Why did inflation hysteria die? The answer is surprisingly simple. Proponents way oversold the thing. They kept claiming that the labor market, via a truly booming economy, would force the Fed’s hand. Wage growth was about to explode, therefore monetary policy couldn’t afford to be complacent. Aggressiveness was about to become Jay Powell’s go-to position.

This year is now more than half over and…?

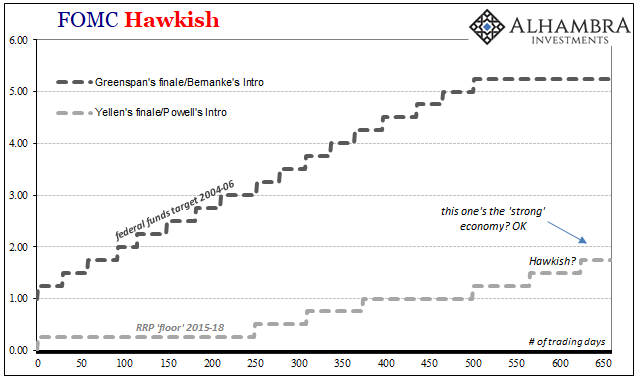

With the FOMC once again refraining from action, you might begin to wonder what all the fuss was about. The economy of the middle 2000’s could hardly be classified as robust, yet that didn’t stop Alan Greenspan’s Fed (finished up under Bernanke) from “raising rates” at each and every meeting; seventeen in a row, in fact.

Janet Yellen used the term “false dawn” in 2014 and it has dawned on an awful lot of otherwise sympathetic people and investors that there is the nontrivial chance this could be still another one. The fact that Powell isn’t even managing half the pace of Greenspan is more instructive than many seem to realize.

Officially, the FOMC upgraded their economic assessment. One of the only changes to the latest policy statement was foregoing a “solid” characterization of economic activity in favor of “strong.” These are, obviously, subjective terms subject to interpretations. The market’s interpretations aren’t being received kindly of late.

That’s the problem. The market was expecting the economy to live up to “strong” starting with this huge, massive, overhanging LABOR SHORTAGE!!! People are right to ask seven months into 2018, where is it?

Today is one of those days that policymakers would probably wish other government agencies would refrain from spoiling their statements. The most laughable was in December 2015 when for the first time in almost a decade Yellen finally moved, and that move was promptly overshadowed by the very same central bank publishing an Industrial Production contraction (a recession signal) simultaneously.

