There are several points of confluence between financial markets and the real economy. Asset price volatility can produce negative effects on confidence, of course, forcing economic agents to reconsider their own business activities. More than that, in the gigantic bond market, in particular, a turn in pricing regimes is often accompanied by the dreaded credit crunch. That’s when it starts to get serious.

In the summer of 2007, even before everything really started to go south, you could tell there was a pretty serious economic setback looming when debt deals were pulled having nothing whatsoever to do with the mortgage or housing business. It would have been one thing had it been limited to subprime mortgage firms.

GM, for example, proposed selling its Allison Transmission unit to a pair of private equity firms, Carlyle being one. The deal had been announced in late June expected to close by mid-July before being pulled off the market when GM’s partners couldn’t easily arrange the debt financing they were counting on and expected. The deal eventually closed…on August 7, 2007.

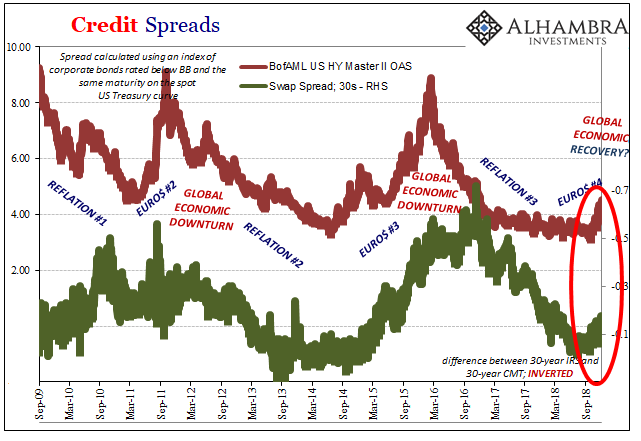

Others weren’t so lucky especially after August 9. From then on, the term credit crunch would become an understatement. This process has been repeated in the several financial redo’s redone since. None has as yet pushed the US economy into a declared recession, though it was close in late 2015, but credit damage isn’t limited to domestic conditions.

In late 2018, we are at least starting to hear the same faint echoes:

While the party isn’t quite over, financial jitters around the world have made lenders and investors less willing to give loans to heavily indebted companies. Loan offerings are being pulled and lenders are demanding — and getting — sweeter terms. JPMorgan Chase & Co. on Tuesday had to slash the price on a $210 million loan to 93 cents on the dollar from around 100 to help finance a private jet takeover. In Europe, three loans were scrapped over the last two weeks, victims of the Brexit tensions gripping the U.K.

Convenient excuses are just as much a part of the redrawn debt landscape; Brexit, or eurodollar? Let me be clear, these aren’t indications for immediate catastrophe. There isn’t a global recession lurking for tomorrow. Rather, these are, as usual, the same escalating warnings we’ve chronicled for over a year; beginning and leading down the road toward the possibility for a greater downside than maybe even 2015-16.

A credit crunch would be another signal as to inevitability.

Markets are being relatively sanguine about all this; then again, the shock of failure over “globally synchronized growth” is still just setting in. There are deeper problems than just a few sketchy leveraged loan deals to consider.

One is the potential for further collateral strain. As noted last month, an avenue for them earlier this year was the Eurobond market. Money dealers, what’s left of them, had been transforming some unknown proportion of the Eurobond binge overseas particularly among EM sovereign issuers into what was really a shadow trilateral repo play:

So, I have junk bonds, you have cash, a money dealer this securities lender can find UST’s from otherwise inert silos, and the bilateral repo carried out under pristine collateral is really a trilateral double bespoke transaction where junk forms the basis of everything. I give the money dealer the junk, he gives me the UST’s, I give you those for cash as if I owned them, and the smallest sliver of the wider world knows only about that last part of the transaction.

Thus, the rejection in 2018 of 2017’s wildly optimistic pricing in EM junk bonds, including many sovereigns, would play havoc in many collateral chains put together by these transformation links.

If US (and developed world) corporate junk is now being rethought, too, then the same collateral process using those as the starting point can potentially run into the same illiquidity troubles as had plagued the global system mid-year.

That’s how these things become self-reinforcing. It could be that’s why this latest eurodollar squeeze, number four, has been more visible mostly overseas up to this point. Until more recently, that’s where most of the turmoil has happened; and through which capacities the channel for economic distress has been limited.

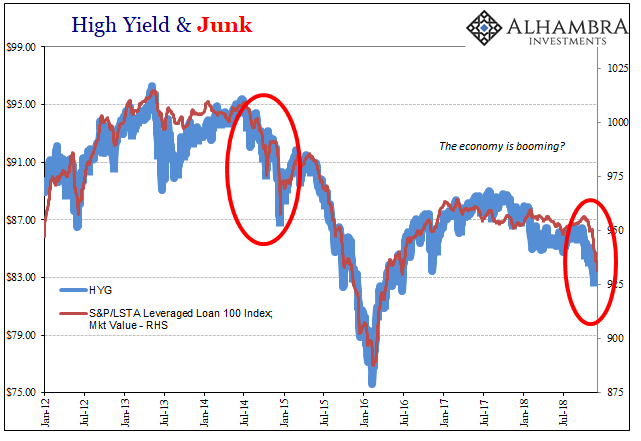

Market action over the past few months, especially following the post-October 3 transformation of the WTI futures curve, finally seems to have awoken nearer and closer market skepticism. Many are trying to claim this is nothing more than healthy rebalancing, especially as it applies to debt covenants (the prolonged lack of any). Perhaps, but more and more it seems as if “something” has changed especially in the context of what’s going on monetarily worldwide.

It’s not a huge jump to this point, though the more it continues to the more it looks to be that inflection. In the end, that may not really matter as timing isn’t as big a factor. If it goes like it did during previous episodes, the chances of a US and global downturn rise substantially (and that probability may be higher already than many otherwise appreciate, given curve inversions spreading out, too).

The flipside of that, obviously, is the greatly reduced chances for recovery and economic acceleration. Even Jay Powell has noticed that part of it (so-called Fed pause). Having experience very little upside so far the past few years, that can play into matters moving forward. After all, a lot of credit, junk, EM, and other, was written and funded under “globally synchronized growth” expectations. It’s surely one reason why the EM junk process turned negative so quickly and harshly April and May (leading to May 29).

It suggests, then, December might be a critical month establishing first any (however small) possibility for escaping this track and then how quickly the economic and continuing market downside might materialize. A credit crunch would be the biggest warning yet.

Stay In Touch