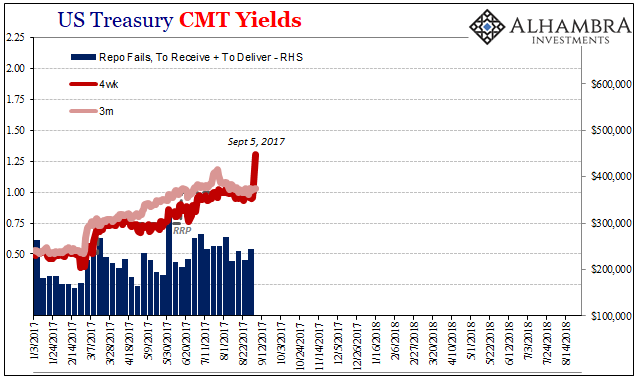

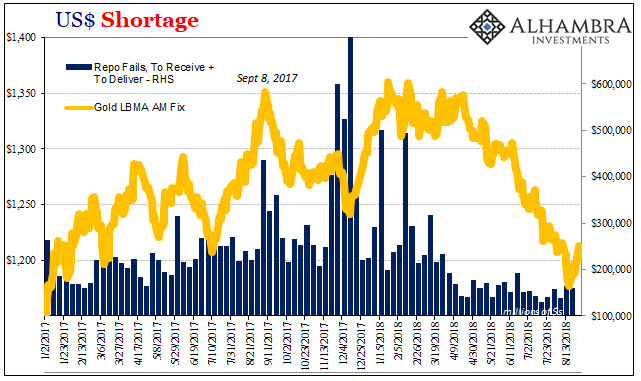

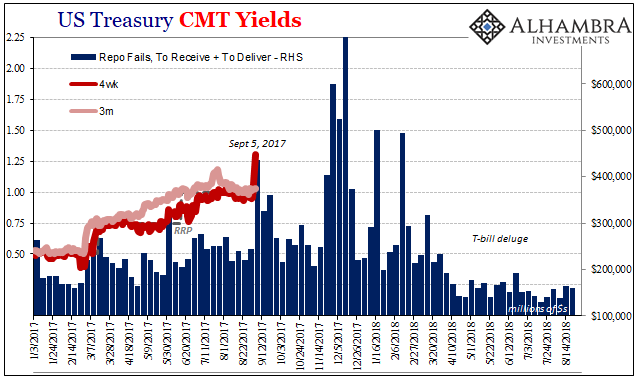

One year ago today, something broke. It wasn’t a big thing, practically a footnote seemingly not worth mainstream attention. Out of nowhere, the 4-week T-bill yield spiked. On Friday, September 1, 2017, the equivalent interest rate for the instrument was steady at 96 bps. That was already a problem because the Federal Reserve’s RRP was at the time set for 100 bps. Bill rates had been shallow all last year, suggesting that underneath conditions were already tight where it counted.

The day after 2017’s Labor Day, however, the 4-week bill absolutely plunged (price). When it was over, the equivalent yield on September 5 had surged to 130 bps. Bill rates don’t move much, so 34 bps in one day was eye popping.

No matter, “they” said. It was just debt ceiling drama. Apparently bill holders were nervous about Trump and the ongoing budget negotiations. At least that was the mainstream explanation. In my view, that wasn’t it. That couldn’t have been it. This was a liquidation of bills, and who might be in the wrong position to have had to do something like that?

I wrote a few days afterward:

Longtime readers of my columns and posts can probably guess what’s coming next. The violence in the 4-week bill was immediately dismissed as a one-off fear over a debt ceiling problem that didn’t ever seem to be much of risk or concern. It was the usual benign (in terms of repo mechanics) rationalization that is common in these times.

