The Asians are selling their Treasuries again, which can only mean one thing. The mainstream media will offer all sorts of explanations as to why that might be and not a single one will be correct. China and Japan are offloading US$ assets primarily federal government debt for vastly different reasons. Their decisions spring from the same source, but Japan’s position in the global reserve system is nothing like China’s.

Here’s one explanation for Japan’s dumping of treasuries offered back in February that probably sounded good when it was written. Weak dollar:

Japanese investors may be America’s bond bears.

They are shifting toward selling U.S. Treasury bonds and other dollar-based debt after fears have picked up in recent weeks that the Trump administration’s budget and other policies add up to a weak dollar.

The repositioning of Japanese banks tells us a lot about this last year, for sure, but not in any way like what is described above. The dollar is no longer weak, but Japan is still selling.

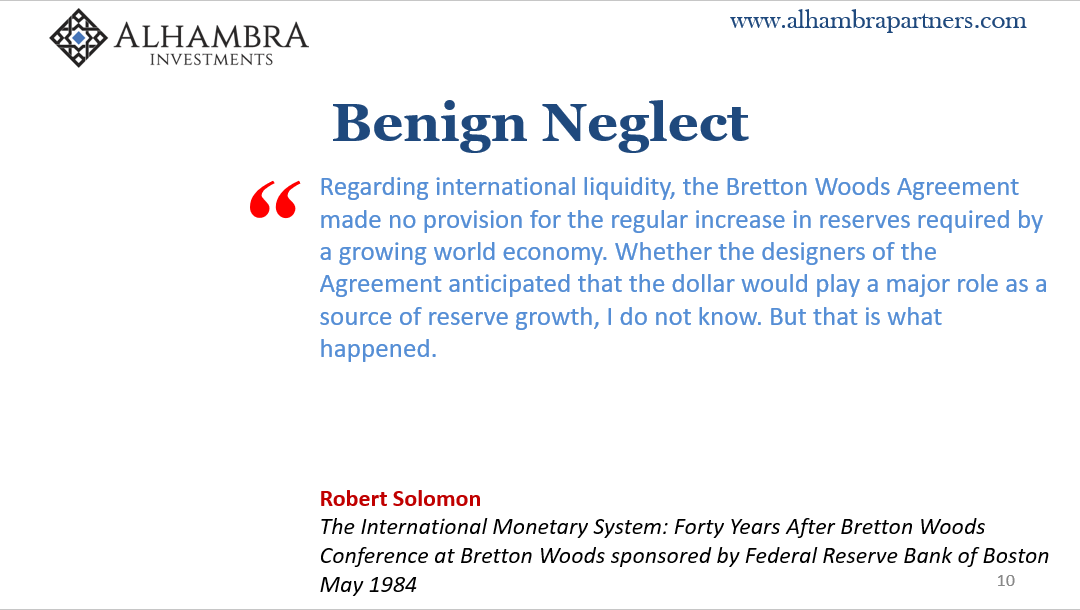

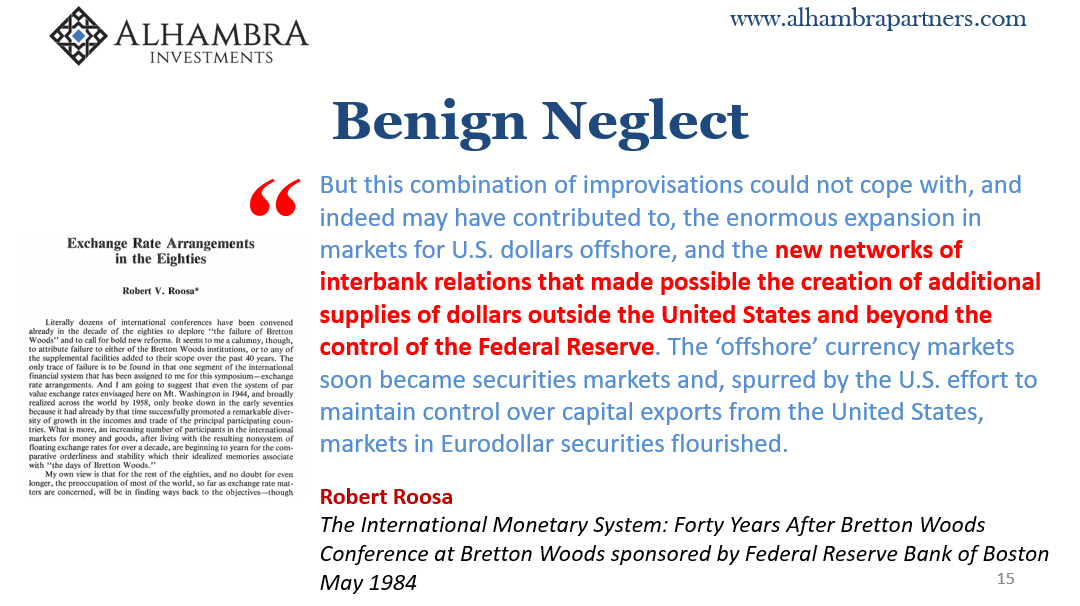

The problem stems from gross misunderstanding of the very idea of a global reserve currency, and therefore the lack of appreciation for the current one. I focused on just this aspect of intellectual darkness, what was once characterized as “benign neglect”, in my speech last week to the CFA Society of the Cayman Islands.

Their topic was globalization and my contribution to it was to try to help understand first what a global reserve currency actually is so as to further appreciate its role in how the world came to be this way. As I said last week:

