In the chaotic days of the early “recovery”, those opposed to the Federal Reserve’s response largely fell into the wrong camp. The central bank had done too much, they claimed. Never mind how the first global panic in four generations had developed and then crushed the global economy, such deflation was over to be taken apart by rapid inflation if not hyperinflation.

The Fed was printing money, everyone believed, a big no-no as demonstrated throughout history. Weimar Germany comes to DC.

Not so, the central bank pushed back. You can be afraid of money printing all you like, but what we are doing isn’t money printing. The creation of bank reserves is nothing more than an accounting remainder.

Here’s one (of many) FRBNY response to the inflationistas from December 2009:

However, a careful examination of the balance sheet effects of central bank actions shows that the high level of reserves is simply a by-product of the Fed’s new lending facilities and asset purchase programs. The total quantity of reserves in the banking system reflects the scale of the Fed’s policy initiatives, but conveys no information about the initiatives’ effects on bank lending or on the economy more broadly. [emphasis added]

The paper goes through the accounting details of LSAP’s with quite satisfactory sufficiency. I have even used these very examples as the basis for going further, the bank structure for Eurodollar University both Series 1 and Series 2 (as well as looking at the implications starting here).

QE was nothing more than an asset swap (in my view, not a very useful one, either). Officials were, at first, well aware of this fact if only to shield themselves from growing mainstream criticism. A lot of that was tied not just to visions of hyperinflation but also restarting the stock bubble. The two were taken as the same; money printing would unleash consumer and asset inflation.

It was all unsophisticated noise, however, this condemnation originating from the same position of eurodollar ignorance that ironically derived from believing too much in the central bank itself. The consequences of its critics being wrong on inflation somehow has meant the central bank cannot be criticized at all. Politicians are now scared.

The Fed doesn’t print money but if businesses and consumers (or stock investors) want to believe that it does so much the better. The modern central bank, after all, operates an expectations-based regime.

There is no money in monetary policy, and FRBNY’s 2009 paper shows exactly that.

In 2018, by contrast, nobody worries about too much inflation any longer since everyone is still waiting for the recovery. In fact, 2017’s hysteria was in response to this fact; the idea that at long last it was going to show up not in hyperinflation but in real recovery that was by then more than half a decade long overdue.

Therefore, nobody wants to talk about the 2009 paper anymore because it might come too close to proposing the start of an explanation for all the years in between.

As is often the case, confirmed by my own experience, there exists a wide gap between the intellectual capacities of those at the top and what’s better understood by the staff underneath. The central bank, like any other government agency, is run by empty suits often those who speak well enough to present themselves as if they know a thing or two.

Pedigree and just enough public speaking prowess (along with a criminally compliant media) apply the gloss of competence. The results demonstrate the complete opposite.

Those within the Federal Reserve system some may realize the Federal Reserve system didn’t print money. Those at the top, they don’t seem to. On only a few occasions do the FOMC members seem aware of what it was they were actually doing. And even then, it is clear that they don’t fully understand the implications.

One of those was the 2011 crisis, a truly sordid affair for so many reasons. As I’ve written many times before (so I’ll spare you repeating the sermon again), 2011 was the final nail in the recovery coffin. But even then, it shouldn’t have been. If 2008 wasn’t enough to convince the FOMC it didn’t know what was going on, monetarily speaking, 2011 should’ve confirmed it as well as diagram what it was they didn’t know.

