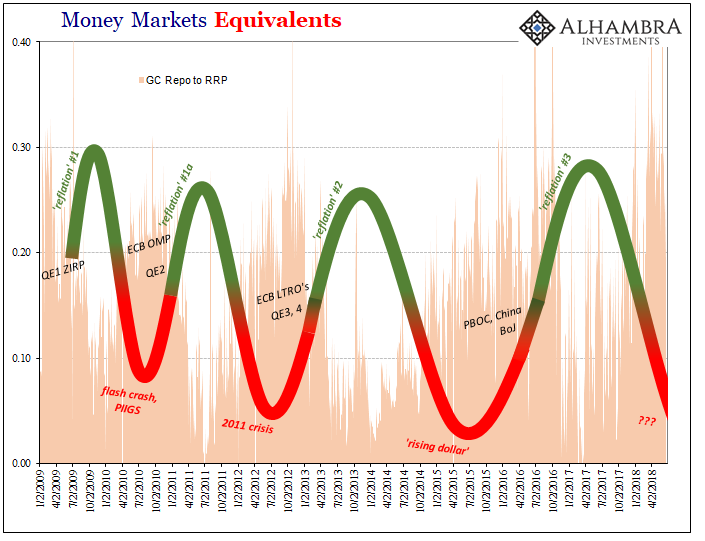

It’s some interesting speculation for how Reflation #3 might be increasingly in the past. Elsewhere in the world, the same tendency is showing up and in more crucial spaces than Russia. That, of course, means China and CNY.

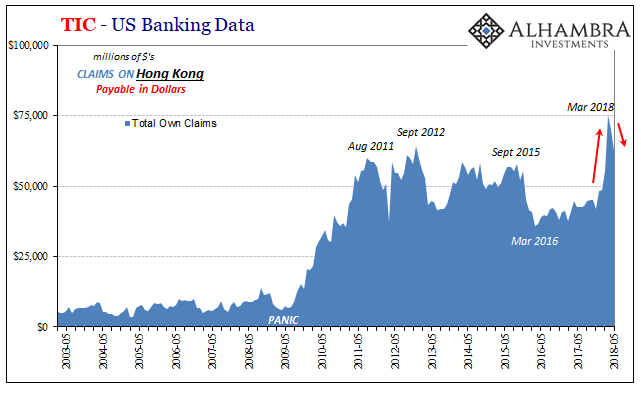

And thus HKD. I wrote last month:

Now, in April 2018, has HK reached something of a limit or barrier? HKD would suggest as much, as does now TIC. The consequence of that appears to be 6.50, or worse (remember: CNY DOWN = BAD).

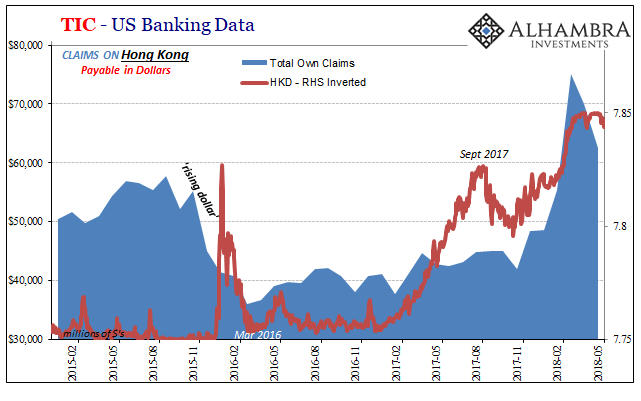

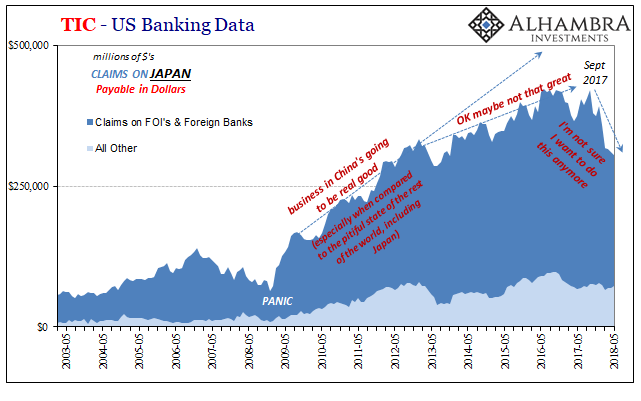

We have supposed that on the other end of Hong Kong supplying some good proportion of those “dollars” is Europe’s banks. In 2017 for the first time since 2011, banks in that jurisdiction increased their presence on the other side counterparty to US banks – which proposes that European banks have been more active in offshore “dollar” markets overall. That may or may not include HK in their renewed propensity toward money dealing, though it is a reasonable inference nonetheless (there simply aren’t any figures for dollars moving between European banks and those in Hong Kong which bypass the US, and US data, entirely).