We so often hear about a global reserve currency, almost always in considering which one might qualify rather than what it specifically means to qualify. What is the current global reserve currency? What is a global reserve currency?

Anyone attempting to answer the first question will inevitably be wrong. The reason is found in the little appreciation for the second. What is a global reserve currency?

Quite simply, the world needs dollars to intermediate global trade. The more global trade, the greater demand for dollars.

Historically, as Robert Triffin once pointed out, this was a bad match. The domestic supply of dollars could never fill the role required of it under this international arrangement. Bretton Woods had in its design an inherent flaw.

Conventional wisdom says that the international system finally broke free when President Nixon closed the gold window in August of 1971, thereby severing the link between dollars and gold. The end of Bretton Woods had meant no country could claim gold reserves from America for the surplus of dollars offered to them.

Nope. That’s not what really happened.

There was, in those early days, a multiplier effect. Once any bank around the world had obtained dollar liabilities for any reason, they could then multiply those offshore such that the global supply of eurodollars would increase immensely while at the same time the domestic money supply did not change.

Recalling Triffin’s Paradox, the eurodollar had solved it long before anyone in official capacity realized that fact.

The world needs dollars for globalization and trade, and the eurodollar system of closely connected banks (balance sheet capacity) supplies them.

But what happens when it doesn’t?

