For the first half of the Great “Recession”, China and the rest of the EM world seemed immune. It was American subprime mortgages that we were told was causing all the problems, and if European banks had somehow gotten themselves entangled in the rotten real estate mess so much the better for where growth was invulnerable.

This first instance of decoupling was just that strange, for these sorts of rationalizations about economic firewalls never stand the slightest scrutiny.

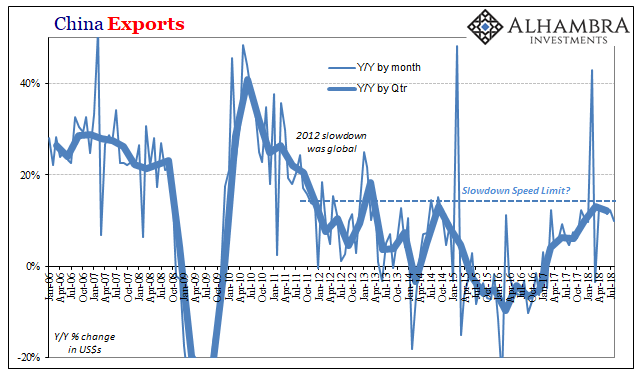

Chinese export growth had moderated in the second half of 2007. Exports were expanding by about 27% in Q2 2007, the last one before August 9. By Q4, outbound trade was growing at just 22%. As late as Q3 2008, Chinese exports were still around that lower level (23%).

Ignore the slowdown, they said. Michael Pettis in August 2008 was among many downplaying the difference:

…the woes of a small but powerful segment of the export industry – low-value-added processors in the south of China, who have been hit primarily by rising wages and a welcome shift in the southern economies towards higher-value-added goods and services – have created a false impression about dire conditions for China’s exporters.

The Council on Foreign Relation’s (globalists proselytizers) Brad Setser the same month:

The sharp fall in German export orders and anecdotal evidence that American manufacturers are seeing a fall in European demand do suggest a broader slump in trade is in the cards, and it is hard to believe that China won’t be touched. If Danske Bank is right, real exports already have slowed significantly, with about 10% of the nominal export growth now coming from higher prices. But 15% real export growth is still quite strong. The US would be thrilled with that kind of growth.

But when I look back, I really don’t see strong evidence that China’s export boom has slowed in any meaningful way.

In Q4 2008, the next one, Chinese exports were basically flat, up just 4.3%. In Q1 2009, minus 19.7%.

The Chinese perceptions of the global economy followed our own, if only to differing degrees. The first half of the panic, that which produced the initial global slowdown starting in the latter half of 2007, wasn’t all that significant in China. You could see it, the numbers all shifted. But by and large they didn’t move enough for people to think “decoupling” wouldn’t be likely.

Going by nothing else, 23% seemed pretty good and comforting.

They never factored the dollar, to appreciate why slowing from near 30% to near 20% might have instead confirmed some serious destructive influence for the whole worldwide economic system. In orthodox terms, the dollar is a simple price no more material than something like Amazon’s stock. It moves and is moved by buyers and sellers.

In the eurodollar system, however, the dollar tells us quite a lot about what really matters. If it starts to go up, that’s never a good sign. And if economic data begins to move the same way, that’s just confirmation.

There were already problems very apparent in global currency before Bear Stearns, and if Bear Stearns’ near failure didn’t get your attention, then the dollar’s stark reversal thereafter should have. People were optimistic about a lot of things in the summer of 2008. That’s the confusion we keep repeating over and over.

It wasn’t that Chinese export growth and overall growth was slowing down, it was why the whole world had fallen into condition where something like that could happen. It had nothing to do with subprime mortgages.

Exports during Reflation #3 may have peaked in Q1 2018 at just 13%. In Q2, they managed 12% growth. As of the month of August 2018, according to figures released on Saturday, less than 10% again.

This doesn’t suggest, for now, that China’s economy is staring off into another abyss like 2009 or 2015. It does, however, indicate that Chinese producers might be again thinking about those times and worrying how they might be deal with the negative pressures.

