We often forget, the middle 2000’s was not uniquely a housing bubble. It commanded our attention because that’s what ended up affecting so many Americans personally; whether foreclosures or just the negative “wealth effect” of declining real estate values. This was also pretty easy to understand, an asset bubble though complicated in its full manifestations intuitive as a result.

There were others, though, a proliferation of financial imbalances due to the global nature of monetary explosion. The EM corporate space was another, as was US commercial lending.

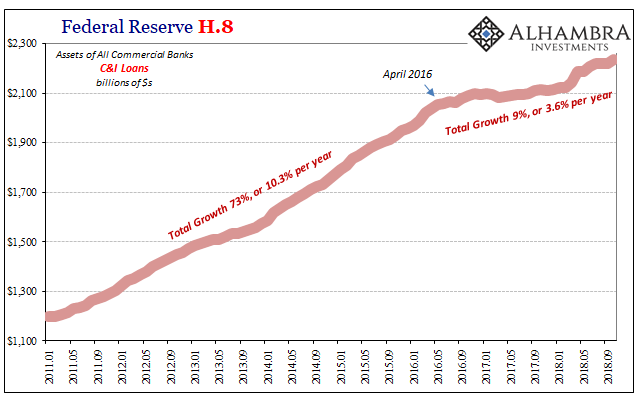

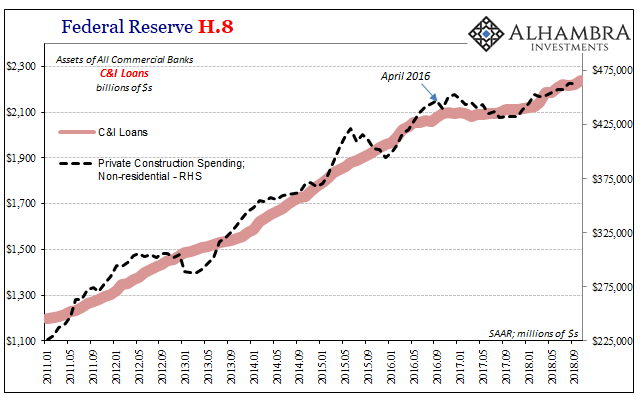

Commercial and Industrial Loans (C&I) would be late to the party, not beginning to rebound until after the “giant sucking sound” had taken a chunk out of domestic demand for credit. From May 2004 to October 2008, the Federal Reserve (H.8) estimates that lending in this space skyrocketed, an astounding 83% growth in a mere 53 months. That works out to a bubbly annual rate of nearly 15% per year.

You’ll also notice that banks really didn’t stop lending to domestic commercial enterprises until the entire financial system and economy began to collapse. The month after Lehman Brothers failed, in October 2008, C&I loans were still growing at a 15% annual rate. Beginning that November, they would eventually tumble an alarming 25% in total high to low (October 2010).

Over the eight years since, credit growth has returned at a more modest pace. Total loan values on the books of depository institutions are up again by more than 80%. This time, it has taken 96 months for them to get that far. It’s an annual rate of just 8.2%, much less than the middle 2000’s.

But even this comparison masks what’s really been going on. That “recovery” trend is really two. Credit growth has been slower, but not all at the same pace. In fact, up until April 2016, C&I loans were moving at a 10% annual increase. Since, across two and a half years, there isn’t much activity at all – a very clear change in trend therefore behavior.

Whereas loans were rising at a 10% average before, since the middle of 2016 they haven’t even increased by 10% total.

What’s odd is how this period corresponds with the so-called boom the current and immediately former Presidents are arguing over. The economy has magically roared back from the doldrums of a decade, but businesses aren’t borrowing like that’s really happening?

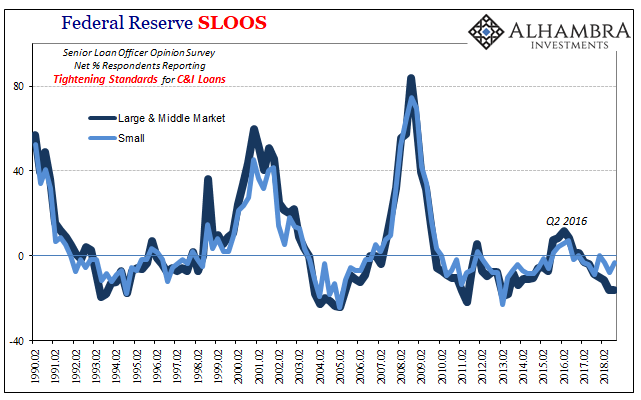

Other Federal Reserve data, the Senior Loan Officer Opinion Survey, or SLOOS, confirms that this is a demand function. In other words, bank lending officers report that overall credit standards in commercial lending are loosening at a historic rate. We cannot count regulations or the financial system as suspect. More banks are reporting being generous with covenants than at almost any point in the series history.