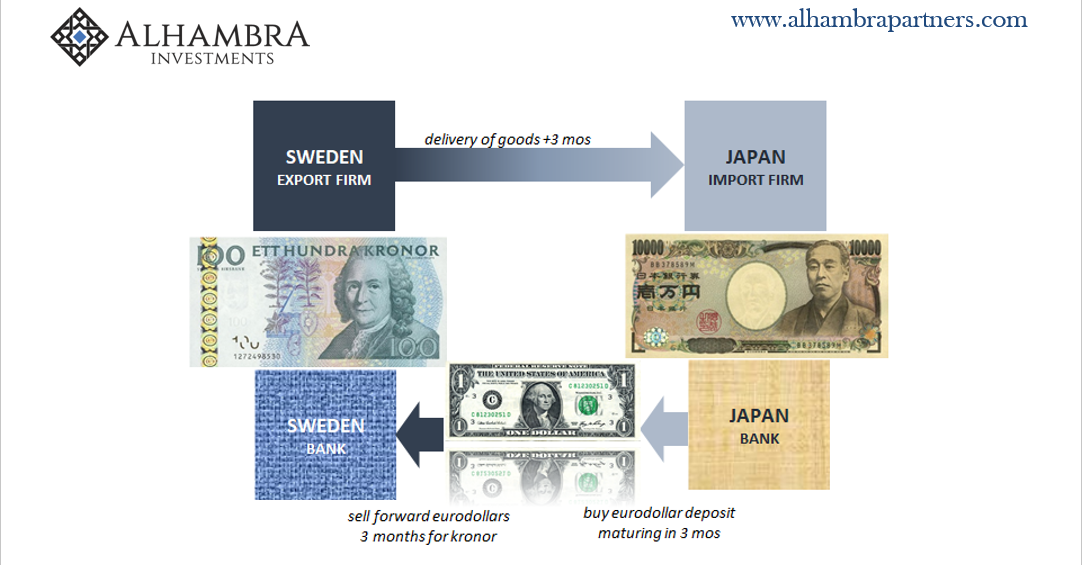

Obviously, global trade suffers without the ability to intermediate monetarily between different systems. In the example shown further above, the Japanese importer would have to find kronor to send to Sweden should it be unable to reasonably obtain dollars from the eurodollar market (either that or Swedish banks would have to be able to process yen the Swedish producer might receive from Japan).