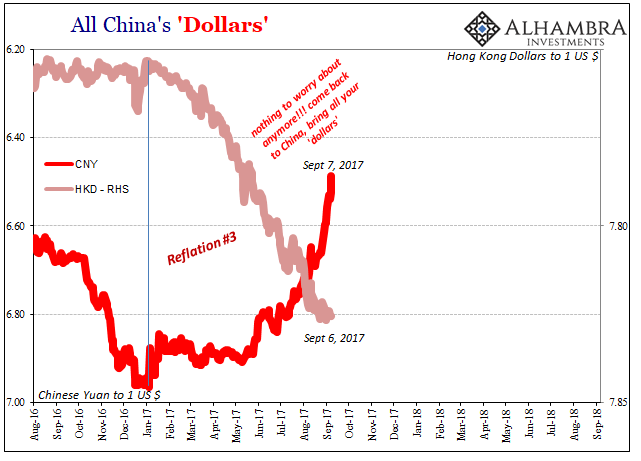

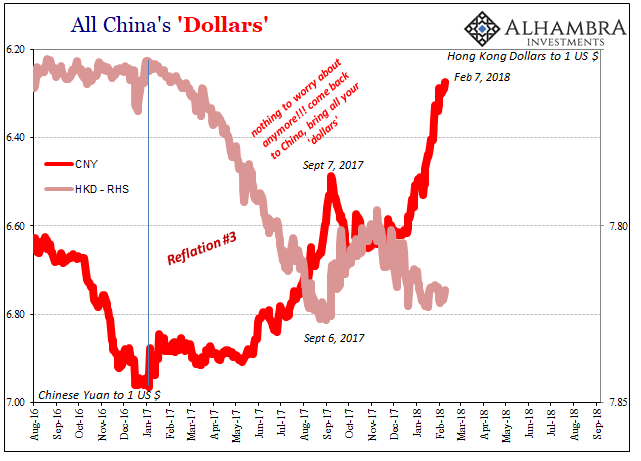

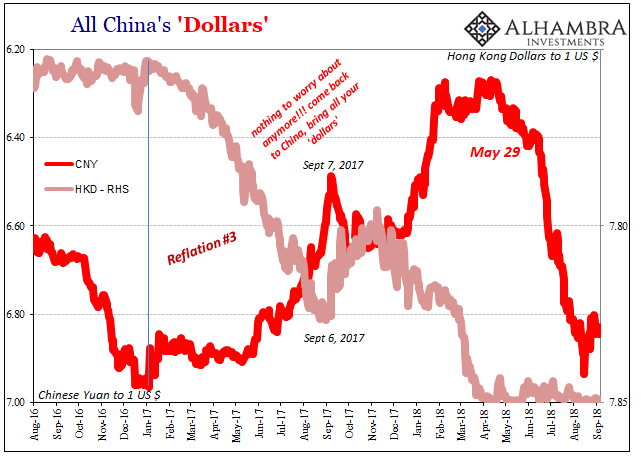

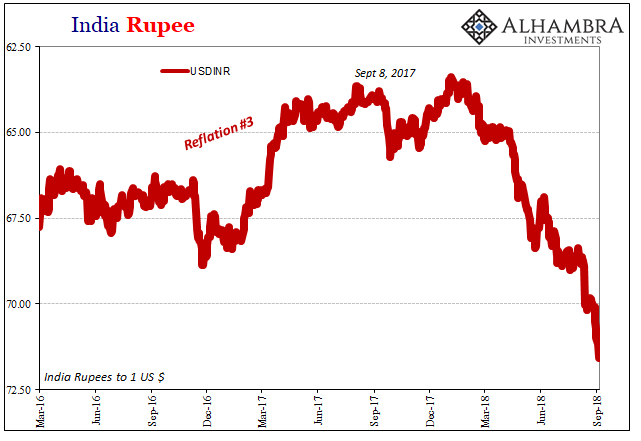

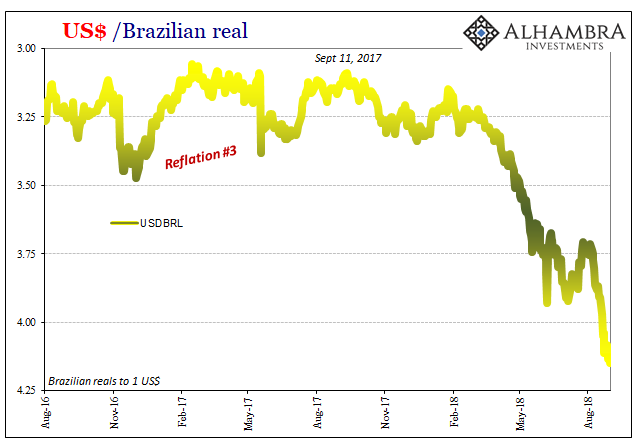

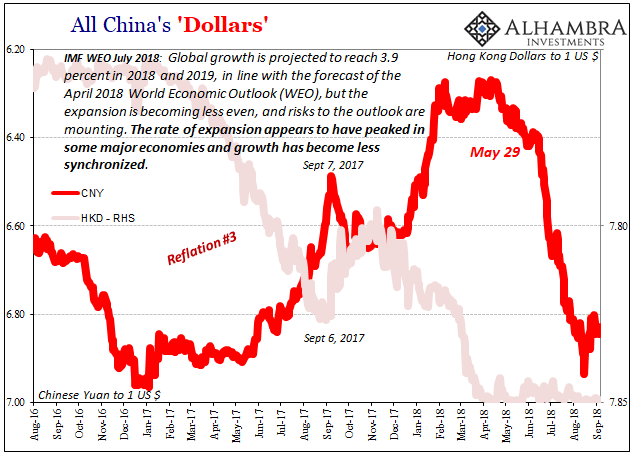

For an alternate (and only partial) explanation we might look instead west across the Pacific. The dominant feature of China money over the past few months has been rapid CNY appreciation.

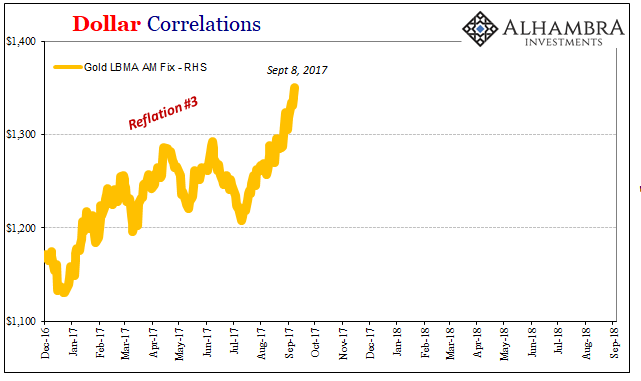

That had been true, too. Reflation #3 wasn’t all that great anywhere else, but it was in CNY. If there was anything the slightest bit attractive about it, the Chinese currency’s miraculous rise was the one part that had inspired at least some wonder whether there might have been something to this one. This was, I speculated, the whole point. Appearances.

If, however, you (being some unknown Chinese or China-related counterparties) are forced to liquidate a huge stock of UST bills all in one day? That’s not going to look good for convincing anyone of the soundness of Reflation #3 in CNY, and therefore everywhere else.

