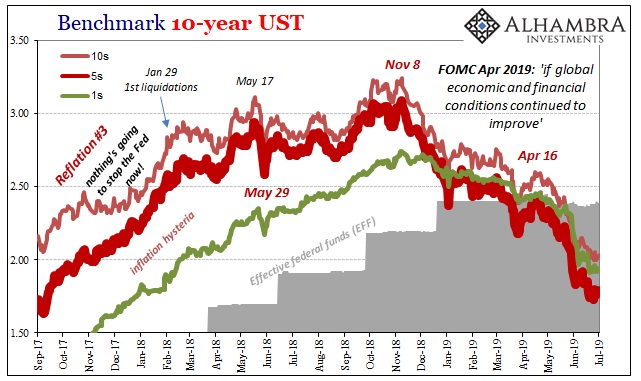

The benchmark 10-year US Treasury yield closed below 2% for the first time since Donald Trump was elected President. Having flirted with that level several times over the past week, today the most-watched interest rate on the planet finally breached this one startling round number. And it comes during a week which by every conventional account should have been hugely positive.

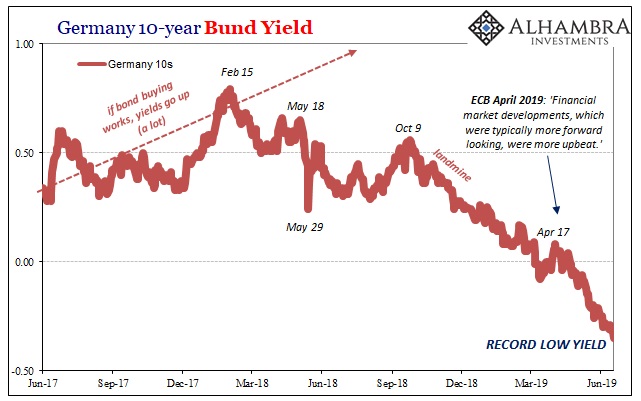

Despite what has been called a trade truce between the US and China, the bond market has been unimpressed in every way imaginable. Not only is this 10-year yield back sporting a 1 handle, Germany’s federal 10-year bund is way ahead in the race to becoming Japan. It finds new record lows, record negative lows, seemingly a few times consistently every week.

At -35 bps in “yield”, the German market like the UST market is already telling you something important.

Still, there are those who maintain interest rates have gotten way ahead of themselves. Maybe it’s the context; after all, not that long ago the mainstream view was one of accelerating growth and inflation. It was only November when whichever bond king had last claimed interest rates had nowhere to go but up.

Here they are getting reacquainted with old levels we’d been told repeatedly the world would never see again. What is going on here? This disconnect is hard to process from the mainstream point of view. It may seem like things have changed far too quickly, therefore more emotion than reality.

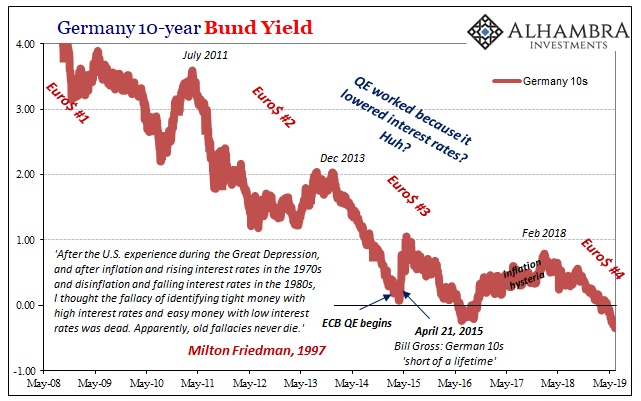

Part of the problem is the media. Practically no one understands curves anymore. Milton Friedman’s interest rate fallacy is deeply ingrained in the public consciousness – Alan Greenspan’s real legacy is being so totally upside down on bonds and rates he had no possible way of anchoring monetary policy.

Since there’s no actual money in that policy, he didn’t think it would matter.

Yet, here we are in 2019 and still interest rates are being mischaracterized. This includes, apparently, for one particular bond “bull.”

For [renowned bond bull Steven] Major, a lot of bad news is already in the price. Trade tensions between the U.S. and China, signs of economic slowdown as well as geopolitical risks have all forced central banks to become more dovish, sending American bond yields lower by nearly 90 basis points this year.