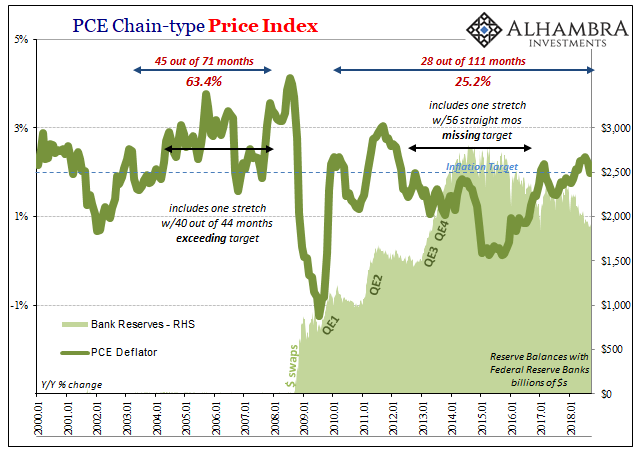

The huge difference between effective money and bank reserves.

Today, the Fed releases its full transcripts for the 2013 meetings, those conducted in the shadows of 2011 leading absurdly to a third then a fourth round of QE. Several people have now sent me the same quote, one from January that year spoken by Dallas Fed President Richard Fisher. Remember who Fisher was; first and foremost an inflationista. He didn’t publicly criticize the Fed as the others, worried as they were about hyperinflation, but I believe he would’ve liked to have joined them in doing so.

Here’s what he said six years ago:

MR. FISHER. Yesterday, many at the table inferred that we might take credit for the perceived improvement in the economy, but nearly all of the money that we’ve created remains in the form of excess reserves. It isn’t circulating through the economy. What we have done, basically, is to provide a monetary head fake. We’ve used language, which is good, and declarations, and indeed, we have, I think, had some effect.

He almost gets there, but doesn’t quite go all the way (because, as history showed, he was actually incapable). Monetary head fake. Excess reserves not circulating through the economy.

Where Fisher goes wrong, and the rest of them, too, is what he believes will happen when they do begin to circulate – thus his early hawkish stance. In Fisher’s view, bank reserves weren’t being current money, they were potential money. That was the head fake to him.

He never realizes, as FRBNY 2009 hinted, they may never circulate at all because that’s not what modern bank reserves are really about. In the eurodollar system bank reserves are, actually, never money. They are, again, just one form of bank liability and not a very dynamic one.

But even assuming Fisher’s position was true, neither he nor anyone at the FOMC ever thought through all the implications. The reserves clearly weren’t circulating in 2012 (as they didn’t in 2011, obviously), yet the FOMC seemed pretty confident they would in 2013 or 2014.

What if they didn’t?

Even as the economy failed to match expectations (recall Stanley Fischer’s 2014 Scandinavian confession) for several years more, US monetary officials continued to ignore the possibility each and every time (at least in public; perhaps there are later discussions and debates about what the Fed actually had done, maybe in 2016 after that downturn, but I really doubt it). You would think someone would say, hey, this potential money just isn’t living up to any potential. Especially after the FOMC missed its inflation target for almost half a decade straight!

Maybe it isn’t any kind of money?

This is where it becomes almost purely political. Would Janet Yellen ever have had the nerve to come out in 2016 and apologize for seven years of “monetary head fake?” No way. Because if she or now Powell would say it, people would go back and rethink everything from the ground up – including and especially 2008.

If you guys don’t do money, what the %&@# were you all doing during that huge monetary panic? You mean, we went through a global crisis without recovery for ten years because you people didn’t read and think all the way through your own research? That sort of admission isn’t happening because that’s what did happen in a sense.

This is one reason, I believe, why so many central bankers (not just in the US) were so emotionally attached to “globally synchronized growth” and therefore purposefully hyped the hell out of it. The unemployment rate was their only way out, the last little tidbit that something might’ve gone right. It was almost like the last chance to be let off the hook for not coming up with any answers despite so many obvious questions.

Richard Fisher, out of any of them, was asking and in 2013!

Once you get past the unearned mystique about QE and bank reserves, then you can get into what the real monetary system looks like. It’s a far larger, more exhaustive journey still, this half century of shadow money darkness.

We are all trapped until the world realizes this fact, one that is being proven again for a fourth time right now. At only a couple points in over a decade did the empty suits almost get there. These best and brightest.

Stay In Touch