Sure enough, TIC figures show a further drawdown in HK dollar activities. Like Russia and RUB, HKD and TIC for Hong Kong continues to suggest 7.85 as a hard limit. The net effect of that limit (banks unable to be compensated for the increased risk of lending toward China, any part of China) is the further closing off of that important eurodollar bypass into the mainland.

For China, what other choice is there but for CNY 6.50 now 6.70 (and today a shock flash crash almost to 6.80).

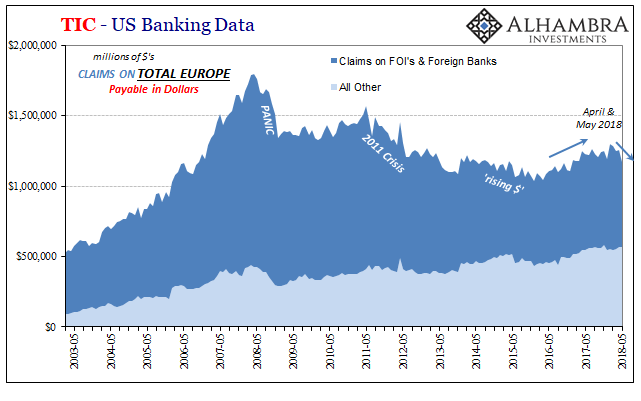

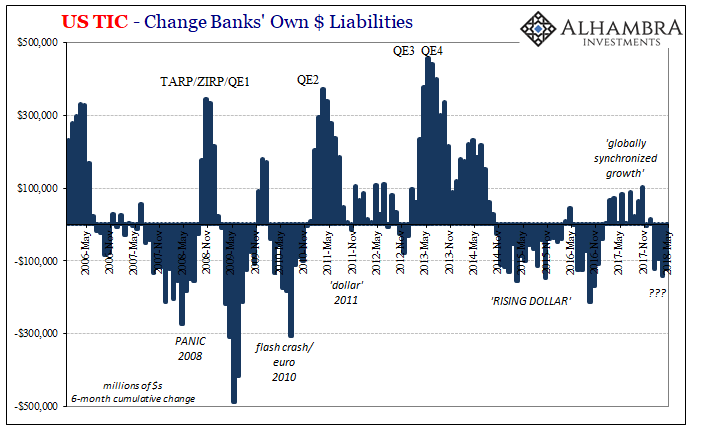

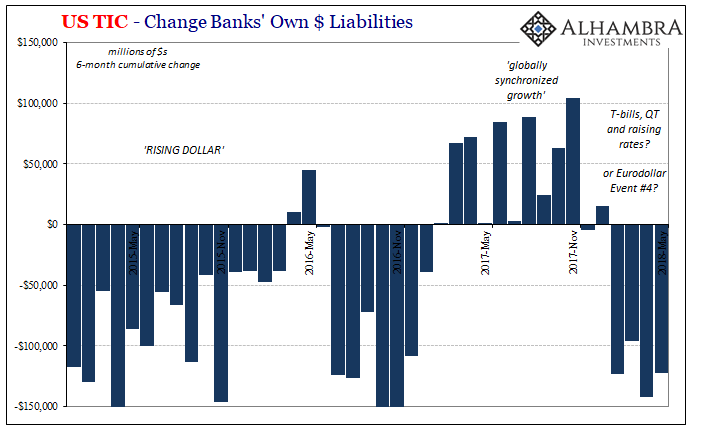

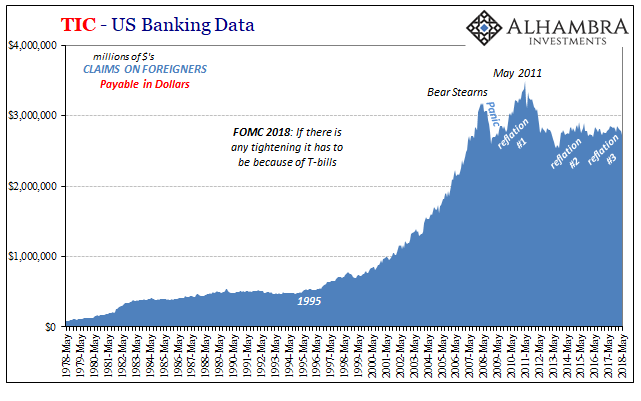

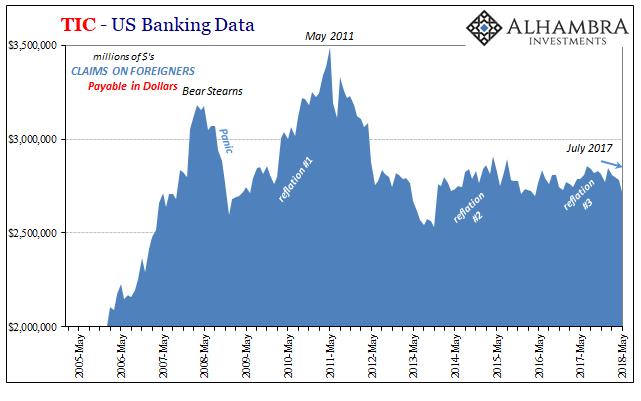

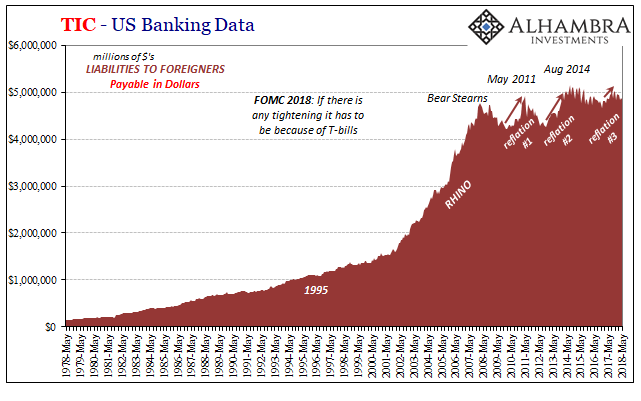

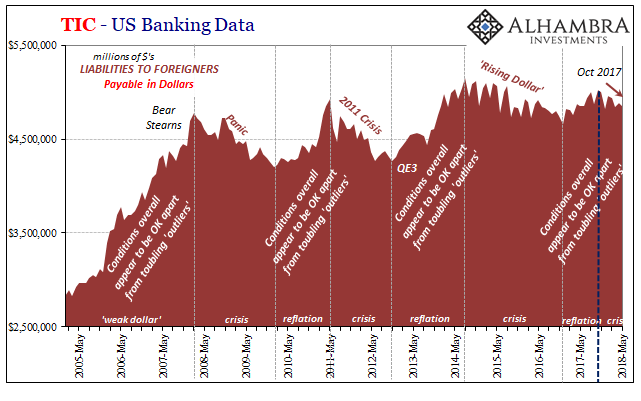

On the flipside in Europe, the banking data from TIC again conforms to our thesis. European banks were withdrawn in May by a rather large amount (as EUR fell). The balance in this one view of offshore dollar capacity was brought down to the lowest in more than a year.

Without the Japanese to depend upon for some alternate or emergency funding channels, in FX dollars, who was left but central banks in April and May to try and stem the rising tide of the dollar (or re-rising tide)?

The further we go into 2018 more and more it appears likely that Reflation #3 had some time ago reached its end. It may not have in everything, but where it matters to start with in these offshore eurodollar spaces there has been enough time to propose a shifting trend back toward the bad stuff.

It doesn’t matter which form of bank liability data in TIC, the pattern is becoming pretty clear, uniform, and sadly recognizable.

Reflation #3 is disappearing even after having been so much shorter and smaller than any of the others. I think that’s because there wasn’t really much behind this one to begin with. Reflation #2, for example, had Draghi’s promise as well as the Fed’s QE3 and QE4. While those didn’t actually change effective liquidity conditions, they did create the positive sentiment that is the basis for these reflationary periods (which is why they eventually flicker out with such an unsatisfying whimper, you can’t gain economic or monetary recovery on sentiment alone).