Negative factors, totally unexpected, of course, forced “central banks to become more dovish”, and that dovishness is what is driving interest rates back into the depths? Nope. Not even close. This is the “maestro’s” backwards view.

But it’s the only way to reconcile what’s going on in bonds with current Economic dogma about money.

In reality, it is a flight to liquidity which causes the movement in rates, the bond market merely believing, actually knowing, that central bankers will inevitably be forced by these big problems to try and catch up. That’s their only role in this.

So, what is the bad stuff? When you add up what’s in the mainstream, it just doesn’t come out. Trade tensions and geopolitical risks don’t you get you below 2% on the UST 10s nor continuing record lows on Germany’s bunds. That’s just not enough, a realization that Mr. Major acknowledges:

“I’m not in the business of being deliberately negative,” Major said in a phone interview. “To get darker than this, to predict a Japan scenario, we would need new information.”

And that’s the whole point: that’s just what the market is telling you! There is new information, you just choose not to see it. Something is spooking the bond market, right now, but because even for bond bulls they still think in mainstream monetary and central bank terms it doesn’t become recognizable until it’s so obvious even a central banker can see it and finally (and pointlessly) acts.

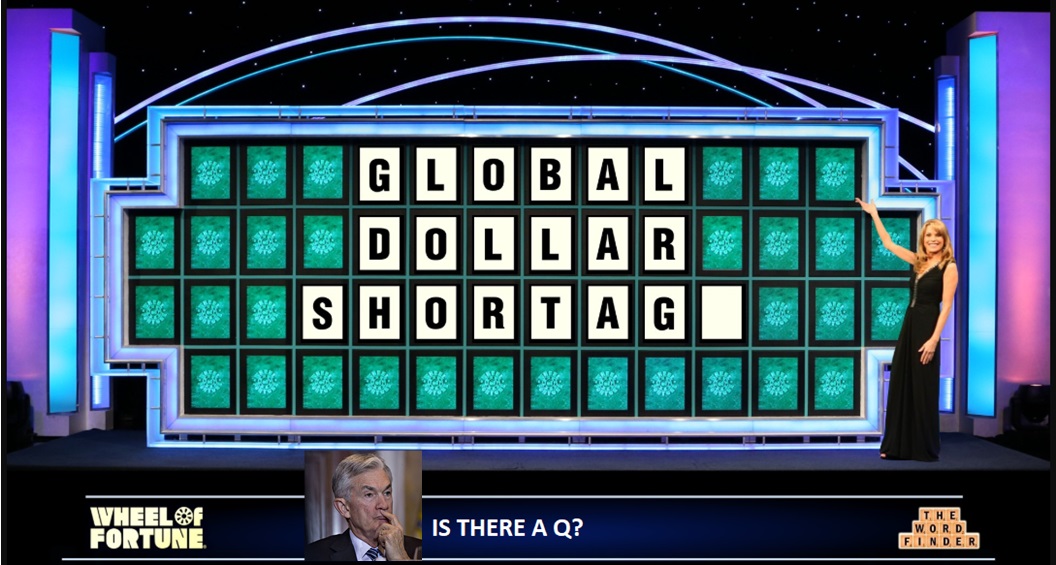

What I’m talking about is what is clearly a global dollar shortage; another one. To Mr. Major, like all the bond kings, this will be “new information” though it needn’t be. All the evidence keeps pointing to liquidity risk as that something behind these market movements.

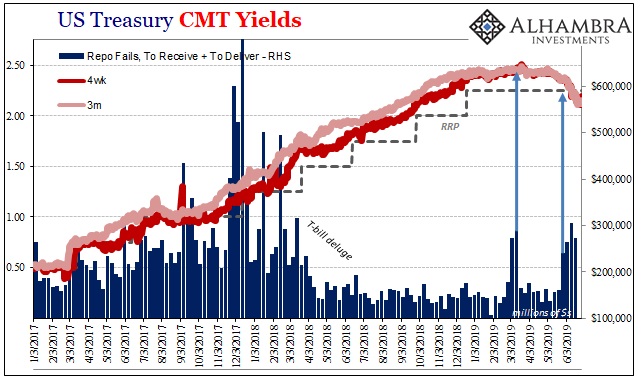

I’ve covered federal funds once already today. In the repo market, not only are fails still well above recent averages, they’ve stayed this way for over a month (up until the latest data from June). According to FRBNY, reported repo fails (UST collateral) have totaled more than $240 billion in each of the last four weeks.

