Paul Volcker caused a minor stir last week releasing a book he has been working on. The aging former Federal Reserve Chairman apparently has a lot to say about the current state of affairs. “We’re in a hell of a mess in every direction,” he told Andrew Ross Sorkin of The New York Times. No kidding; that about sums it up.

That’s the easy part. The hard part is figuring out why. I have little doubt Volcker doesn’t have any answers. How can he? His tenure at the Fed is the very reason we are in this mess.

It was during his time where monetary policy shed all relationship with money. Central bankers couldn’t define it anymore, the “missing money” seventies were only the beginning. After the twin recessions to begin the eighties, Volcker’s role in them seemingly definable, Economists began to believe they wouldn’t ever need to.

Monetary policy had shifted from, well, monetary policy to expectations policy. There is no money in the latter and central bankers used to be somewhat comfortable with its absence. The last decade shows they still believe in expectations management, it’s just that they aren’t nearly so comfortable.

Volcker in his 2018 book apparently criticizes the Fed’s current inflation target.

I puzzle at the rationale. A 2 percent target, or limit, was not in my textbook years ago. I know of no theoretical justification.

It shouldn’t confuse him in the slightest, his feigned outrage smacks of revisionism. There will eventually come a time when history takes a hard look at the last few decades and judges things very harshly; especially the pieces where central bankers were once thought to represent the apex of technocratic capabilities. Greenspan and Bernanke, it appears, aren’t the only former “best and brightest” concerned about their reputations holding up to actual rather than political scrutiny.

In monetary policy that is all about expectations a target is more than useful. If everyone believes the Fed can do what it says, because that’s how the early eighties have been put forward as an example, then anchoring expectations at 2% or whatever other arbitrary number necessarily follows. The central bank doesn’t actually have to do anything except, as Milton Friedman warned near the end of his life, keep up with public relations. Keep feeding the belief.

In terms of the Federal Reserve and the domestic inflation mandate, the 2% target for the PCE Deflator was implicit until the beginning of 2012. This distinction didn’t really matter because even in the nineties everyone knew that it was at least a central guidepost for Greenspan’s monetary policy.

In the whole of the 21st century to this point, we can easily divide its history into two chapters. The demarcation line is obviously the Great “Recession”, a worldwide monetary panic that still today isn’t recognized for how that could be. Something, something subprime.

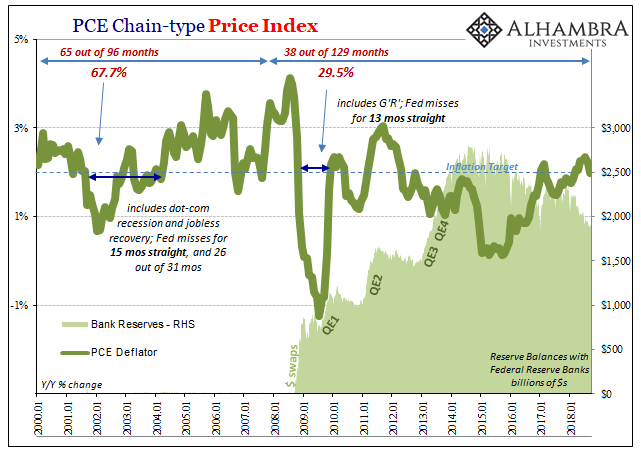

Prior to the 2007-09 contraction, the PCE Deflator grew at least by 2% in 65 out of the 96 months. That included a stretch at the last parts of the dot-com recession and into the recovery from it when inflation failed to meet 2% for 15 months straight. Despite that recession and the weak recovery from it, the target was met in two out of three months.

During this period the Fed did practically nothing though inflation was by far more likely to be above than below. There were almost no bank reserves in the system, instead the FOMC would vote for 25 bps (sometimes 50 bps) changes to a single money market rate.

Contrast that to the period after the break. The Fed has been very busy starting in August 2007. Except, the more the central bank does the less it succeeds in terms of its inflation mandate. It has met its now explicit 2% target in just 38 out of the 129 months, or less than one in three.