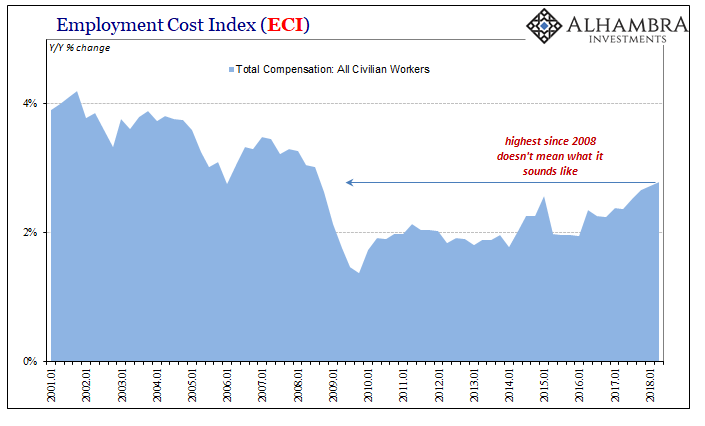

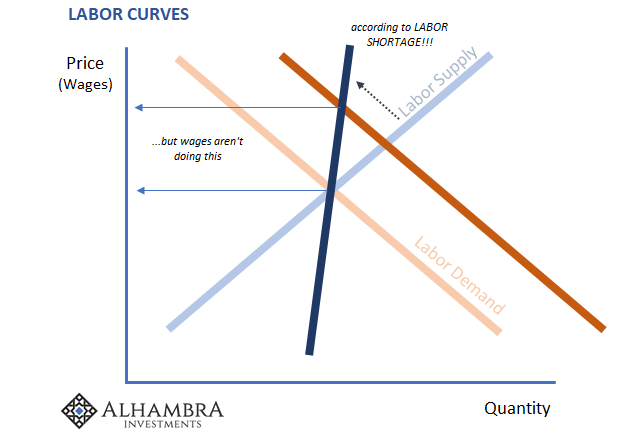

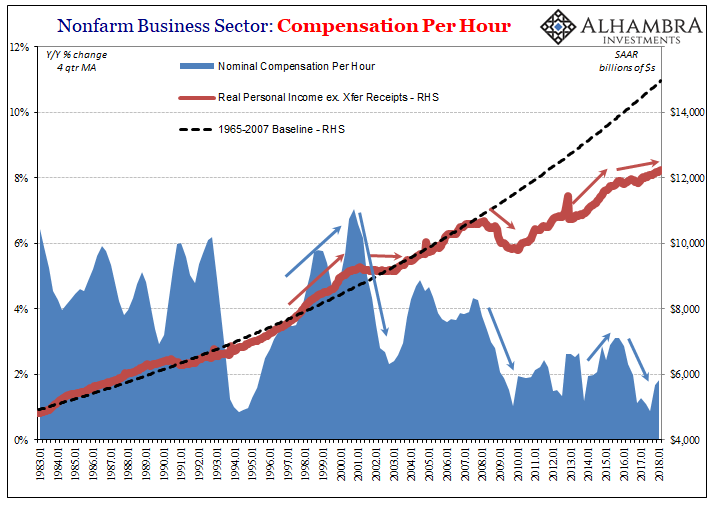

If the LABOR SHORTAGE!!! is going to make the Fed more aggressive, then it’s absence among potentially corroborative sources would do what? The Bureau of Labor Statistics (BLS) reports that the Employment Cost Index (ECI) rose 2.78% year-over-year in Q2 2018, the highest rate since 2008. That’s the good news. The bad news is that it rose by 2.78%.

That rate is practically unchanged from Q1’s 2.71%, or Q4 2017’s 2.66%. For a booming economy that is reported to be drastically short of available labor, this is hardly what one would expect to find in the price of labor.

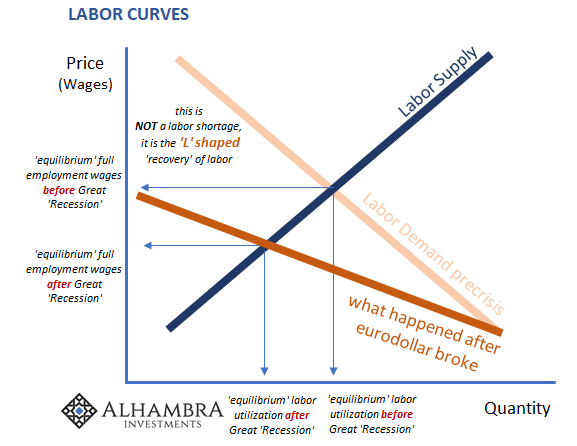

It’s even more contradictory given that 2.78% is substantially less, still, than the pre-crisis era. Rather than providing evidence for a booming economy, this crucial picture of the labor market shows us instead how it shrunk in 2008 and has never come back. The unemployment rate, therefore, can only apply to the shrunken piece, not the overall level.

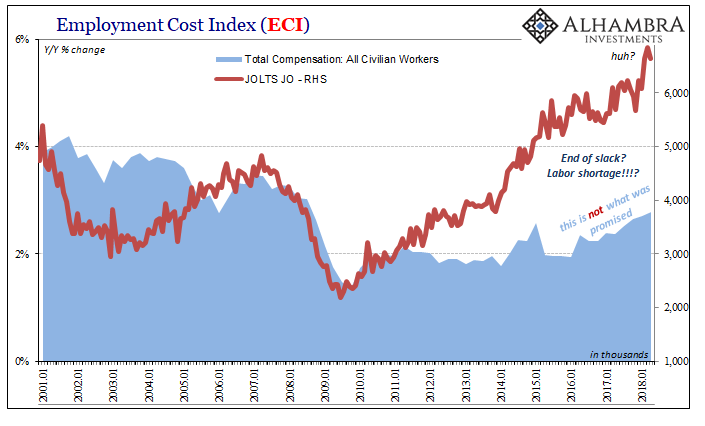

The pace of compensation is equivalent to the rate of hiring in the US economy. That’s also the bad news since the level of hires, according to separate BLS data (JOLTS), remains considerably less than it was. Again, shrunk.