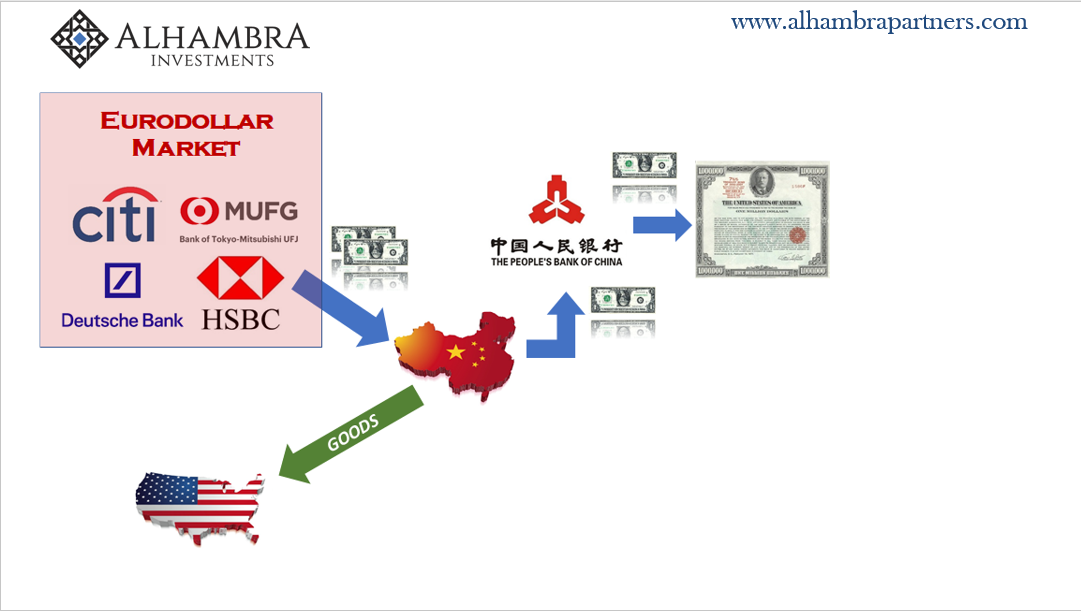

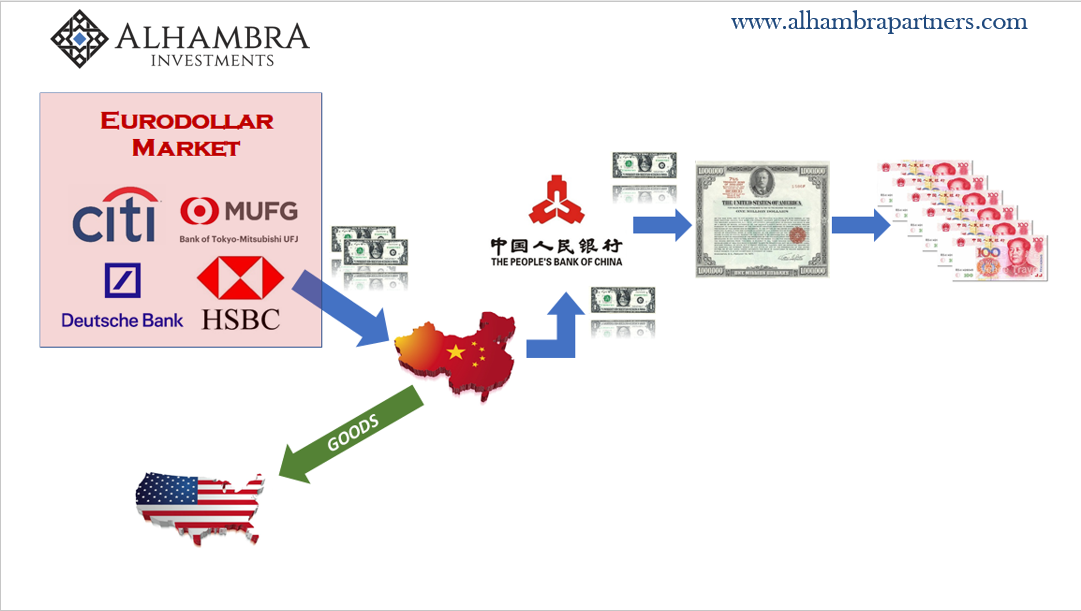

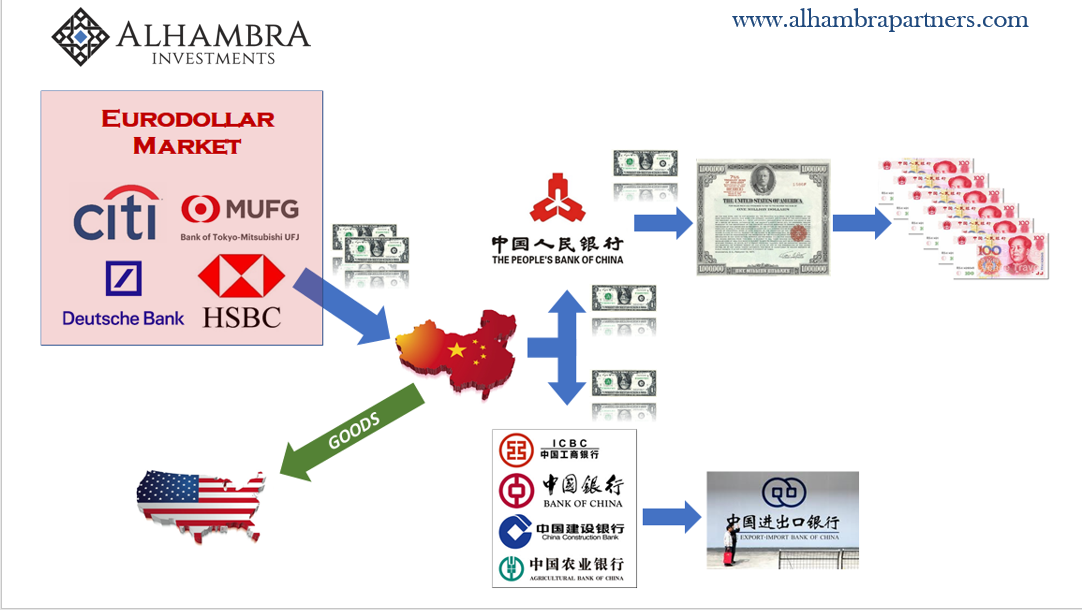

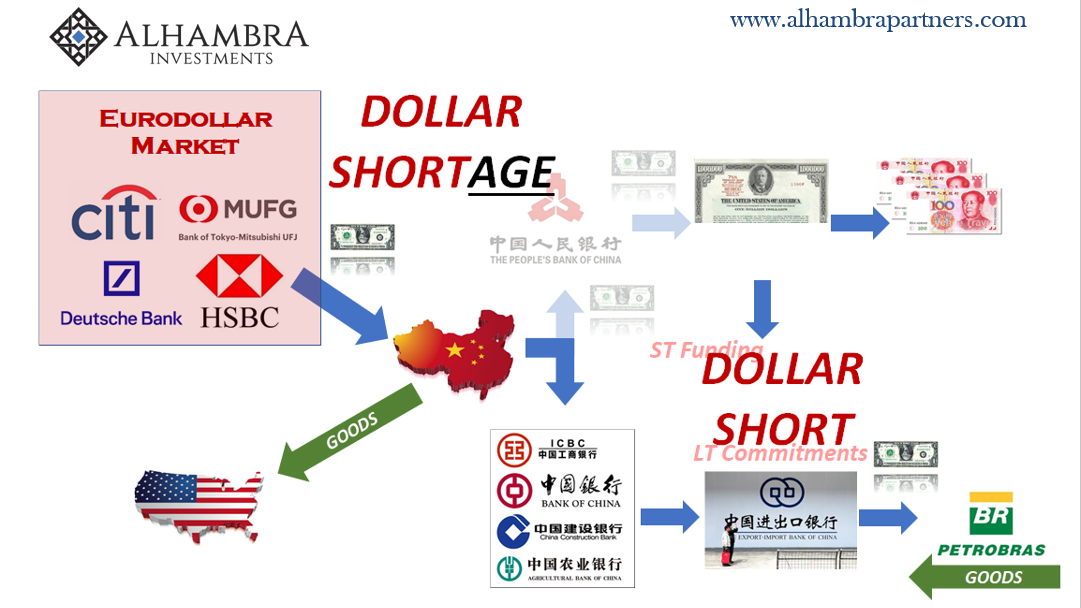

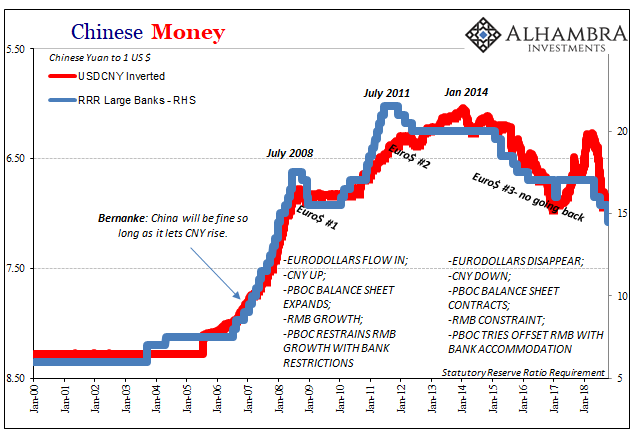

But it’s more complicated than all that. Much more. There are as many local monetary consequences as global, including how the import firm in Japan might instead be itself a bank intending to obtain dollars for further redistribution. China is the best example of this, the direct link between internal China money (RMB), the eurodollar system flowing through Tokyo, and ultimately US Treasury assets.

The following are excerpts (not complete) from my presentation in the Cayman’s:

Dollars enter China for both the purposes of merchandise trade as well as foreign investment, the so-called “hot money” of financial lore. The People’s Bank of China, the country’s central bank, ends up with a significant quantity of them. This was the consequence first of pegging the currency exchange of CNY with the dollar.

It takes these invading dollars and turns them into earning assets. We all know and hear about how China owns so much of the US national debt, here is where they obtain US securities. And not just those of the United States, but other currencies and assets are involved, as well. By and large, however, the largest proportion is in US$ official assets including agency paper.

You’ve also no doubt heard about how the Chinese, if they so desired, agitated enough by trade wars and what not, could destroy the US by selling all those bonds in a fit of audacious rage. It’s entirely untrue.