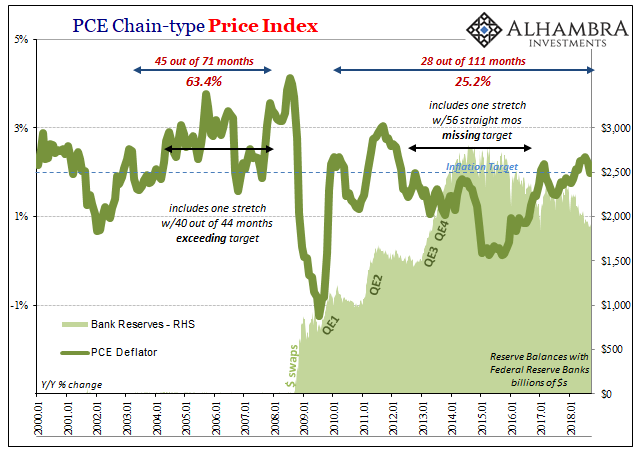

If we take out the recession months from both chapters, the track record is actually worse. Despite four QE’s and years of zero interest rates, Bernanke/Yellen/Powell have managed to hit their target in just one out of four. This includes, of course, a single stretch of 56 months where inflation continuously undershot often significantly. The entirety of QE’s three and four occurred within this period.

The more the Fed does, the less inflation results. This doesn’t mean that policymakers are the cause of the disparity. Rather, it simply shows that they see the same problems we do and react to them; only their solutions, balance sheet expansion and interest rates, don’t have any effect. They are irrelevant to inflation, therefore effective monetary conditions. Inflation is, over time, a monetary phenomenon.

The most charitable it can be said of monetary policy is that it tells us when the monetary system is malfunctioning. If the Fed feels compelled to act, then it’s probably not a good thing and it is definitely not a problem money-less monetary policy can solve.

This is the quite natural difference between monetary policy with money in it and expectations policy which the central bank has been following since the Volcker years. When confronted by a monetary break, a real one, central bankers had no idea what to do, sticking instead with expectations management and failing every step of the way.

Has anything changed?

Jay Powell’s Fed is committed like Yellen’s Fed to an inflationary scenario anyway. Predicated on the unemployment rate over anything else, because of a roaring economy tightening the labor market companies have to be competing for workers that are increasingly hard to find. As they, supposedly, pay more for them these businesses will have to pass those rising costs to consumers in the form of accelerating consumer price inflation.

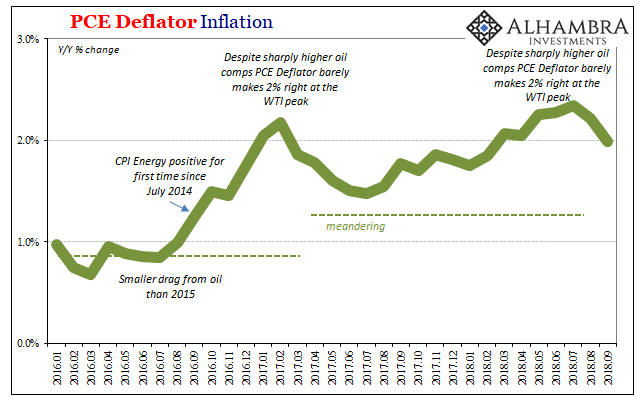

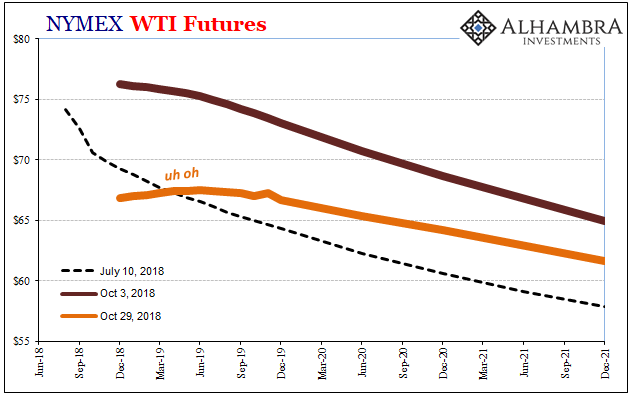

It just hasn’t materialized. We’ve been waiting now four years for it. Outside of oil prices rebounding from a conspicuous monetary-driven crash in between, inflation has tended still to be underneath rather than above its target. This includes the latest monthly figures for September 2018. Despite still heavy support from oil and energy prices year-over-year last month, the PCE Deflator was actually just a tick less than 2% (1.992863%).

It doesn’t really matter the exact figure and its exact position relative to monetary policy’s stated objective. What does is the direction; broad-based consumer price gains are supposed to be accelerating driven by the factors included in a sub-4% unemployment rate. Instead, more and more it looks like nothing really has changed.

At some point, and it should have been a very long time ago already, inflation indices should have been pushed upward by something other than WTI. If they aren’t, then this is the same indicated monetary condition as over the last eleven years since the last months in 2007.

The Fed is irrelevant. Sadly, from Volcker to Powell they don’t yet know it. That’s why they keep making these forecast errors. Central bankers here and everywhere else still believe that everyone still believes. Up until August 2007, the eurodollar system could run on belief.

Now it runs on risks. Those are what’s actually rising. Again.

Stay In Touch