The Steering Committee for the International Monetary Fund (IMF) warned last week that tighter financial conditions globally are a risk. A bit late perhaps, but that’s how these things go. You can tell matters are serious when Economists are shaken out from their global growth slumber. The IMF wants everyone to know that this could be a danger to not just Emerging Market economies but also those in the developed world including the US, Europe, and even Japan.

The Bank of Japan’s leader, Haruhiko Kuroda, for one isn’t worried. The words “monetary” and “tightening” like monetary loosening are always associated with the central bank for these guys. Kuroda therefore immediately connects the IMF warning with the hawk Jay Powell.

It’s good that the United States is normalising monetary policy, because the economy is growing and inflation is already near (the Fed’s) target.

Kuroda’s right that rate hikes should be a welcome end to an otherwise disastrous decade. But there’s one key assumption buried underneath forever unchallenged: Federal Reserve officials think the economy is growing and inflation is already near target, and that’s why they are raising rates. What if they are wrong not just on the economy but also this global tightening so upsetting everyone?

Few contemplate the possibility. Convention remains fixed in this regard; central bankers are the best and brightest, therefore if they say so then who is anyone to argue?

They get away with this via mathematics. If you try to debate the point you end up discussing complex statistical theories instead. People are afraid of the math, politicians most of all, and Economists know it.

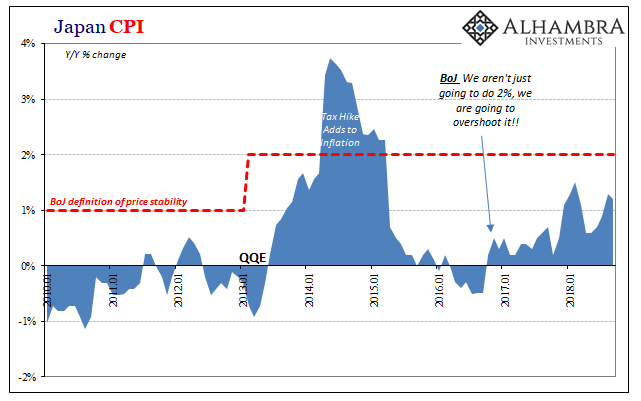

Nowhere is this more evident than in Japan. In January 2013, the central bank with Kuroda leading the charge announced that monetary policy would no longer be satisfied with 1% CPI inflation as a goal, it would actively target 2% CPI inflation. Three months later, QQE was launched with all this in mind based on tens of thousands of statistic simulations that said:

The Bank will achieve the price stability target of 2 percent in terms of the year-on-year rate of change in the consumer price index (CPI) at the earliest possible time, with a time horizon of about two years.

Two years would have been April 2015. But before getting that far, at the end of October 2014, QQE was somehow expanded. The calculations from early 2013 must’ve been off?

The Bank will continue with the QQE, aiming to achieve the price stability target of 2 percent, as long as it is necessary for maintaining that target in a stable manner. It will examine both upside and downside risks to economic activity and prices, and make adjustments as appropriate

We are meant to believe and then just accept that the equations didn’t properly anticipate “risks” which sort of makes simulations excluding them worthless. Now they’ve got them, so off they go.

Not content with several additional years of failure, the Bank of Japan kept at it. Nearly two years after expanding QQE Kuroda’s gang doubled down again in September 2016.

The Bank has introduced an inflation-overshooting commitment, under which it continues expanding the monetary base until the year-on-year rate of increase in the observed CPI (all items less fresh food) exceeds 2 percent and stays above the target in a stable manner. Through this commitment, the Bank aims to enhance the credibility of achieving the price stability target of 2 percent among the public.

Not only were they going to reach 2%, they were going to let inflation go and overshoot the target for some time. The reason? Don’t laugh, “to enhance the credibility” with the public.

Economists in Japan have always maintained the economy suffers from a deflationary mindset among the Japanese people. That’s not it at all, regular folks have come to realize what the rest of the world hasn’t quite yet. These central bankers have no idea what they are talking about and therefore have no idea what they are doing.

Think about all this. BoJ changes the definition to show Japan and the world it really, really means it this time – back in January 2013. That was more than five and a half years ago. Time may not be a parameter for DSGE evaluations, but it is in the real world.

Then expanding QQE to really, really demonstrate their resolve – just about four years from today. And finally to blow way past 2% inflation and get the whole thing undeniably overheated – twenty-five months later and the world is still waiting for them to come close.

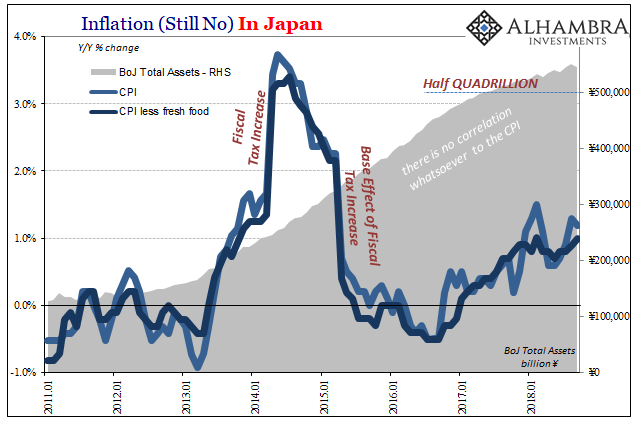

That’s not a deflationary mindset so much as a credibility gap, and a large one. That’s really been the only thing the Bank of Japan has managed to expand outside of its balance sheet. The more it does, and the longer it does it, there isn’t the least bit of doubt left.

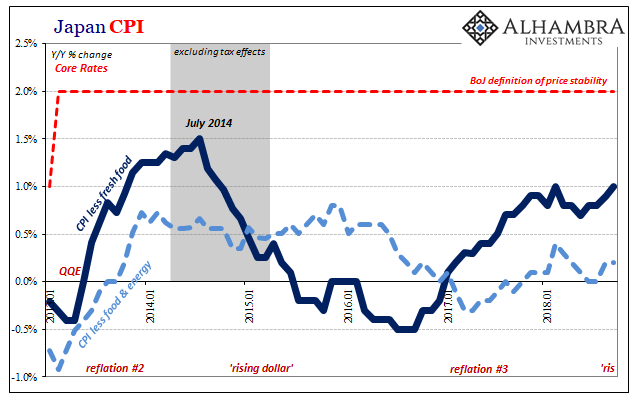

Outside of food and energy prices, there is nothing inflationary in and around Japan. Those other categories are being driven by factors that have nothing to do with monetary policy. The latest data for September 2018 merely confirms the waste of a mind-boggling amount of time on these supposedly best and brightest. The overall CPI fell back to 1.2% year-over-year while the index less fresh food rose by just 1.0%.

Stripping out both energy and food, inflation was all of 0.2% last month. More than half a decade of rhetorical rather than monetary exercises.

Following up with everything else this week, they don’t get the small things right. They miss the big things. And they can’t perform on the basic things, either, which inflation is for every central banker.

Sure, Powell thinks the US economy is doing well and getting back to normal. But, like his intellectual brother Kuroda, what does he know?

Stay In Touch