According to the Conference Board, US consumers are sky high. The business association’s index measuring consumer confidence jumped to a level it hasn’t seen since the apex of the dot-com days. Though I’m not sure that’s really a positive reflection on the economy, the mainstream verdict is as usual quite different.

U.S. consumer confidence surged to near an 18-year high in August, as households remained upbeat on the labor market, pointing to strong consumer spending that should help to sustain the economy for the remainder of the year.

Nothing but good things as far as the consumer is “feeling.” So, where is the spending? It’s just not there, though everything you hear makes it seem like it is.

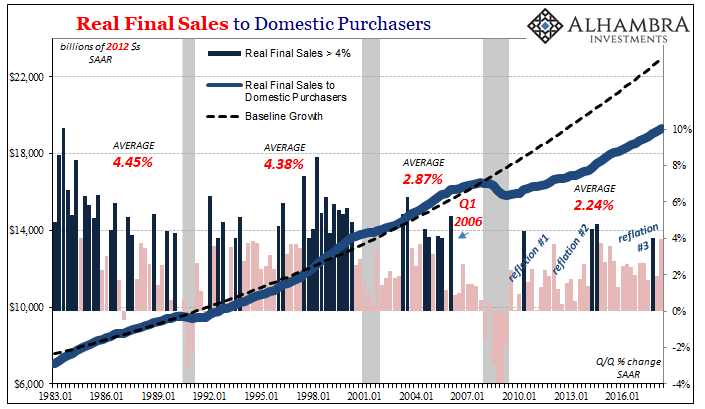

After all, GDP in Q2 2018 was just revised a tic higher to 4.2% (Q/Q SAAR). Within that number, Real Final Sales to Domestic Purchasers, the most exhaustive and comprehensive estimate for consumer and business spending on everything from goods to services no matter where they are produced, grew by just less than 4%. In fact, that makes two out of the last three quarters above or near a 4% annual growth rate. Booming!

But these rates only stand out because everything has been so awful for so long. The average gain since the end of the Great “Recession” has been a pitiful 2.24%. Compared to that, 4% does look awesome.

Before the housing bubble collapsed in the middle of 2006, however, consumer spending used to average better than quite a bit more than 4%. In this environment of surging consumer confidence, consumers manage to spend at rates that were once below average – and it looks like a splurge compared to recent imposed frugality.

It shows that the economic problems in 2018 are really two problems, both of which reach all the way back a decade and more. We no longer recognize a truly strong economy when we see one because we haven’t seen one is so many years. Consumers may be confident, but that’s clearly nothing more than stock market noise (thus, the dreaded comparison to the dot-com era).

They sure aren’t acting confident. A four percent quarter is fine, but actual economic growth would mean at least that much quarter after quarter after quarter the way it used to be. Not even the most technocratic friendly optimist is expecting this 4% stuff to last.

CNBC admits as much in its writeup of today’s GDP revisions:

But the robust growth in the second quarter is unlikely to be sustained given the one-off drivers such as a $1.5 trillion tax cut package, which provided a jolt to consumer spending after a lackluster first quarter, and a front-loading of soybean exports to China to beat retaliatory trade tariffs.

Think about what they are saying in the context of proper context. It took a $1.5 trillion tax cut package and all we got was one 4% quarter? That’s not robust by any stretch, and it sure isn’t the positive signal everyone seems to want to make it. It’s instead pure confirmation bias.

#understandtheconfusion

#understandtheconfusion

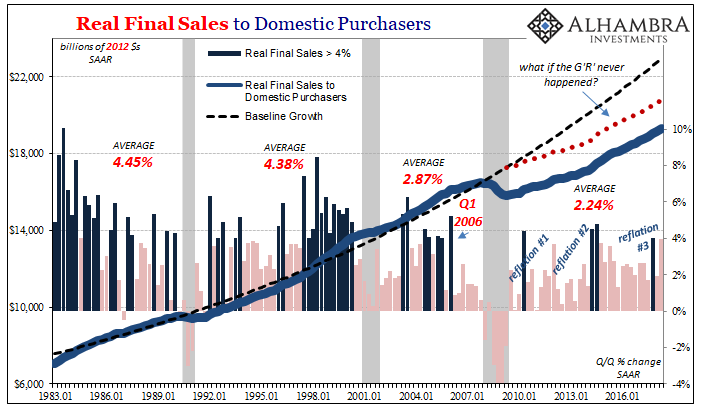

To demonstrate just how far off the current economic condition is from anything resembling a boom, we can zero out the Great “Recession” (red dotted line above) and consumer spending still lags so far behind as to still be of an entirely different paradigm. If the 2008-09 hole was magically erased and filled in, the lack of growth including 2017 and 2018 leaves us with massive unresolved problems anyway.

Of course, the two things are very much related. The lack of growth following 2008 as well as the collapse in that year and the first half of the one that followed were results of the same monetary breakdown. The economy has never recovered, and it isn’t recovering now. This would have to happen before any actual boom.

That means, despite the Conference Board’s measure of stock market exuberance, consumers remain in another world post-2008 collapse. Because it was such a major jolt, as well as the further monetary jolts received over the decade since, growth is no longer even possible on prior terms. They call it that because the numbers are positive and occasionally near average (while at the same time ignoring all the downturns, “transitory” whatnot).

Therefore, when speaking or writing about the booming economy in the mainstream, they can only be referring to the last ten years. There is no boom at least not by any reasonable historical standards. And even by the relative comparisons within the last decade, this year doesn’t even match up to 2014. To say only that the economy is booming compared to 2015 just isn’t the same thing; at all.

But consumer confidence is much higher now than four years ago, even though consumers aren’t spending as much (rowth). It’s almost as if consumer confidence is meaningless, just like share prices, in economic terms.

Four percent is better than 2%, to be sure, but we’ve seen the occasional 4% before. That’s never the problem. The only thing that matters is why there isn’t more of these quarters. And if it takes massive tax cuts to get there just once, no wonder everyone’s favorite economic measure is now suddenly the yield curve.

Stay In Touch