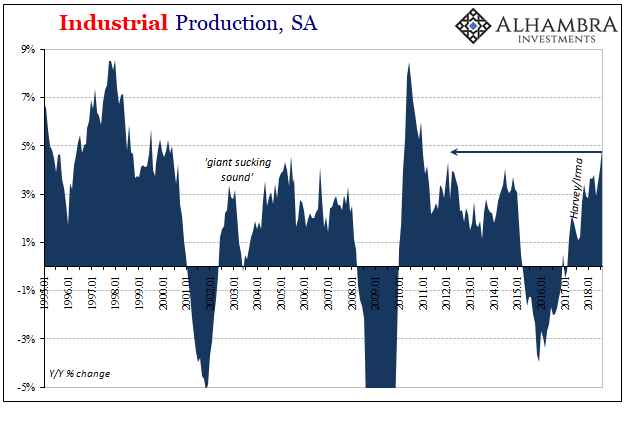

Industrial Production in the United States increased by 4.9% year-over-year in August 2018. That’s the best for American industry in 92 months going all the way back to December 2010. Hurray for the boom.

As with retail sales, August was in position for the best possible monthly comparison. Unlike retail sales, IP has another month of favorable base effects given that Harvey and Irma had shutdown a lot of heavy capacity also last September in addition to August.

More than the mathematical quirks of how statistics conform to a calendar, there are indications things are slowing down. It’s nothing like Europe or several EM economies, those that are already contracting. Instead, the growth rate over the last few months as compared to those prior is materially lower but still positive.

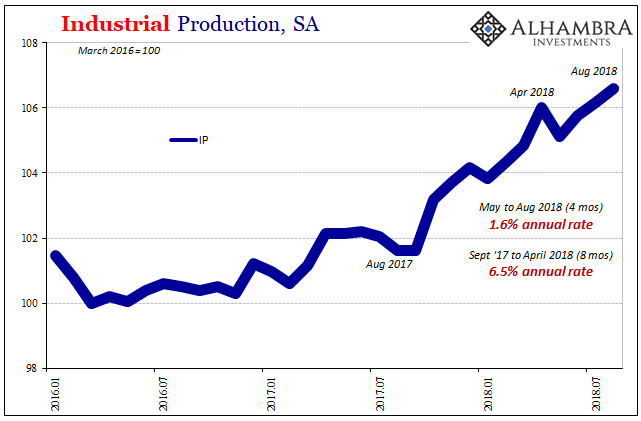

Accounting for this difference isn’t difficult. Between September and December 2017, the aftermath of Harvey and Irma contributed much to the increase, as did the pre-trade war period in 2018 up to around April. From August 2017 forward to April 2018 (8 months), US IP advanced at a 6.5% annual rate.

That would have been a 20th century kind of increase had it continued. Unfortunately, since April, IP is up at a very 21st century/post-crisis slowdown kind of rate. At less than 2% over the last four months it’s more consistent with what we’ve been seeing elsewhere around the world in the global goods trade.

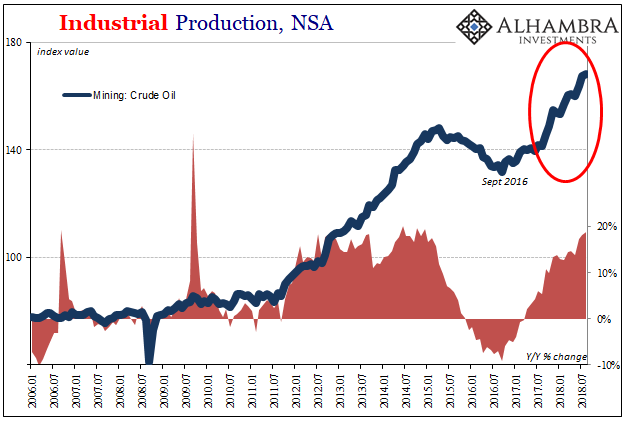

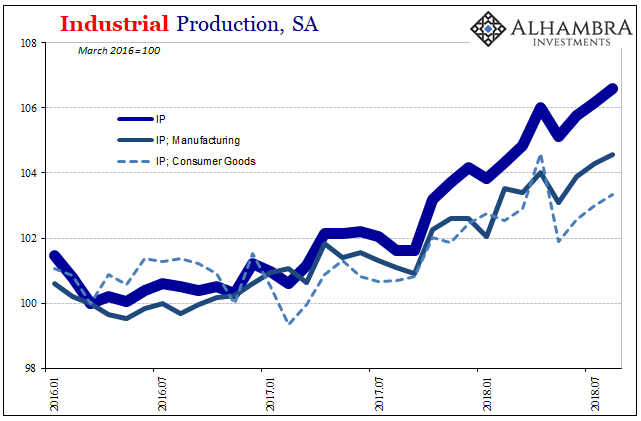

That’s really the big difference, too. US IP is being heavily influenced to the high side by crude oil production. In manufacturing, especially production of consumer goods, the US “boom” isn’t really one. The manufacturing index is up 5.0% from the low, but that’s across more than two years not one (2.2% annual rate).

