What is it that’s different in August? If there was some relative calm in global markets in June and July it certainly disappeared this month. The dollar shot higher and global liquidity indications began sinking again. Yields have fallen on safety (liquidity) instruments more apparently divorced from any other mainstream factors.

One place to look for answers is Tokyo. I wrote at the beginning of July during what seemed like a lull:

It doesn’t mean, however, Japan is out altogether. Far from it. Japanese banks are still in the eurodollar business and tied to China. Like some mafia family organization, once you are in there is no getting out, at least not all the way. They can cut back and turn off some of their activities but not all of them. There is still very much a “dollar” redistribution business running through Tokyo.

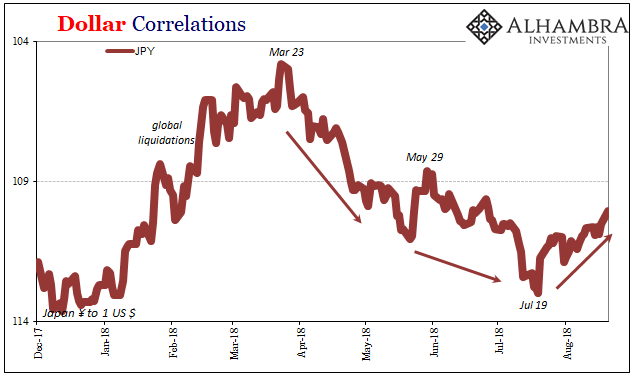

That would be, for me, one indication of moving deeper into the red at least as I sketched out these reflation/deflation cycles last week. If JPY were to suddenly and sharply move inversely to CNY, it might propose those kinds of self-reinforcing behaviors that are down at the worst of things.

Inverse to CNY would mean, obviously, JPY rising as CNY falls. Sure enough, here’s JPY since mid-July:

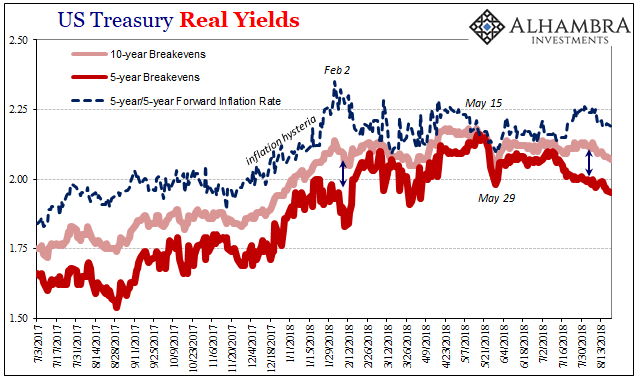

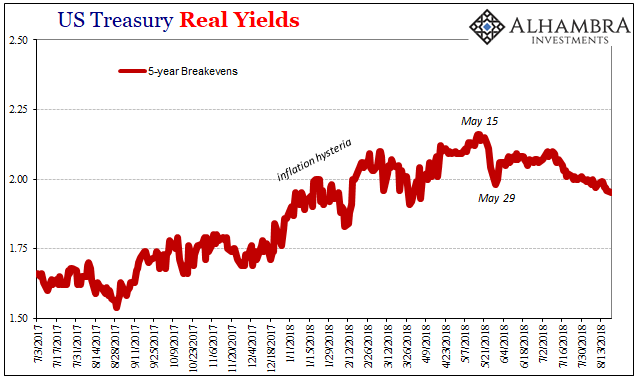

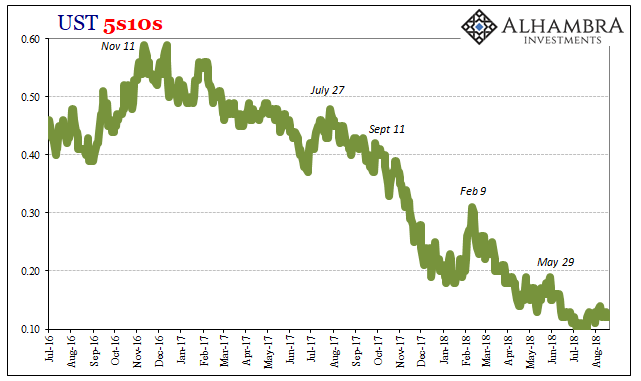

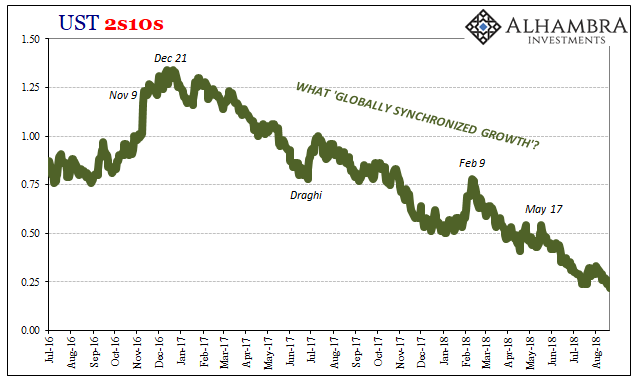

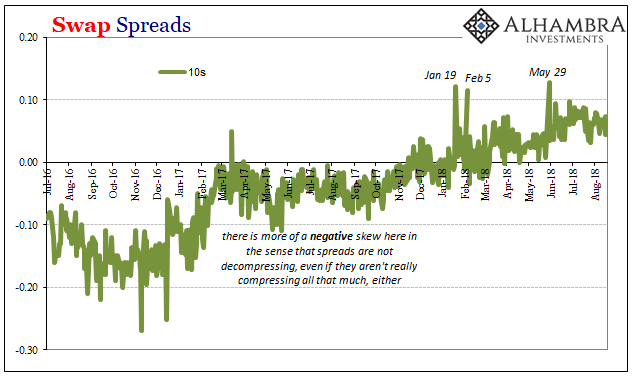

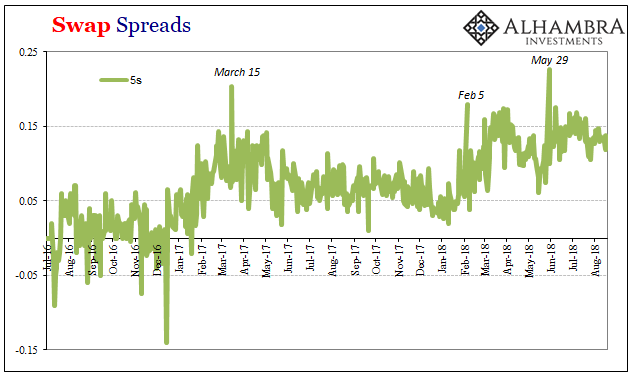

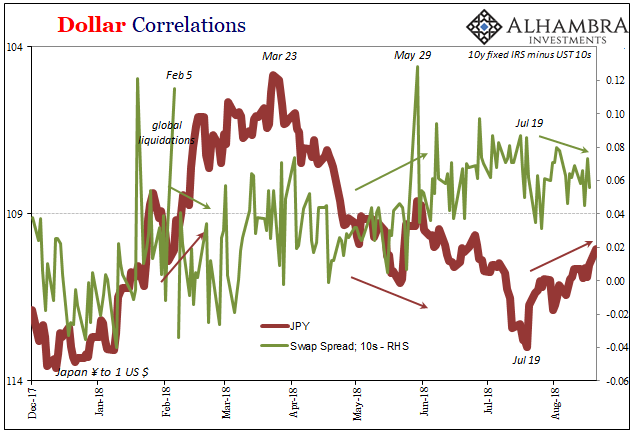

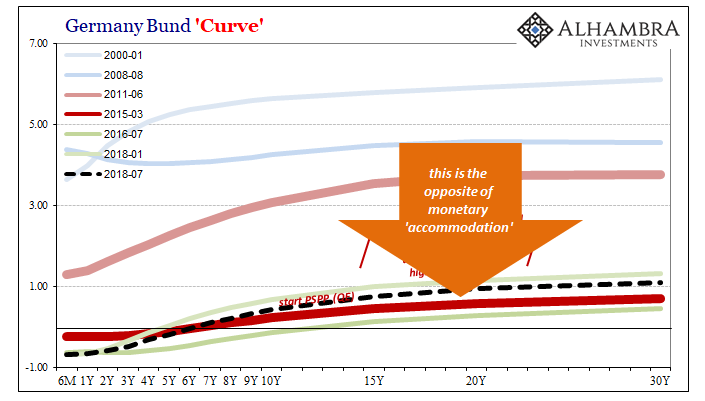

More and more it appears that the period between May 29 and the middle or end of July was not really one of calm so much as re-assessment. The rethinking seems to have been about what that was on May 29 and what it might mean for beyond the short run. We see May 29 show up practically everywhere, not just in bunds yields.

