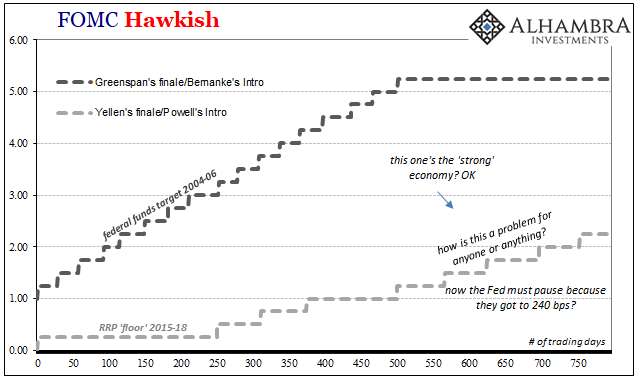

There is much more chicken to each hawk than any of the birds would care to admit. What I mean by that is fairly straightforward, or it should be. Alan Greenspan was resolute. Right or wrong (the latter, trust the curves), after taking federal funds down to 1% officials pushed the rate right back up to 5.25% without pause. At every meeting interval during the middle 2000’s, the FOMC added another 25 bps.

There was no equivocation or lamenting R*’s and complicated repo mechanics. They may not have known what they were doing, but they at least believed in their own madness.

Janet Yellen began the same trajectory in the second year of her tenure. After taking almost all of 2016 off, the first Fed pause, she resumed with a conspicuously cautious attitude. She’s already gone now, a year already, and the rate is still closer to zero than Greenspan’s middle portion. QE was the most powerful monetary instrument ever unleashed, they said, but the economy that came from it couldn’t withstand more than three or four 25 bps hikes per year?

Sure.

Not only that, especially since 2017 policymakers have ratcheted up the rhetoric. The less they act the more they claim it is because the economy is too strong. Don’t bother about the contradiction, it’s another one of those aspects of Economics you aren’t meant to actually think about. Expectations policy was stripped of its rationality a long, long time ago.

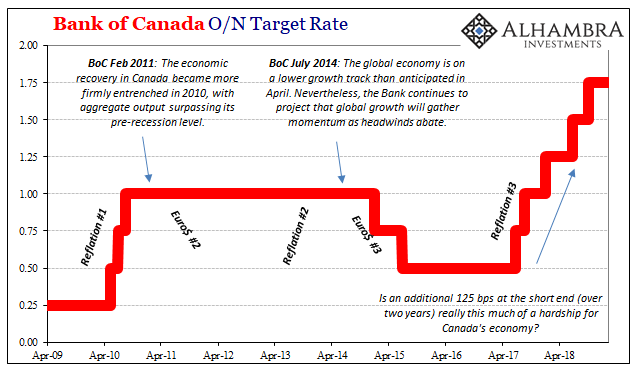

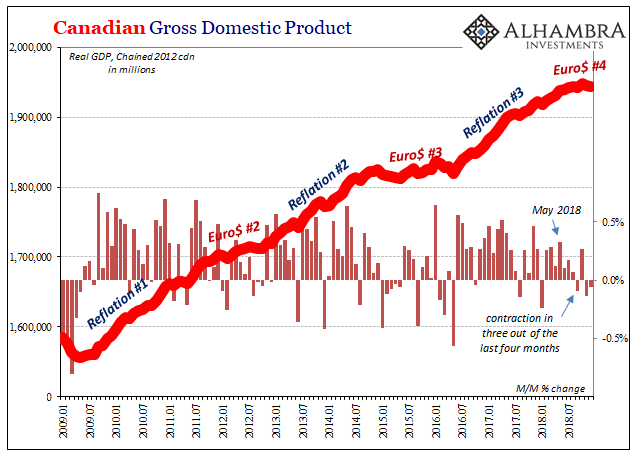

The Federal Reserve isn’t the only central bank which has chosen the chicken. Our neighbors to the north in Canada, their central bank has followed in Yellen’s footsteps. Its head officials keep saying Canada is booming, very close to dangerously overheated inflation. Ever since July 2017, the Bank of Canada has been doing the 25 bps thing, too.

But not every meeting, you see. The ungodly strength of the Canadian economy couldn’t handle such regular rate hikes. Instead, five 25 bps increases have been spread out across thirteen policy meetings. That last one was all the way back in October.