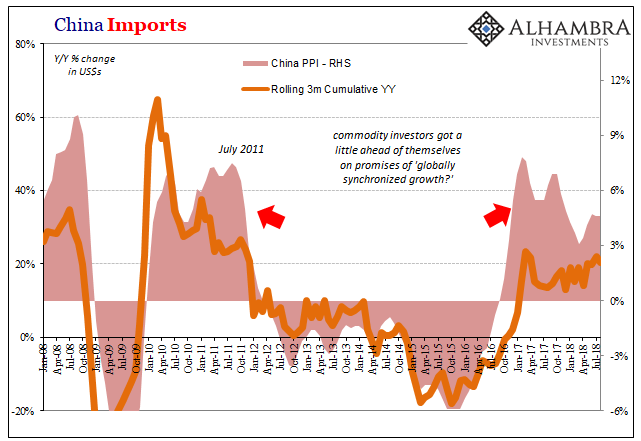

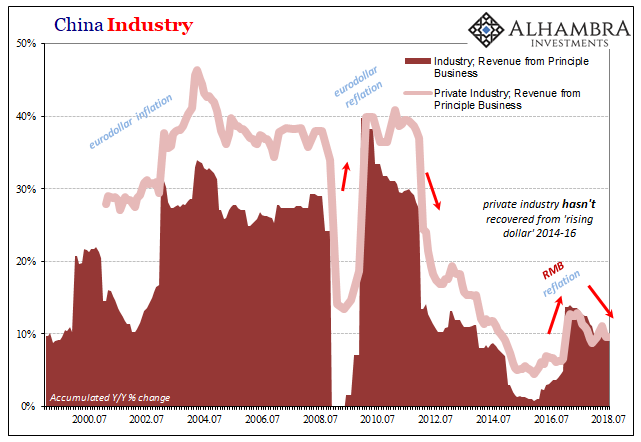

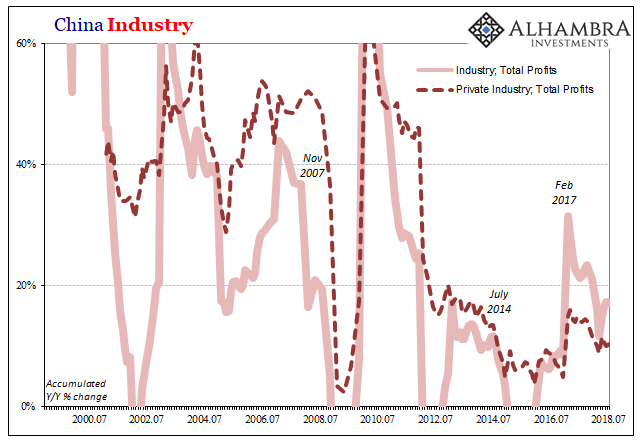

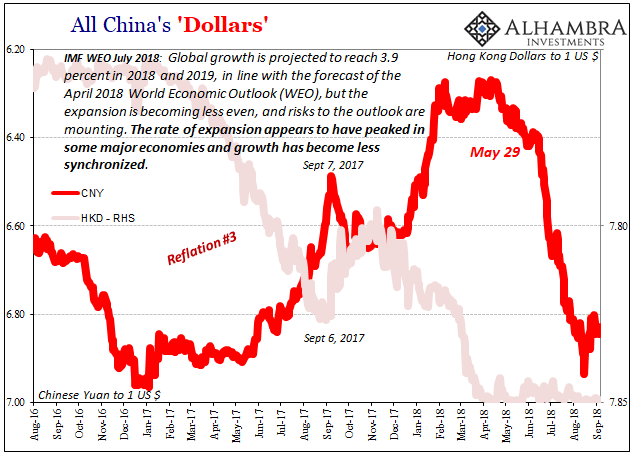

That’s a problem somewhat separate though related in things like China’s pricing structure. For one, commodity investors bought into Reflation #3 starting in 2016. They foresaw, via what was judged to be committed government “stimulus”, a Chinese economy therefore global economy that could be firing on all cylinders for the first time in years. If not 2017, then surely by the beginning of 2018.