One of the more prominent reversals has been inflation trading. Breakevens derived from the TIPS market display a crystal-clear inflection in those specific days between when the UST selloff reached its recent high (yield) and that collateral event two weeks later. In terms of the 5s breakevens, it’s about as prominent of a rolling over signal as you might ever see.

It’s now three months and counting, and therefore not as likely some usual market vacillation. In other words, money and bond markets (largely the same thing) are more and more pessimistic about the state of affairs starting with global eurodollar liquidity (not Korea, inflation, trade wars, Italy, or whatever other flavor of the month). The deflationary gold signal is in no way isolated; it’s being compounded all over the place just not all at once (nothing goes in a straight line).

I still don’t think we are quite at the stage of self-reinforcing illiquid behavior, but it has to be getting close. The warnings are multiplying but they just aren’t as obvious and unambiguous yet in other places beyond TIPS or JPY.

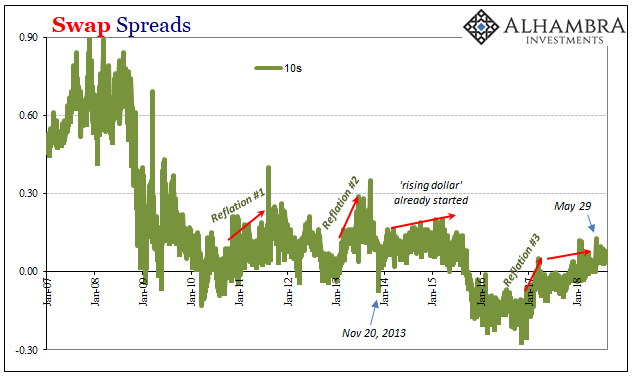

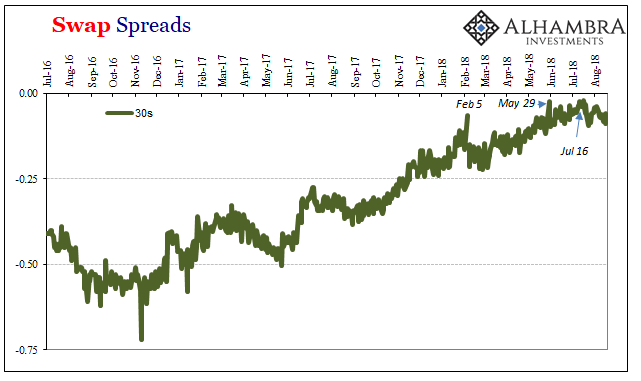

Swap spreads, for example, which are a lagging global balance sheet indicator exhibit largely the same things including May 29. And they have shifted in the months after the collateral difficulties, too, but not yet in a manner that would clearly indicate a wholesale change in conditions. Right now, swap spreads merely suggest or hint that something more serious like that could be underway.

When you put swap spreads together with something like JPY you end up wondering just how close to the edge monetary conditions might be. Again, it’s impossible to tell but with so many things moving this way it does possibly explain what’s different around August so far.

Back to July:

If WTI and JPY were to crack in the weeks and months ahead, that would really mean something. Not that we shouldn’t be concerned now; we don’t need to look at things in binary fashion. The possible or even likely end of Reflation #3 doesn’t necessarily mean the beginning of Eurodollar Event #4. There is some space in between them.

Still, the more of deflationary hints that might appear the less likely the self-reinforcing stuff remains at bay.

I didn’t add WTI here, but we could if we wanted to (particularly the shape of the futures curve that is actually lagging the European gasoil futures curve already back in contango).

Briefly, August has been bad because pessimism is growing, downside potentials moving back into focus. I’ve fixated on May 29 because it seems to have been a very big deal in all these places – not that you would know it on the outside. This isn’t surprising, a global collateral call will get anyone’s attention who is paying attention (meaning not central bankers or Economists).

Money and bond markets looked at it and increasingly it appears they don’t like what they saw/see.

Stay In Touch