There were, again, already problems leading up to September 5. These disturbances are not actually out of blue. No one had bothered to provide an explanation for HKD’s mirrored movements to CNY. In fact, very few even noticed.

These linked currencies suggested a background attachment, in dollars. The event on September 5, 2017, was the first ripple that increasingly established the association. The more that happened, the less “miraculous” CNY’s remarkable ascent appeared to be.

That would suggest more and more the strongest piece of Reflation #3 was, in essence, an engineered lie. No wonder risk perceptions started to rise again following September 5. For the rest of 2017, the repo market would be an unstable mess fitting of this kind of grand re-assessment.

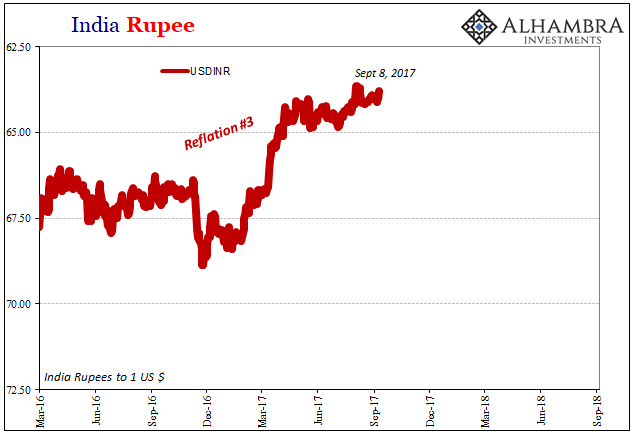

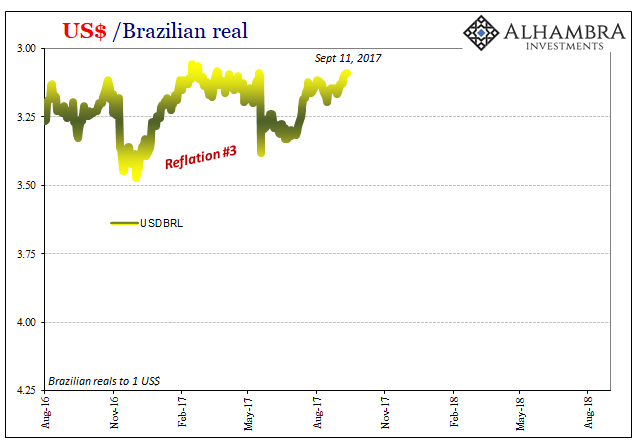

Once repo started to fall apart, inflationary reflation signals were immediately muddied. From gold to EM currencies, the first week in September 2017 has proved to be an inarguable turning point. It didn’t necessarily represent the exact moment when Reflation #3 flipped, but over and over we see how it was the point at which the process of reversal began.