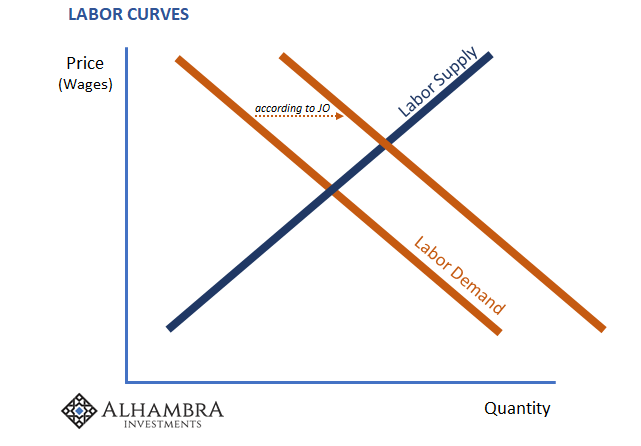

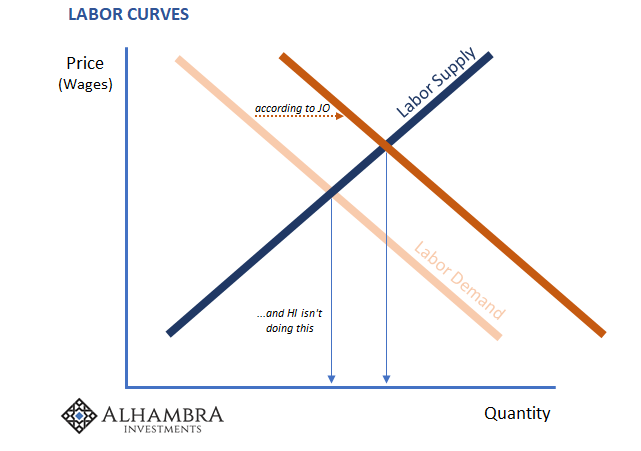

But Job Openings!

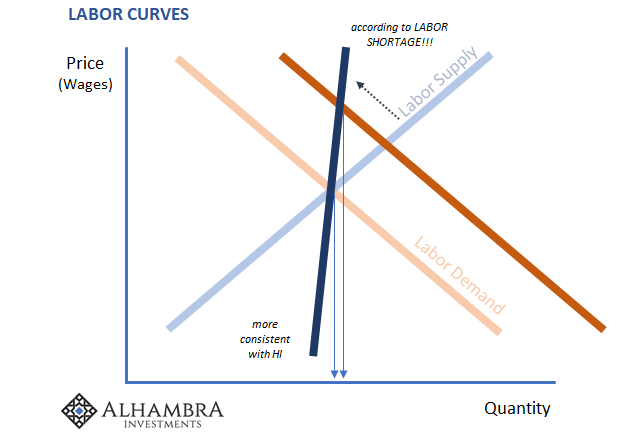

If the price of labor was accelerating as was promised, then the difference between JO and HI would be consistent with an actual labor shortage – rapidly rising JO as demand for workers and stable to depressed HI as the inability of employers to find them. Instead, as determined by basic economics (small “e”), all JO suggests is that employers are using more online advertisements per position than they used to.

That’s it.

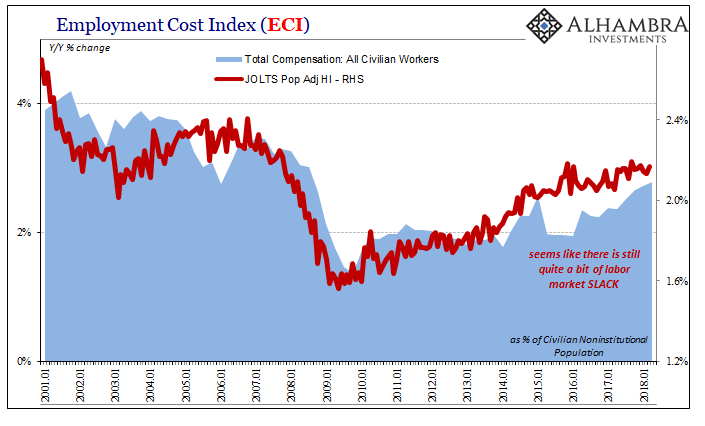

Supply and demand curves don’t lie, nor do they subjectively determine themselves as “strong.” Inflation hysteria died from a steady diet of nothing but strong. The last two charts of the set below are all Jay Powell would need (even with revisions for “underreported” income).

Stay In Touch