The way the global monetary system has evolved under this eurodollar standard has meant the dollarization of local currencies, including renminbi in China. These US treasury and other foreign assets are the basis for domestic monetary regimes. To oversimplify, renminbi is “backed” by the eurodollar.

For Chinese firms to export manufactured goods as well as import raw materials and parts so as to manufacture those goods, all those trade transactions require Chinese banks to have within their reach the same eurodollar market as in our stylized prior example.

Most often, funding in eurodollars means doing so at the shortest terms – just like any regular bank operating anywhere else in the world conducting regular banking activities. To obtain the cheapest and most dynamic funding, banks borrow overnight or at very limited maturities. But in this case Chinese banks aren’t overnight of renminbi, they are overnight US$’s obtaining them in the form of offshore dollar liabilities from banks that, as Milton Friedman showed, often have no direct connection to the US at all…

And also like every other bank, they lend these dollar liabilities out structured in longer-term arrangements. This maturity transformation is common throughout the history of banking, meaning that the only wrinkle, to be understated, is that the denomination and location of the funding source is very different.

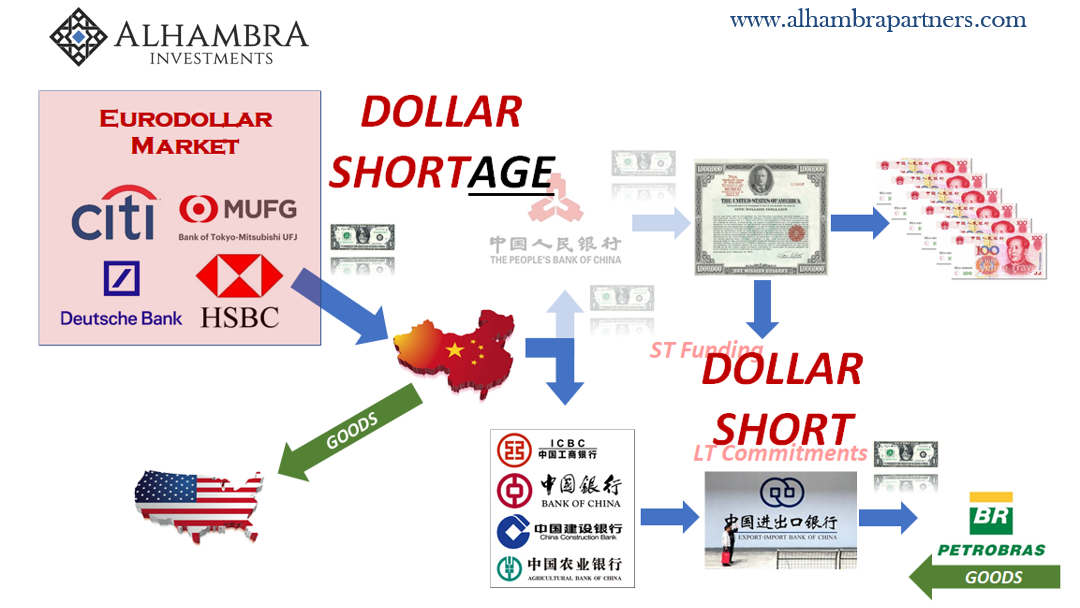

In functional terms, this means that China’s banks are “short” the dollar. It does not suggest, as the term “short” implies in other financial contexts, that they are betting the dollar will drop in exchange value. This is a synthetic short, one that caused a whole lot of global trouble right around ten years ago.

A synthetic short simply means that the regular maturity transformation banks carry out as a basic part of their business has been extended across a monetary or currency boundary such that they can’t easily match their book. If for some reason Chinese banks should run into funding difficulties here, because their liabilities are in dollars they have few options available to resolve them.