I wrote in mid-September 2017:

It started with repo, and that part is confirmed. The real question is what this all means, up to and including whether it marks like fails in June 2014 the start of whatever the next phase of eurodollar decay might be. We obviously won’t know anything like that for some time (and we have to be very careful about bias, meaning that since I suspect it, it’s easy to believe and see what I think is already there), but the biggest clue will be in escalating warnings like this.

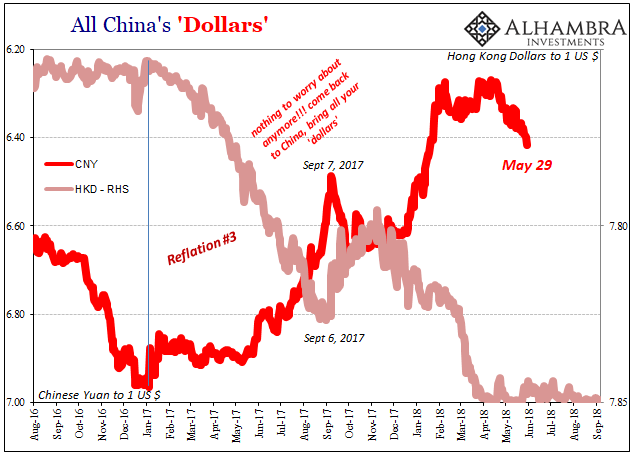

An entire year after that T-bill signal there can’t be much doubt left. Not about Reflation #3, that’s now long-gone. Instead, having actually witnessed a series of such warnings, from January/February liquidations to the possibly gigantic collateral call on May 29, we are at the stage facing toward downturn all over again.

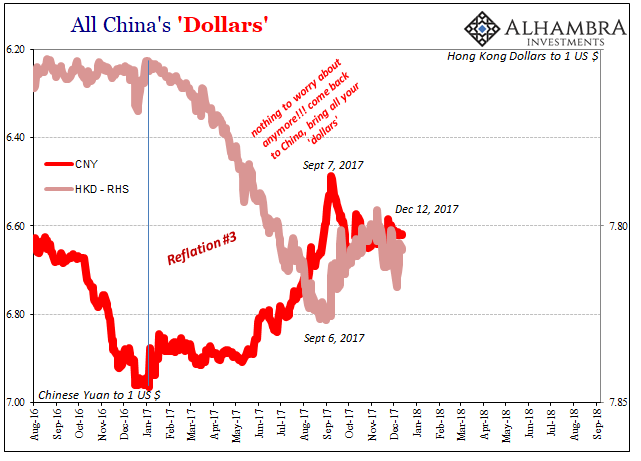

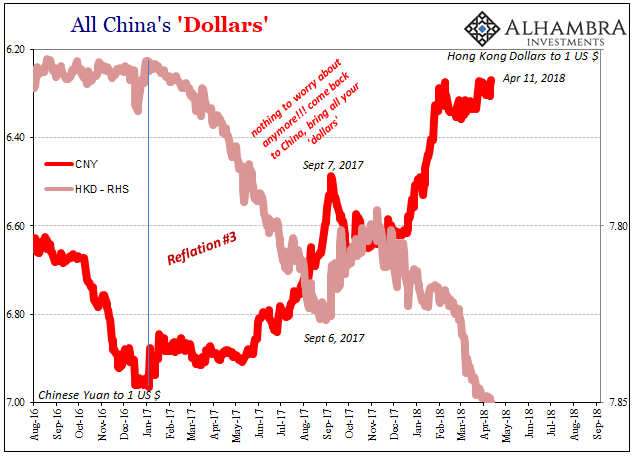

It didn’t happen all at once, these things never do; nothing ever goes in a straight line. Against every mainstream instinct, from inflation hysteria to globally synchronized growth, more and more the hidden pieces of eurodollar markets were the only things being synchronized. CNY would reach its cyclical high in early February just after those January liquidations, and then questions surrounding HKD emerged.

On April 11, HKD finally reached its lower boundary. In Hong Kong, the result was treated as a good thing (in public), the normalcy of so-called safety flows reversing. HKMA officials said nothing about the disorderly manner in which HKD had taken en route to 7.85; nor, obviously, have they attempted to explain what came next (starting with a massive collateral shift, in US$’s, that very week).

