They will have to be forced into it. There is no voluntary rate cut and there never has been. This idea, however, is what’s being offered today in the wake of another stubborn line in the sand.

Central bankers are always, always the last to figure things out. Jay Powell was still talking about inflation and more aggressive monetary policy in the middle of December. He wasn’t thinking about any sort of “pause” back then, just a few months ago. He had his mind changed for him.

This new dovishness wasn’t his idea. It’s a stepped process.

At his press conference today, the Federal Reserve’s Chair (no more “man”) reiterated his new redline. Inflation is down again, unexpectedly, but it will surely pop right back up. What’s holding it back are some new “transitory” factors (mentioning airline tickets and financial services) that have, unexpectedly, replaced the old set of transitory factors (Verizon).

You may have noticed how there has been an almost continuous string of transitory factors that strung together add up to this persisting undershoot. Powell even had the nerve to use a form of that very word:

If we did see inflation running persistently below, that is something the committee would be concerned about and something we would take into account when setting policy.

If I am swimming in the deep end of a pool, and someone swimming underneath me reaches up and pulls me under the water’s surface, what matters, according to Powell, is not that I drown eventually it’s whether or not the same person holds me down the entire time. If that first devilish act is given up to a second’s, and then a third’s, maybe a fourth, each of those is to be treated separately and individually?

The more honest and unbiased out there among you might instead suspect that each of those transitory murderers was probably, likely connected together somehow. It would have to be some hugely random coincidence otherwise. The criminal investigation would start here, not end there in the usual shrug of the shoulders over a tragic accident.

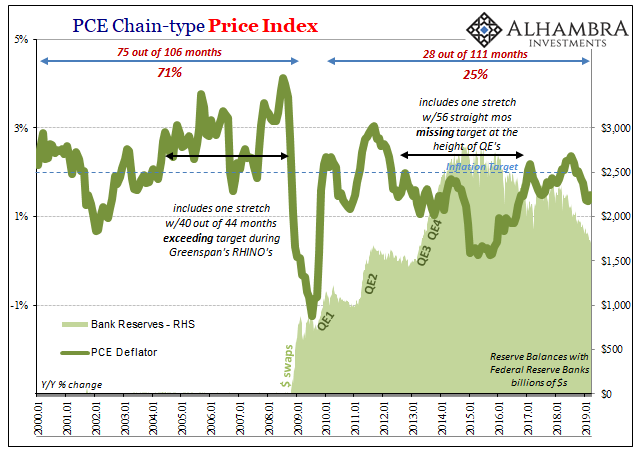

The last 111 months (shown above) have been the very model of “persistent” when it comes to inflation. Economists would have you believe, though, that something substantial has changed in the past few years. The persistent undershoot is now persistent transitory inflation factors, as if that’s actually different even though both end up with the same result.

It is the theater of absurd repeating itself all over again. Nobody has paid any attention to Bill Dudley. That guy more than any of the others in 2007 made these very same mistakes of downplaying bad market signals. The eurodollar futures curve, in particular, warned him for months and months and months that the FOMC under Bernanke with Dudley as its chief advisor (Open Market Desk) was far, far more likely to cut rates than do anything else.

We know how it turned out; the rate cuts were only the beginning. It was a very different reality the whole Economist community had to be dragged kicking and screaming to face up to. A central banker is never cleverer than when being shown market data contradicting their predetermined conclusion.

To that end, is the third time the charm? Or is it Strike 3?