A dollar shortage is the eurodollar market’s inability to steadily service the local dollar short. The scenario of a systemic dollar shortage isn’t theory. The global financial crisis in 2008 wasn’t a Wall Street panic so much as it was Lombard Street; meaning that it wasn’t a dollar disruption, it was a eurodollar squeeze. Banks worldwide not just in China had been short, in these same funding mismatches, by unknown trillions. We don’t know by just how much because, thanks to Greenspan, Bernanke, and the modern practice of benign neglect, nobody knew enough to check…

In our China example, these banks are forced to restrict, obviously, new dollar loans they can extend for Chinese trade. If severe enough, it could force the calling in of existing loans as well as in extreme cases default on dollar funding.

This is one reason why so many countries chose to use foreign reserves as the basis for their monetary system. It was widely believed that stockpiling US$ reserve assets in particular would act as insurance against a dollar shortage. The Asian flu outbreak of 1997 and 1998 seemed to validate this approach, except that it was derived from the flawed Bernanke-type perspective that saw currency problems as the work of individual speculators rather than a systemic shortfall within the actual global reserve system.

The PBOC can choose to mobilize these reserves in the event of a dollar shortage. Domestic Chinese banks can then obtain their marginal dollar funding, or be subsidized in it, from the central bank bypassing to some extent a malfunctioning eurodollar market. The manner in which this happens isn’t always the straight selling of foreign reserves, in our example US Treasury securities, as the PBOC can and does use a variety of structures including swaps and repo’s to supply dollars when it deems it necessary.

This shortcut isn’t a cost-free tradeoff, however. Remember, the vast majority of the assets on the PBOC’s balance sheet are these foreign reserves, and therefore are connected directly to the internal RMB money supply.

Thus, we’ve related selling UST’s to the curtailing of currency growth inside China, both physical RMB notes as well as bank reserves, all originating from the dollar shortage; that is the inability of the eurodollar market to supply what’s minimally required. This is the very China stuff I’ve been yelling about all year. If you understand this arrangement, a few other things become very clear.

One:

It is for this reason that many central banks are reluctant to intervene even when presented with a large dollar shortage given their large standing dollar short. They must figure out how to maintain some balance between importing a potentially huge external monetary imbalance and making it an internal one at the same time their local banks unequivocally require those dollars for global trade purposes.

The economy suffers either way.

And two:

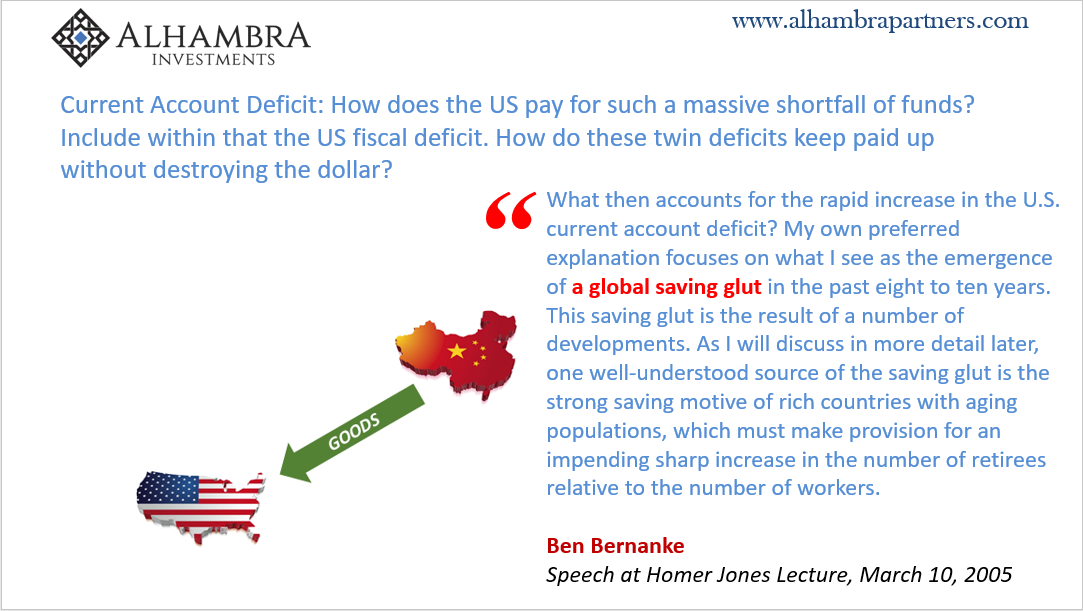

The fruits of globalization up to 2007 were carried forward by rapid monetary growth in this shadow global reserve currency. This made globalization popular, at the same time it made monetary ignorance even more so. So long as the eurodollar system was expanding, Alan Greenspan was a genius and countries like China experienced a modern economic miracle. Of course they would tolerate the US current account deficit as well as hold enormous quantities of US Treasury assets; those were features of the system, not bugs.

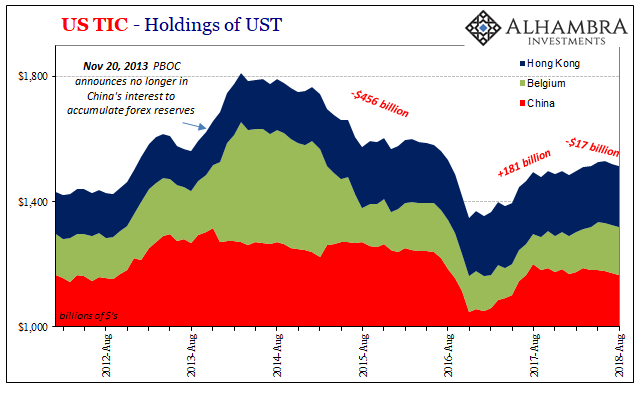

After letting CNY freefall all year, it does appear, and the latest TIC data does suggest, that Chinese officials have been supporting it again since July. In both July and now August there has been more “selling UST’s.”

That also corresponds to the renewed dollar warning coming out of China in the form of internal liquidity adjustments. The PBOC cut the RRR rate once in April before all this, then again in early July. It has since reduced the RRR one more time effective this past Monday. External dollar problems become internal RMB problems.

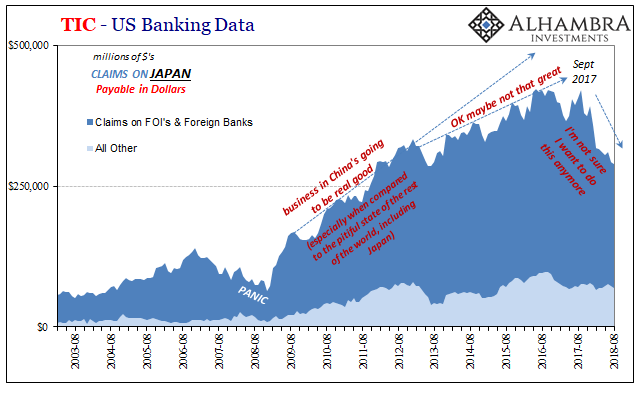

For Japan, the problem is the same though for those different reasons. Japanese banks are selling their holdings to get out of the dollar redistribution business. As the primary network connection between China’s dollar short and the rest of the eurodollar market, their exit is, in my view, a big part of why this year has turned out so very different from what it was supposed to.

In other words, Japanese banks are an important part of that eurodollar market, and their reluctance to add capacity to it, and in fact take a lot of capacity away from it since last September, explains conditions in a way convention simply cannot. The mainstream view is built upon the modern doctrine of “benign neglect” which is perhaps better characterized as determined monetary ignorance.

In closing, I told my audience the simple but for many hard-to-believe truth.

We have to peer behind the curtain and see what’s actually going on in exhaustively complex detail, no matter how uncomfortable that may make defenders of the status quo, in order to get the world economy and therefore the whole world back on track. Half a century of monetary honesty and plain minimal competency is required in place of ongoing benign neglect.

At this stage, there is no benign just neglect.

Stay In Touch