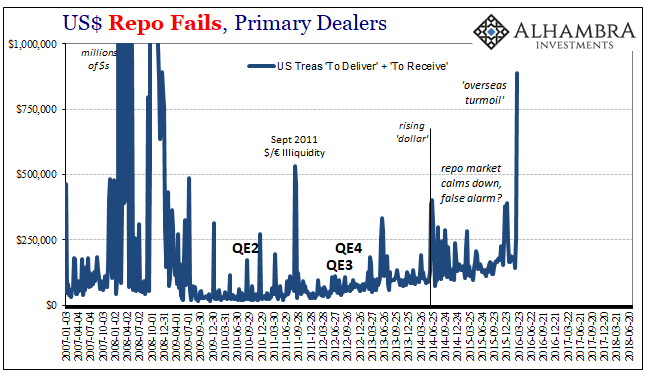

Everything that has followed in the weeks and months since April 11 has been those very escalating warnings. Again, the big one, so far, was May 29. The global eurodollar system has been increasingly disruptive ever since – despite the fact that US$ repo fails haven’t been a problem.

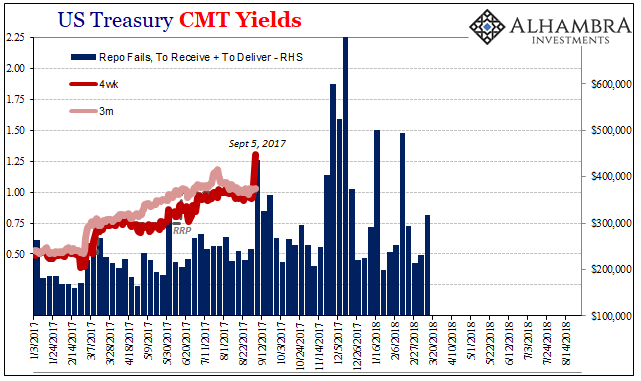

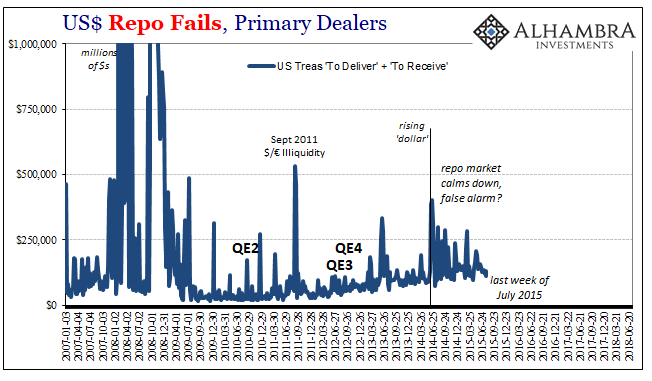

That’s the thing about shadow money. We’ve seen this before. In 2014, for example, repo fails did end up signaling the breakout of the “rising dollar” but then for almost a year there wasn’t much to them. Repo went back into the shadows while other parts went haywire.

It wasn’t until August 2015 the week before CNY broke that fails would start to rise at all. And it wasn’t until December 2015 that fails would again reach the same proportions as back at the beginning of the eurodollar cycle in June 2014.

In other words, “it” may start in a single place or in a single instrument like the 4-week bill in repo but if “it” doesn’t stay there then that’s when we get big trouble. This was ultimately what I meant by “escalating warnings.” It’s not that we should have expected the repo market to be a persistent, constant mess, where fails would only go up and up and up. It would be really easy if everything was one-to-one, but that’s not how it works.

Rather, like June 2014, there was something going on in early September 2017 that triggered a whole bunch of other problems. And since it was something that in the grand scheme of things wasn’t all that much, a little small disturbance in repo mechanics, what it really indicated was a fragile environment to begin with. There really wasn’t much to Reflation #3 after all.

These irregularities have since been spreading outward like an unstoppable runaway freight train, crashing the capacities of the most vulnerable pieces – and some that are not-so-vulnerable, like federal funds.

What exactly happened one year ago? I don’t know, and I don’t believe we ever will. What I do know is that it was a warning. Somewhere in between, Reflation #3 ended. Where we go from here is still up in the air, though now only somewhat. The baseline trajectory, unfortunately, is no longer the same one as globally synchronized growth. That idea had little chance to become reality.

In a single word of review: fragile.

Stay In Touch