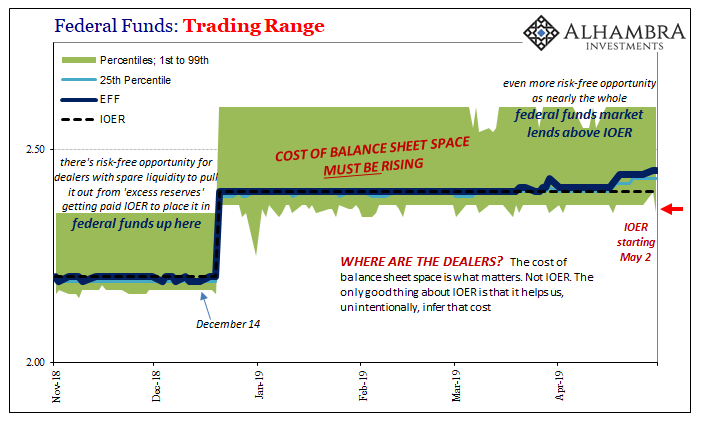

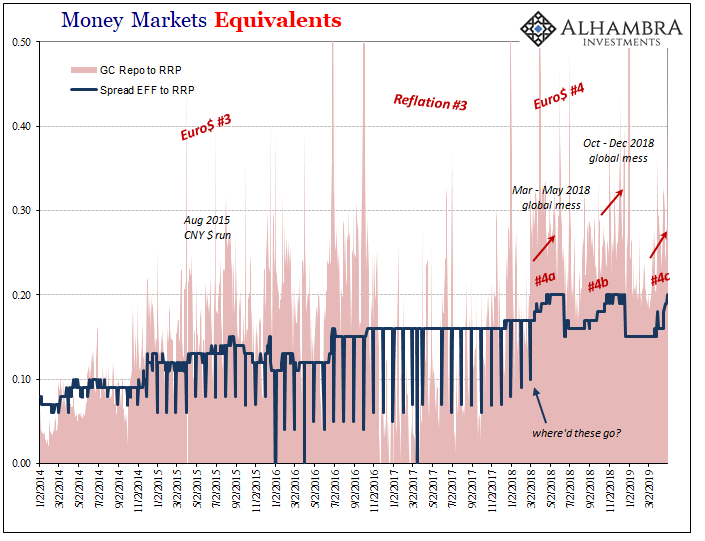

The only change to the FOMC’s policy today is IOER. The Committee has voted for a third “technical adjustment” to its policy mechanics. Starting tomorrow, the central bank will now pay 235 bps on excess reserves placed with the central bank. That’s a change to 15 bps below the upper bound (which didn’t change), 5 bps further down than today.

Presumably, this will incentivize anyone with spare liquidity to seek better returns which just so happen to be quite literally everywhere already.

The entire FOMC affair is an abject lesson in the only reason why we pay attention to IOER. If they can’t get the small stuff right, if you have to struggle and adjust and fight just to keep the irrelevant federal funds rate on track, then no wonder you won’t see the reasons for an unwanted rate cut coming right at you. Three technical adjustments, but Jay Powell is right about transitory inflation?

You can appreciate market skepticism. No one ever forces him to answer the only question that matters.

The central bank’s shift follows an increase in recent weeks in the effective fed funds rate within that band. The benchmark has been above IOER for more than a month and this week crept up to 2.45 percent, fueled in part by rates squeezing higher in other short-term funding markets.

WHY ARE RATES BEING SQUEEZED HIGHER IN OTHER SHORT-TERM FUNDING MARKETS?

Even if you believe the problem is QT, you still have a big problem. Where are the dealers? In the absence of the Fed’s bank reserves, the private banking dealer system should be filling in the vacuum. That’s their entire purpose. A resilient monetary system, as Janet Yellen used to say, wouldn’t need the Fed’s balance sheet at all.

But it’s not QT. It is instead the dealers, the only “money” that matters. They won’t supply it. Increasingly, they are hoarding. Again.

Jay Powell looks at the unemployment rate and from it alone he, like Yellen and Bernanke, concludes a whole bunch of sweeping generalizations that are about to blow up in his face. At less than 4%, to officials it must mean: the financial system is totally healed; the economy is fully mended; and all because central bankers know what they are talking about. QE was genius.

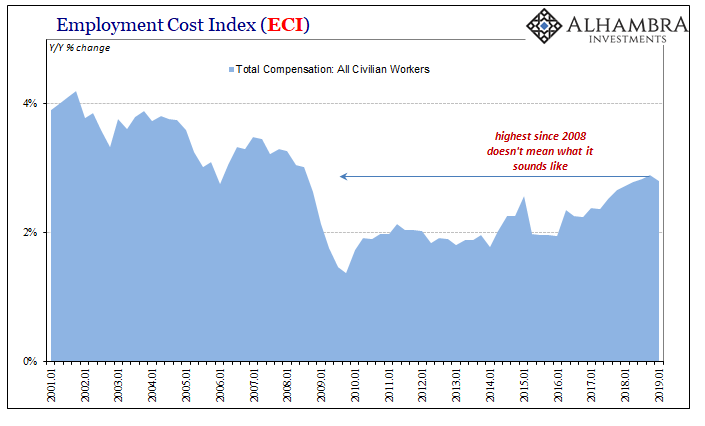

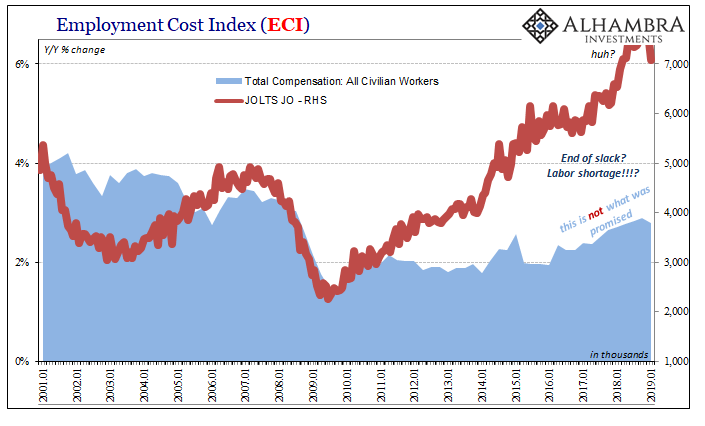

There’s just no inflation, there’s not even wage data (the latest Employment Cost Index, released yesterday, shown above) to suggest there’s a tight labor market let alone one epically imbalanced in the positive direction, and now proliferating minuses all over the global economic landscape. Three technical adjustments. The very things that would make an honest person a little skeptical about the mainstream story, maybe even to consider a better chance of a rate cut certainly than rate hike. Whether or not Jay Powell today wants to, that’s entirely beside the point.

He has no idea what he is doing. Kicking and screaming. Don’t fight the Fed? The Fed always fights…reality.

Stay In Touch