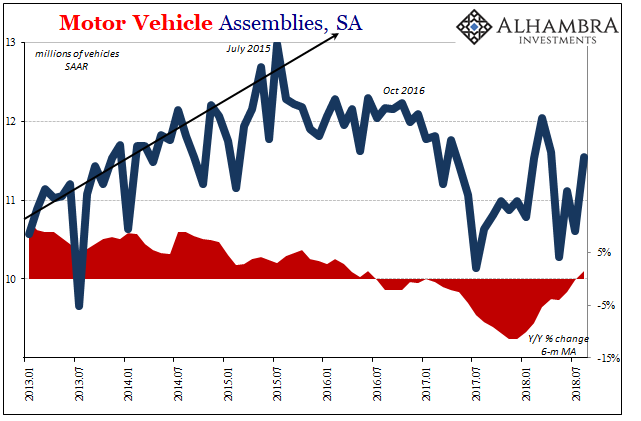

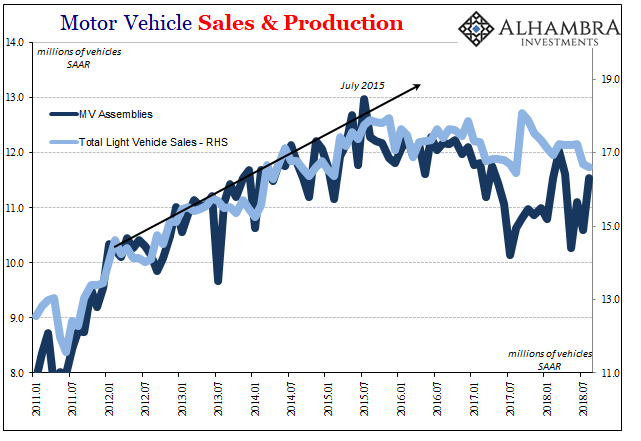

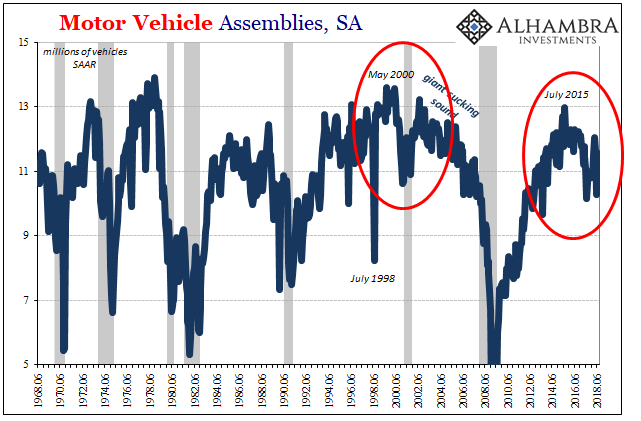

It continues to be the auto sector that is holding back American industry. Motor Vehicle Assemblies (MVA) came in at a seasonally-adjusted annual rate of 11.54 million in August. While up from 10.6 million in July, the prior estimate was revised way down from 11.18 million. There continues to be serious uncertainty in the auto business, as suggested by the uncertainty in the estimates for the auto business.

Auto sales continue to be sluggish, a break in the prior trend that is stretching into its fourth year. It’s a pretty conclusive signal. There is nothing to indicate that auto sales are about to pickup as they would in a truly booming economy (meaning the whole outside of just energy). Rather, the latest sales estimates are pointing down not up. Vehicle sales in August were just about as bad as the lowest point in 2017 before Harvey destroyed thousands upon thousands of cars and trucks.

The variable in between is inventory. Despite the recession-like slowdown in auto production starting in late 2016, inventories remain elevated such that two years later supply hasn’t yet equalized to what appears to be slightly if steadily declining demand.

It’s yet another economic sector and variable where oil prices are muddying the picture. The mainstream narrative of globally synchronized growth is like WTI, where increases are believed to be the “real” underlying trend despite all these major inconsistencies.

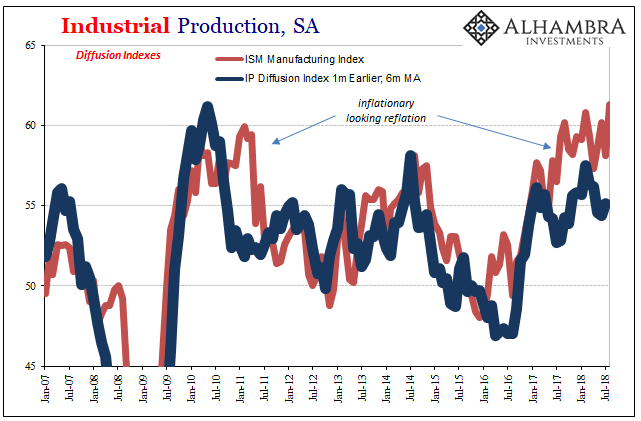

Even the outlook for industry and manufacturing is divergent. The ISM Manufacturing PMI, for example, keeps rising to new multi-year highs. The diffusion index contained within the Industrial Production data, on the contrary, has not rebounded quite so far and is signaling this current slowdown. The difference is how the ISM captures changes in prices, one of the big movers this year in that PMI, whereas these diffusion estimates do not.

And so, like headline inflation in either the CPI or PCE Deflator, we are back to questioning whether the good parts (mining; crude oil) are sustainable in the face of continuing weakness almost everywhere else. Will the energy sector be able to pull up a struggling economy so that it actually booms at some point?

It didn’t in 2014, that’s for sure, and the US economy had a lot more going for it back then (including autos). The only positive so far in the second half of 2018 is that the dollar hasn’t been nearly as disruptive worldwide. But that’s hardly a positive economic attribute; the global monetary system isn’t as completely screwed up (yet) as it was four years ago.

Despite the gaudy headline rate, these are not the attributes of healthy economy. They are instead the signs of an artificial boom, at best. The trick isn’t getting to reflation, it is getting past reflation into true recovery. That could still happen, but already two-thirds of 2018 have been booked and the downside risks remain far more substantial than upside potential. And that’s before we get to the possible next downturn.

Stay In Touch