In 2017, by contrast, the only thing pushing any positive action, reducing negative “dollar” pressures, was this almost laughable idea of globally synchronized growth. That was it. Put that basis together with the increasingly jaded nature of markets (why the important curves flattened at only 3%) and it meant Reflation #3 was only ever going to be minimal. In most of these TIC figures, it barely registers (just ask the Chinese, suggesting why the whole HK ruse in the first place).

Now it doesn’t register at all.

As with other indications and curves, I think that puts the eurodollar system in the red but still not quite yet into the deep red of self-reinforcing negativity. Banks worldwide are almost surely pulling back, perfectly consistent with the deep currency crisis already on display since April. There aren’t widespread confirmations that they are running for the exits.

What happens now is ramping up of countermeasures by overseas central banks, something we’ve already seen this month with interventions spanning the globe – especially Big Mama. Inevitably, they accomplish nothing of value only buying time though for no true purpose; this “dollar” issue, as if you haven’t figured out by now after eleven years, is the same thing repeating over and over. In other words, it is a chronic condition that can’t be overcome let alone solved by any individual action.

What I wrote yesterday applies in light of these figures:

The world was fooled into thinking that everything was fine and that all this other stuff that wasn’t fine in 2013 was just a rough patch to be easily smoothed over by the successful completion of a global recovery… That’s what believing in the taper tantrum did to the world, leaving it blind, and wholly unprepared, for what was about to happen.

SSDD. Taper tantrum and now QT tantrum? Nope. Eurodollar Event #4 will have been perfectly predictable and yet no one will have seen it coming.

Stay In Touch