There was a modest tightening of standards in that same time period, Q2 2016, which has since abated especially for larger and mid-market commercial firms. The credit is there if anyone wants it.

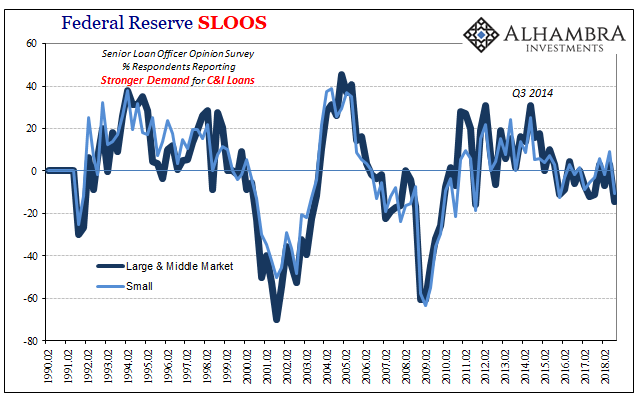

The SLOOS data also confirms that very few do. Reported demand for C&I loans continues to be conspicuously weak; certainly not what you would expect to see out of an economic boom. As the unemployment rate falls lower and lower, projecting one, US businesses remain completely cautious on credit.

The changeover, the point of inflection, tells us everything we need to know. In the middle of 2014, the start of the last “rising dollar”, commercial and industrial business grew cautious on credit as an “unexpected” global downturn emerged where global acceleration and recovery was predicted to be. Economists all over the world continue to forecast that same thing, but none of the credit data with the exception of lending standards fits those forecasts.

This wouldn’t be at all atypical, as again bankers are like central bankers the last to know. Last time, they kept right on lending into the worst economic downturn since the Great Depression. To their credit, pardon the pun, US businesses don’t appear to be very keen on repeating their end of that mistake by borrowing what’s otherwise available to be borrowed.

This post-2015 slowdown pattern is something we’ve seen in a number of places, from aggregate national labor income (contradicting the unemployment rate, and therefore the narrative of a labor shortage which is pretty much all there is supporting the idea of a boom) to private non-residential construction spending (capex).

American industry is neither borrowing nor building (nor paying labor) like there is robust opportunity in front of everyone. It’s just not there. But for that one statistic, the unemployment rate, the opposite case is made, another form of an “L.” The US economy nearly fell into recession in 2015 and early 2016, and it has not recovered from it. That’s exactly how businesses are acting.

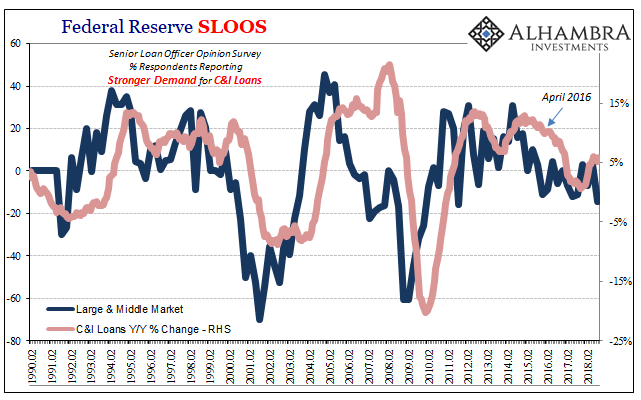

And now the global economy begins to see the re-emergence of minus signs – which may be what US commercial interests have been fearing for these last several years despite all the incessant mainstream assurances. Banks, as they are wont to do, extend credit terms based on Economists’ predictions and the always positive views of central bankers. The SLOOS estimates for credit demand, as of the latest quarterly data in November, are going lower still.

Commercial and Industrial firms are clearly reluctant to make the same mistake as the last cycle. If there really was a robust economy these past few years, borrowing wouldn’t be seen as a risky, potentially very costly mistake.

Stay In Touch