This has coincided with the more extreme movements across the yield curve, including bill yields plummeting well below what are otherwise supposed to be equivalents (such as the RRP “floor”).

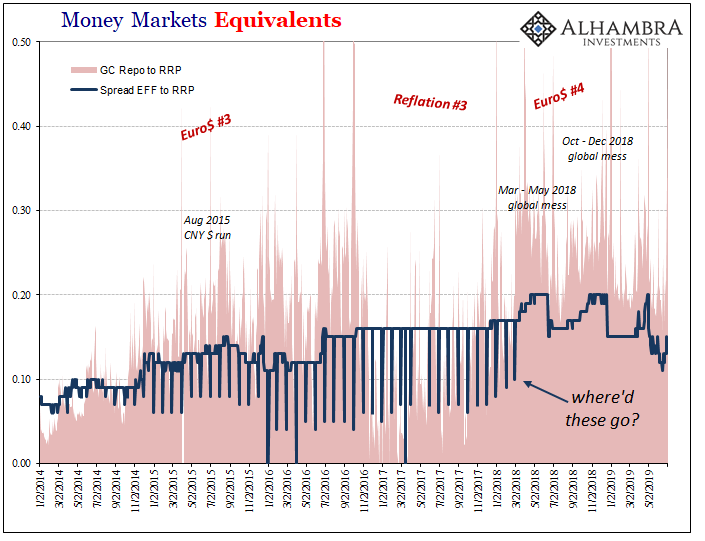

If that wasn’t enough on its own to describe a far less than ideal funding environment, how about the repo rate? DTCC figures the GC rate for UST collateral was 2.87% yesterday, 62 bps above the RRP, and still above 2.60% today. Both are higher than they were on June 30, the actual quarter-end.

It has been even less desirable in MBS repo.

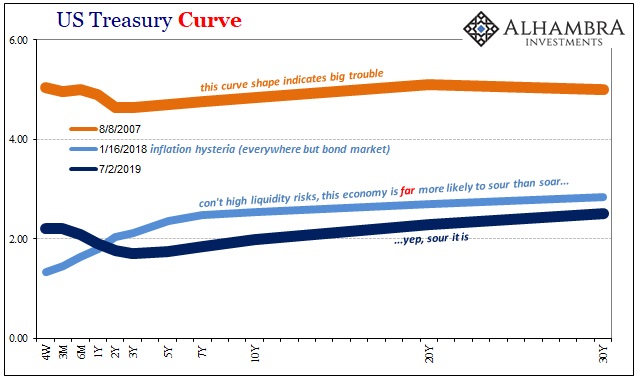

People don’t think there is any liquidity risk because they’ve bought the Fed’s puppet show on QE. The bond market is telling you, screaming at you, that not only is there liquidity risk it is getting ridiculous. For longer yields to be falling, as they are in Germany, that’s already one thing; for them to do the same thing with the short end where it is in US$ markets, this is quite serious.

Curve distortions of this magnitude aren’t just rare, they are meaningfully scarce.

Not choosing to be so blind about the way things actually work in practice, we have the option of recognizing the one factor all the evidence keeps pointing toward. If it walks like a duck, swims like a duck, and quacks like a duck, it’s almost certainly a duck. QE says it can’t be a duck, though, because monetary policy exterminated the species and we have to take their word for it even though no central banker has ever been asked to produce a single dead duck.

If you believe in Greenspan, then all ducks have been eradicated and like for him the bond market is a suspect place for wild and irrational pessimism. It might as well be a hyper-sensitive if caring central bank mixing up a more dovish punchbowl (to further mix metaphors) that is causing interest rates to dive as they have. You might even take comfort in that particular “stimulus” scenario.

It seems so simple, getting anyone to understand how bonds and rates actually work. So thorough has Economics screwed everything up, hardly anyone believes their own eyes. Even so-called bond bulls. It will only seem like new because they’ve chosen, repeatedly, to dismiss what is otherwise and already consistent information.

Stay In Touch