Commodity prices were bid anticipating the global opportunity that awaited. Unfortunately for China’s producers, all that did was inhibit profit growth especially in manufacturing. Input prices went up by a lot more than the economy ever did. We keep hearing about particularly European and US economic booms, yet the Chinese have to be wondering where these are in the real world.

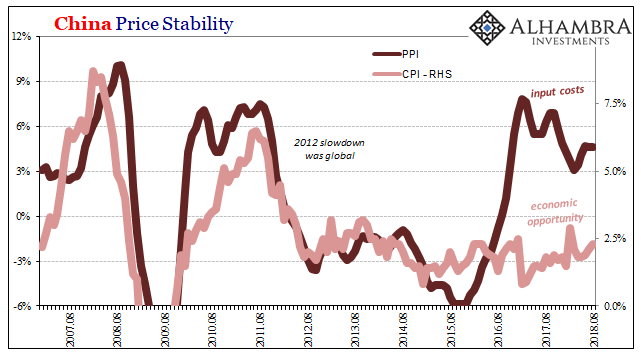

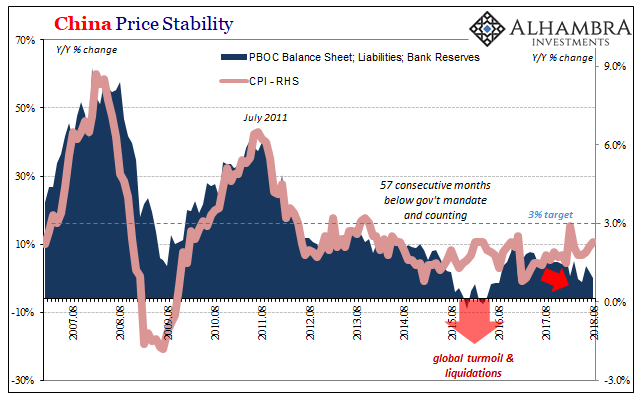

China’s National Bureau of Statistics reported also this weekend that its Producer Price Index (PPI) decelerated to 4.1% year-over-year growth in August. That was still materially greater than the Consumer Price Index, which rose only 2.3% (even as swine flu grips the Chinese porcine stock the CPI falls far short of the 3% target for the 57th straight month).

Investors were betting on an economy that just won’t materialize. And if China’s economy isn’t feeling globally synchronized growth, then the chances the thing was ever real is almost nil.

The difference, as always, is dollar. In the case of China’s CPI, money growth is inhibiting. The PBOC can’t manage a higher rate of bank reserve growth because they aren’t receiving any “dollar” inflows like they once did. The central bank tried in 2016 to “print” RMB to offset the eurodollar-based deficiency, but gave up after seeing limited results – including where commodity “speculators” got way ahead of themselves.

The dollar’s drag on China was also an anchor for the whole global economy. Reflation #3 was never all that strong even at its best point. The currency turnaround for CNY was misleading in that fashion (as, I’m sure, it was meant to be; Hong Kong). That only made the situation more tenuous given this difference between actual economic opportunity and the speculative costs of buying into the best-case scenario prematurely.

The results:

In economic terms, there was so much less to Reflation #3. And now, more and more, it looks like it’s gone, too. None of the economic indicators related to opportunity are suggesting anything like global growth, so in macro terms Reflation #3 may have done more harm than good (there’s always a price to be paid for mismatched expectations).

China wasn’t in trouble in 2008 because exports had come down from 28% to 22%. Likewise, the Chinese and therefore global economy isn’t in trouble because China can’t manage more than 13% growth in its best recent quarter. It’s why these things happen. The dollar goes up, and nothing good follows.

Stay In Touch