The only time BoC did back-to-back was the first two in the middle of 2017.

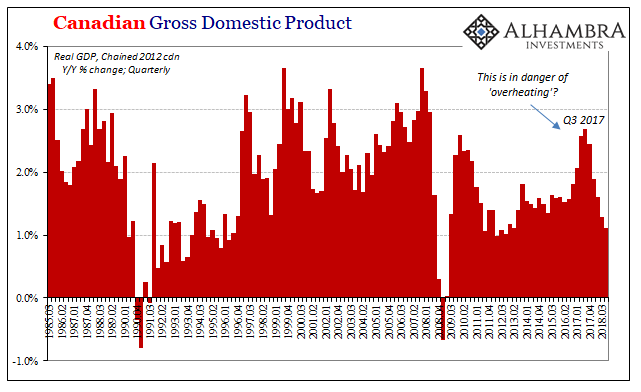

Ever since that second hike, the one in September 2017 (note the timing), Canada’s economy has been off. It was certainly on an upswing before then, with GDP clearly accelerating from the second half of 2016.

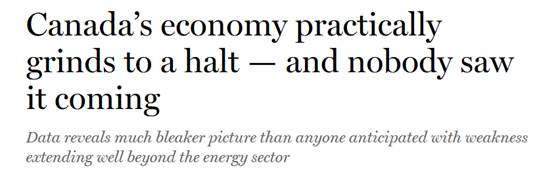

In the five quarters since, though, what went up has come down. According to the latest estimates from Statistics Canada, real GDP had contracted in three out of the final four months in 2018. If you were relieved by lagging US GDP, take a gander at leading Canada. The Canadian economy has, as one Calgary news headline put it, ground to a halt.

The real news, of course, is the rest of what is written above. As M. Simmons points out, the substantial weakness is this time, as each time, “unexpected.” It is always unexpected.

Broad-based weakness in Canada is a sign of the times, exactly where broad-based strength would have been had it been a real trend. As elsewhere around the world, Canadian officials grabbed onto 2017’s Reflation #3 really turning it into the slogan of globally synchronized growth. Well, it was synchronized but it didn’t ever amount to a realistic path toward sustainable growth.

Central bankers wanted to believe in it because they realized just how pressed for time they were. It was 2017, after the elections in 2016 around the world they began to realize people wanted results.

Except, they weren’t ever actually convinced. They sounded like it in public, to be sure, but it’s not what they say it’s what they do. In other words, if they had truly believed in globally synchronized growth it would’ve been full throttle on the rate hikes.

As in 2007 and 2008, monetary policy is conducted by a fingers crossed strategy. Hopefully, maybe by speaking in confident tones people will just overlook everything else rational that undermines the authority. It is, in fact, a preposterous way to conduct a nation’s monetary affairs.

This is what 2018 represented, another chance to be reminded that these people really have no idea what they are doing, their monetary policies totally devoid of any money in them. Yet, as the newspaper headline once again demonstrates, they are afforded every benefit and by virtue of only their pedigree their unsubstantiated claims are repeated widely and forcefully.

Central bankers tell us what to think on the economy though they aren’t sure themselves what they should be thinking. The only thing we do know from them is what they mawkishly wish might happen. That’s some pretty substantial fine print.

Once you understand the nature of this central banking business, you begin to sketch out the same broad outlines of what really and truly moves the global economy up and down. It isn’t a central bank’s monetary policies; it isn’t any central bank at all. They just aren’t central.

Instead, modern monetary doctrine, as is on display in Canada right now, comes down to hoping you never notice. The global economy needs monetary competence and all we’ve been given by the so-called best and brightest is destructive theater.

Like Germany’s, Canada’s economy tells us something very important about the global direction. With Canadian activity tied more closely to Asia, there’s that about them, too. The Bank of Canada didn’t kill a strong economy by adding a mere 125 bps to their overnight target rate. This northern misfortune was set in motion whether policy was changed or not.

What makes any of them chicken, I think, is that on some level in their worst nightmare some of them are starting to realize this is true. Then when these downturns stop being “unexpected”, that’s when it becomes time to turn the lights on them.

Stay In Touch